Chiến lược giao dịch kết hợp Đường trung bình động hàm mũ ba (TRIX) và Chỉ báo dao động ngẫu nhiên với Đường trung bình động hàm mũ mượt

Tổng quan

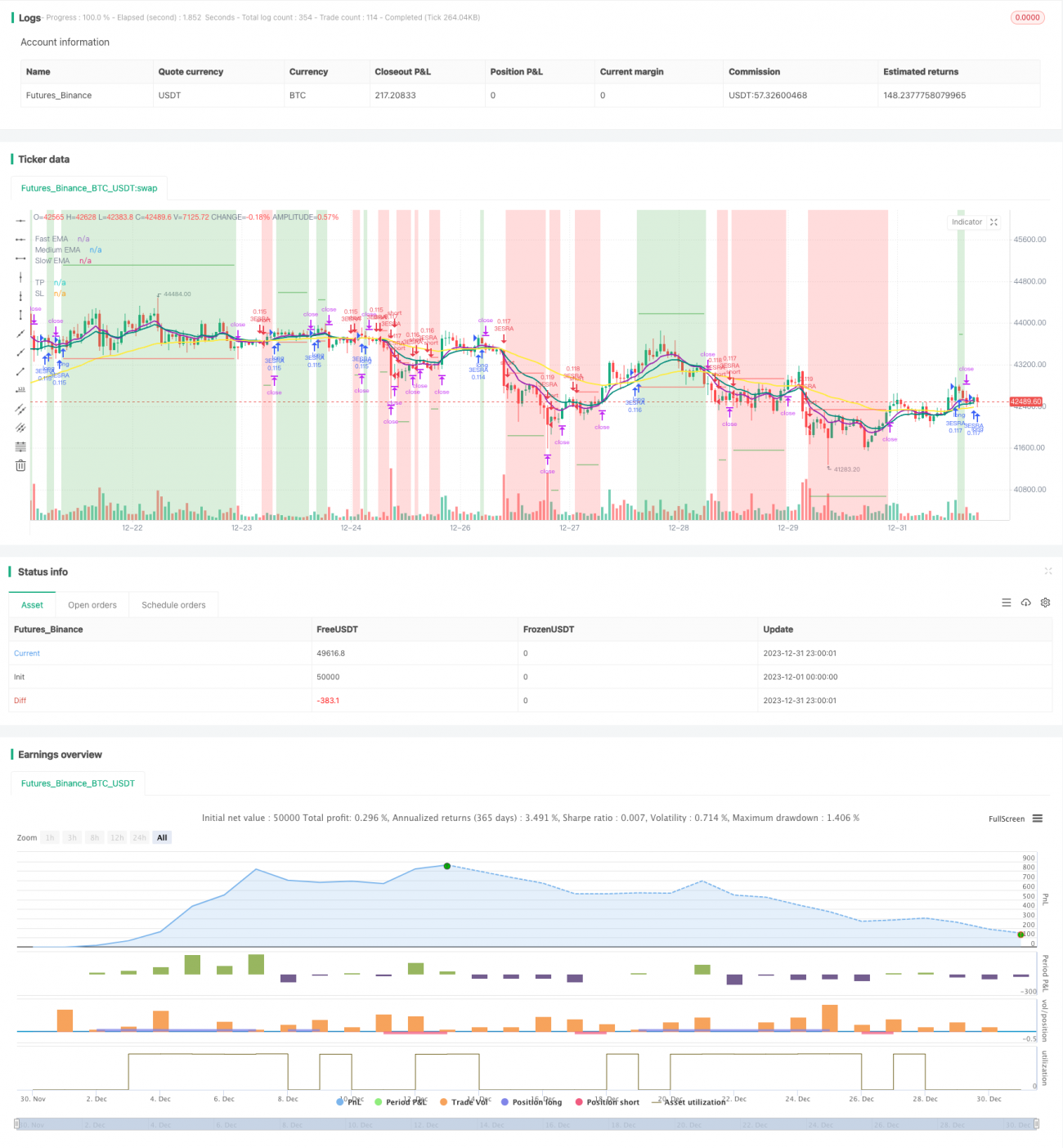

Chiến lược này là một chiến lược giao dịch theo xu hướng, kết hợp chỉ báo đường trung bình động hàm mũ ba lần (Triple Exponential Moving Average) và chỉ báo Stochastic RSI để tạo ra tín hiệu giao dịch. Khi đường trung bình động nhanh cắt lên trên đường trung bình động trung bình, và đường trung bình động trung bình cắt lên trên đường trung bình động chậm, thì đó là tín hiệu tăng giá; khi đường trung bình động nhanh cắt xuống dưới đường trung bình động trung bình, và đường trung bình động trung bình cắt xuống dưới đường trung bình động chậm, thì đó là tín hiệu giảm giá. Đồng thời, chiến lược này cũng sử dụng chỉ báo Stochastic RSI làm chỉ báo hỗ trợ để đánh giá.

