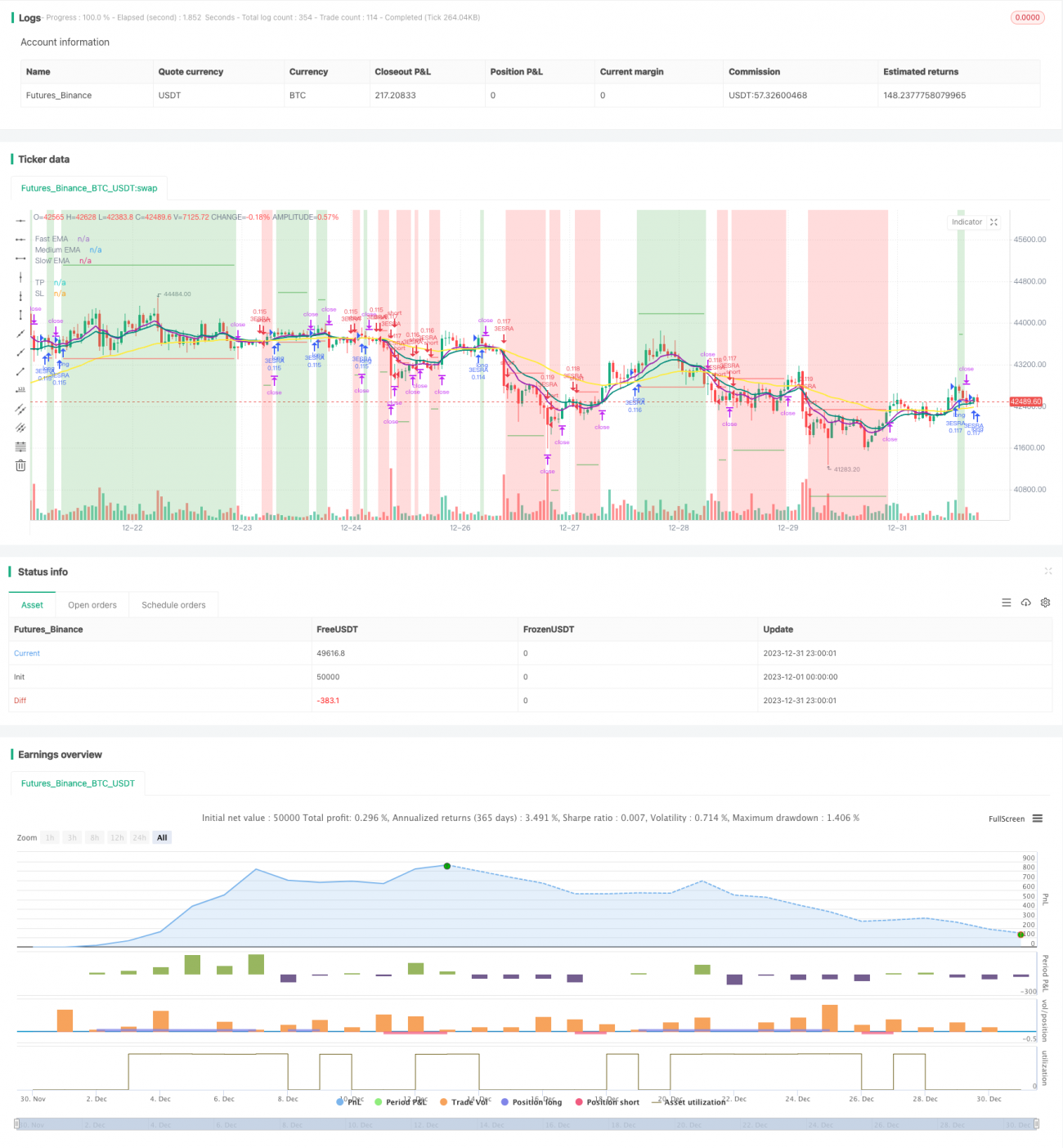

トリプル指数移動平均線とストキャスティック指数平滑移動平均線の取引戦略

概要

この戦略はトレンドフォロー戦略であり、トリプル指数移動平均線とストキャスティックRSIインジケーターを組み合わせて取引シグナルを生成します。短期移動平均線が中期移動平均線を上抜け、中期移動平均線が長期移動平均線を上抜けた場合に強気、逆に短期移動平均線が中期を下抜け、中期が長期を下抜けた場合に弱気と判断します。同時に、この戦略ではストキャスティックRSIを補助的な判断指標として導入しています。

