Estratégia de Negociação com Média Móvel Exponencial Tripla e Média Móvel Exponencial Suavizada Estocástica

Visão Geral

Esta estratégia é uma estratégia de acompanhamento de tendência que combina o indicador de Média Móvel Exponencial Tripla (TEMA) e o indicador de Índice de Força Relativa Estocástico (Stochastic RSI) para gerar sinais de negociação. Quando a média móvel rápida cruza acima da média móvel intermediária e a média móvel intermediária cruza acima da média móvel lenta, é um sinal de alta; quando a média móvel rápida cruza abaixo da média móvel intermediária e a média móvel intermediária cruza abaixo da média móvel lenta, é um sinal de baixa. Além disso, a estratégia introduz o indicador Stochastic RSI como um indicador auxiliar de julgamento.

Princípio

-

Utiliza médias móveis exponenciais triplas de 8, 14 e 50 períodos. Quando a MME de 8 períodos cruza acima da MME de 14 períodos e a MME de 14 períodos cruza acima da MME de 50 períodos, um sinal de alta é gerado; caso contrário, um sinal de baixa.

-

Utiliza o indicador Stochastic RSI como indicador auxiliar. Especificamente: primeiro calcula o RSI de 14 períodos; em seguida, calcula o indicador Estocástico sobre o RSI; por fim, aplica uma média móvel simples de 3 períodos ao Estocástico para obter a linha K e uma média móvel simples de 3 períodos para obter a linha D. Quando a linha K cruza acima da linha D, é um sinal auxiliar de alta.

-

Ao gerar um sinal de negociação, se o preço estiver acima da MME de 8 períodos, entra em posição comprada; se o preço estiver abaixo da MME de 8 períodos, entra em posição vendida.

-

O stop loss está posicionado a 1 vez o ATR abaixo/acima do preço de entrada. O take profit está posicionado a 4 vezes o ATR acima/abaixo do preço de entrada.

Vantagens

-

A média móvel como indicador base pode rastrear eficazmente as tendências do mercado. A Média Móvel Exponencial Tripla, ao combinar múltiplos períodos, garante sensibilidade tanto a curto quanto a médio/longo prazo.

-

A inclusão do Stochastic RSI como indicador auxiliar pode filtrar sinais falsos e melhorar a precisão das entradas.

-

A definição de stop loss e take profit com base no ATR permite acompanhar dinamicamente a volatilidade do mercado, evitando stops ou metas excessivamente amplos ou estreitos.

-

A configuração de parâmetros da estratégia é razoável, apresentando bom desempenho em tendências fortes. O drawdown é pequeno e os retornos são relativamente estáveis, adequados para operações de longo prazo.

Riscos

-

A combinação de múltiplos indicadores aumenta o risco de reversão. Quando as médias móveis e o Stochastic RSI emitem sinais opostos, podem gerar sinais de negociação incorretos. Nesses casos, é necessário observar a tendência do próprio preço.

-

A definição de stop loss e take profit é relativamente conservadora, podendo ser violada em movimentos bruscos de mercado, resultando na saída precoce e perda de oportunidades de tendência. Nesses casos, pode-se ajustar o parâmetro ATR ou aumentar o múltiplo do stop/take.

-

Devido ao uso de médias móveis triplas, quando a linha rápida e a linha intermediária se revertem, pode haver um certo atraso. É necessário observar se o próprio preço se reverteu para decidir sobre a entrada.

-

A estratégia é mais adequada para mercados com tendência; pode ter desempenho inferior em mercados laterais. Nesses casos, pode-se considerar otimizar os períodos das médias móveis ou usar outros indicadores de julgamento.

Otimização

-

Pode-se considerar a adição de outros indicadores, como o MACD, para refinar ainda mais o timing de entrada. Também é possível testar diferentes combinações de períodos das médias móveis.

-

Pode-se otimizar os parâmetros do ATR para ambos os lados. Por exemplo, ajustar o stop loss de 1 ATR para 1,5 ATR e o take profit de 4 ATR para 3 ATR, para verificar se obtém melhores retornos.

-

Pode-se testar o uso apenas das médias móveis, eliminando o indicador Stochastic RSI, para verificar se filtra mais ruídos e gera retornos mais estáveis.

-

Pode-se considerar a inclusão de mais condições para julgar a tendência, como a adição de um indicador de volume, garantindo a operação em tendências de grande escala.