Nguyên lý

-

Sử dụng đường trung bình động hàm mũ ba lần với các chu kỳ 8, 14 và 50 ngày. Khi đường EMA 8 ngày cắt lên trên đường EMA 14 ngày và đường EMA 14 ngày cắt lên trên đường EMA 50 ngày, tín hiệu tăng giá được tạo ra; ngược lại là tín hiệu giảm giá.

-

Sử dụng chỉ báo Stochastic RSI làm chỉ báo hỗ trợ. Cụ thể: Đầu tiên tính RSI 14 ngày, sau đó tính chỉ báo Stochastic dựa trên RSI, cuối cùng tính trung bình động đơn giản 3 ngày của chỉ báo Stochastic để có đường K và trung bình động đơn giản 3 ngày để có đường D. Khi đường K cắt lên trên đường D, đó là tín hiệu hỗ trợ tăng giá.

-

Khi có tín hiệu giao dịch, nếu giá cao hơn đường EMA 8 ngày thì vào lệnh mua; nếu giá thấp hơn đường EMA 8 ngày thì vào lệnh bán.

-

Cắt lỗ được đặt ở khoảng cách 1 lần ATR bên dưới/bên trên giá vào lệnh. Chốt lời được đặt ở khoảng cách 4 lần ATR bên trên/bên dưới giá vào lệnh.

Ưu điểm

-

Đường trung bình động là chỉ báo cơ bản, có thể theo dõi xu hướng thị trường hiệu quả. Đường trung bình động hàm mũ ba lần kết hợp nhiều chu kỳ, đảm bảo độ nhạy đối với cả xu hướng ngắn hạn và trung dài hạn.

-

Thêm Stochastic RSI làm chỉ báo hỗ trợ, có thể lọc các tín hiệu giả, nâng cao độ chính xác khi vào lệnh.

-

Sử dụng ATR để đặt cắt lỗ và chốt lời, có thể theo dõi động biến động thị trường, tránh cắt lỗ/chốt lời quá lớn hoặc quá nhỏ.

-

Các tham số của chiến lược này hợp lý, hoạt động tốt trong xu hướng lớn. Mức sụt giảm nhỏ, lợi nhuận tương đối ổn định, phù hợp với giao dịch dài hạn.

Rủi ro

-

Chiến lược kết hợp nhiều chỉ báo làm tăng rủi ro đảo chiều. Khi đường trung bình động và Stochastic RSI đưa ra tín hiệu trái ngược, có thể dẫn đến tín hiệu giao dịch sai. Lúc này cần chú ý đến xu hướng của bản thân giá.

-

Cài đặt cắt lỗ và chốt lời khá thận trọng, có thể bị phá vỡ trong điều kiện thị trường biến động mạnh, dẫn đến bị thoát lệnh và bỏ lỡ cơ hội xu hướng. Lúc này có thể điều chỉnh tham số ATR hoặc tăng bội số cắt lỗ/chốt lời.

-

Do sử dụng ba đường trung bình động, khi đường nhanh và đường trung bình đảo chiều, sẽ có độ trễ nhất định. Lúc này cần xem xét liệu bản thân giá có đảo chiều hay không để quyết định có vào lệnh hay không.

-

Chiến lược này chủ yếu phù hợp với thị trường có xu hướng, hoạt động kém trong thị trường đi ngang. Lúc này có thể cân nhắc tối ưu tham số chu kỳ của đường trung bình động hoặc sử dụng các chỉ báo đánh giá khác.

Tối ưu hóa

-

Có thể xem xét thêm các chỉ báo khác như MACD để tối ưu thời điểm vào lệnh. Cũng có thể thử nghiệm các tổ hợp tham số đường trung bình động khác nhau.

-

Có thể tối ưu tham số kiểm tra đa sắc thái của ATR. Ví dụ: điều chỉnh cắt lỗ từ 1 ATR lên 1,5 ATR, chốt lời từ 4 ATR xuống 3 ATR, xem liệu có thể đạt được lợi nhuận tốt hơn không.

-

Có thể thử nghiệm chỉ sử dụng đường trung bình động, bỏ chỉ báo Stochastic RSI, xem liệu có thể lọc được nhiều nhiễu hơn và đạt được lợi nhuận ổn định hơn không.

-

Có thể xem xét thêm nhiều điều kiện để đánh giá xu hướng, ví dụ như thêm chỉ báo khối lượng giao dịch, để đảm bảo giao dịch trong các xu hướng lớn.

Tổng kết

Chiến lược này kết hợp đường trung bình động hàm mũ ba lần và chỉ báo Stochastic RSI để xác định hướng xu hướng. Tín hiệu vào lệnh khá chặt chẽ, giúp giảm thiểu giao dịch không cần thiết. Cắt lỗ và chốt lời được thiết lập động theo ATR, giúp các tham số chiến lược có tính thích ứng. Từ kết quả backtest, chiến lược này hoạt động tốt trong thị trường có xu hướng, mức sụt giảm nhỏ, lợi nhuận tương đối ổn định. Thông qua tối ưu hóa thêm, có thể đạt được hiệu quả tốt hơn.

- 1