原理

-

8日、14日、50日のトリプル指数移動平均線を使用します。8日指数移動平均線が14日指数移動平均線を上抜け、14日指数移動平均線が50日指数移動平均線を上抜けた場合に買いシグナル、その逆で売りシグナルとなります。

-

ストキャスティックRSIを補助判断指標として使用します。具体的には、まず14日RSIを計算し、そのRSIに基づいてストキャスティックを計算、さらにストキャスティックに対して3日単純移動平均を計算してK線とし、同様に3日単純移動平均をD線とします。K線がD線を上抜けた場合、買いの補助シグナルとします。

-

取引シグナル発生時、価格が8日指数移動平均線より上であれば買いエントリー、下であれば売りエントリーを行います。

-

ストップロスはエントリー価格の上下1ATRの位置に設定します。利確はエントリー価格の上下4ATRの位置に設定します。

優位性

-

移動平均線を基本指標とすることで、市場トレンドを効果的に追跡できます。トリプル指数移動平均線は複数の期間を組み合わせることで、短期および中長期トレンドへの感度を同時に確保します。

-

ストキャスティックRSIを補助判断指標として追加することで、偽シグナルをフィルタリングし、エントリー精度を高めます。

-

ATRに基づいてストップロスと利確位置を設定することで、市場の変動度合いに動的に対応でき、ストップロスや利確が大きすぎたり小さすぎたりするのを防ぎます。

-

この戦略のパラメータ設定は合理的であり、大きなトレンド下で優れたパフォーマンスを示します。ドローダウンが小さく、収益は安定しており、長期運用に適しています。

リスク

-

複数の指標を組み合わせた戦略は、反転リスクを高めます。移動平均線とストキャスティックRSIが反対のシグナルを発した場合、誤った取引シグナルが発生する可能性があります。その際は、価格自体のトレンド性に注意する必要があります。

-

ストップロスと利確の設定が保守的であるため、相場が急激に変動した際に突破されて損切りされ、トレンドの機会を逃す可能性があります。その場合は、ATRパラメータを適宜調整するか、ストップロス・利確の倍率を大きくすることが考えられます。

-

トリプル指数移動平均線を使用しているため、短期線と中期線が反転する際に一定の遅れが生じます。その際は、価格自体が反転しているかどうかを確認し、エントリー判断を行う必要があります。

-

この戦略は主にトレンド相場に適しており、レンジ相場ではパフォーマンスが低下します。その場合は、移動平均線の期間パラメータを最適化するか、他の判断指標を使用することを検討します。

最適化

-

MACDなどの他の指標を追加して、エントリータイミングをさらに最適化することを検討できます。また、異なるパラメータの移動平均線の組み合わせをテストすることも可能です。

-

ATRの多空チェック用パラメータを最適化できます。例えば、ストップロスを1ATRから1.5ATRに、利確を4ATRから3ATRに変更した場合に、より良い収益が得られるかどうかを確認します。

-

移動平均線のみを使用し、ストキャスティックRSIを削除した場合に、ノイズをより除去でき、より安定した収益が得られるかをテストできます。

-

出来高指標など、トレンド判断のための追加条件を組み込んで、大規模なトレンドでの取引を確実にすることも検討できます。

まとめ

本戦略はトリプル指数移動平均線とストキャスティックRSIを総合的に活用してトレンド方向を判断します。エントリーシグナルは比較的厳格で、無駄な取引を効果的に削減できます。利確・ストップロスをATRに基づき動的に設定することで、戦略パラメータに自己適応性を持たせています。バックテスト結果から、この戦略はトレンド相場で優れたパフォーマンスを示し、ドローダウンが小さく収益は安定しています。さらなる最適化により、より良い結果が期待できます。

- 1