Resumo

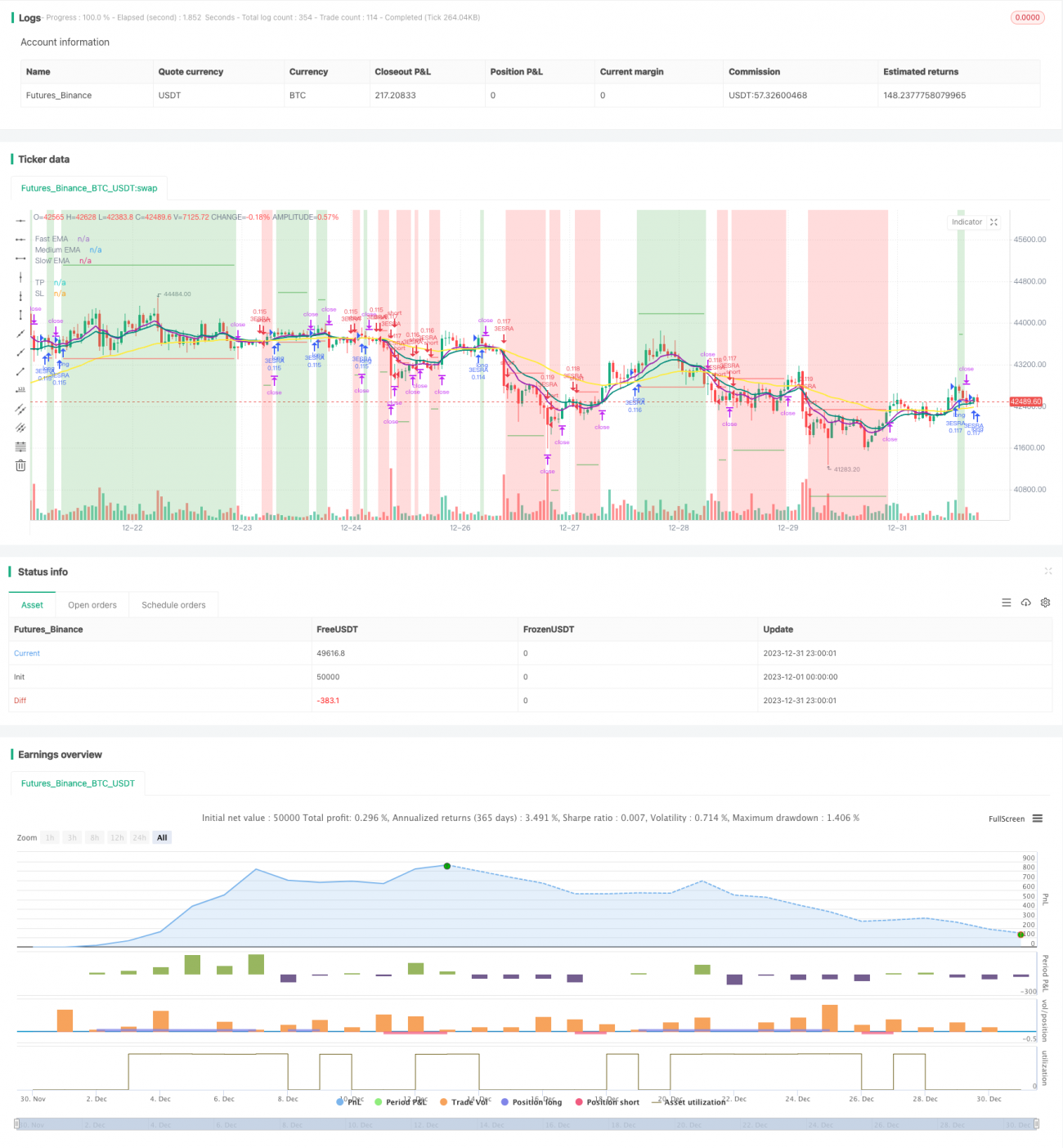

Esta estratégia utiliza de forma abrangente a Média Móvel Exponencial Tripla e o indicador Stochastic RSI para determinar a direção da tendência. Os sinais de entrada são bastante rigorosos, reduzindo efetivamente negociações desnecessárias. A definição dinâmica de stop loss e take profit com base no ATR confere adaptabilidade aos parâmetros da estratégia. Pelos resultados do backtest, a estratégia apresenta bom desempenho em mercados com tendência, com pequeno drawdown e retornos relativamente estáveis. Com otimizações adicionais, é possível obter resultados ainda melhores.

- 1