Chiến lược giao cắt đường trung bình động kết hợp động lượng đường chậm MACD

Tổng quan

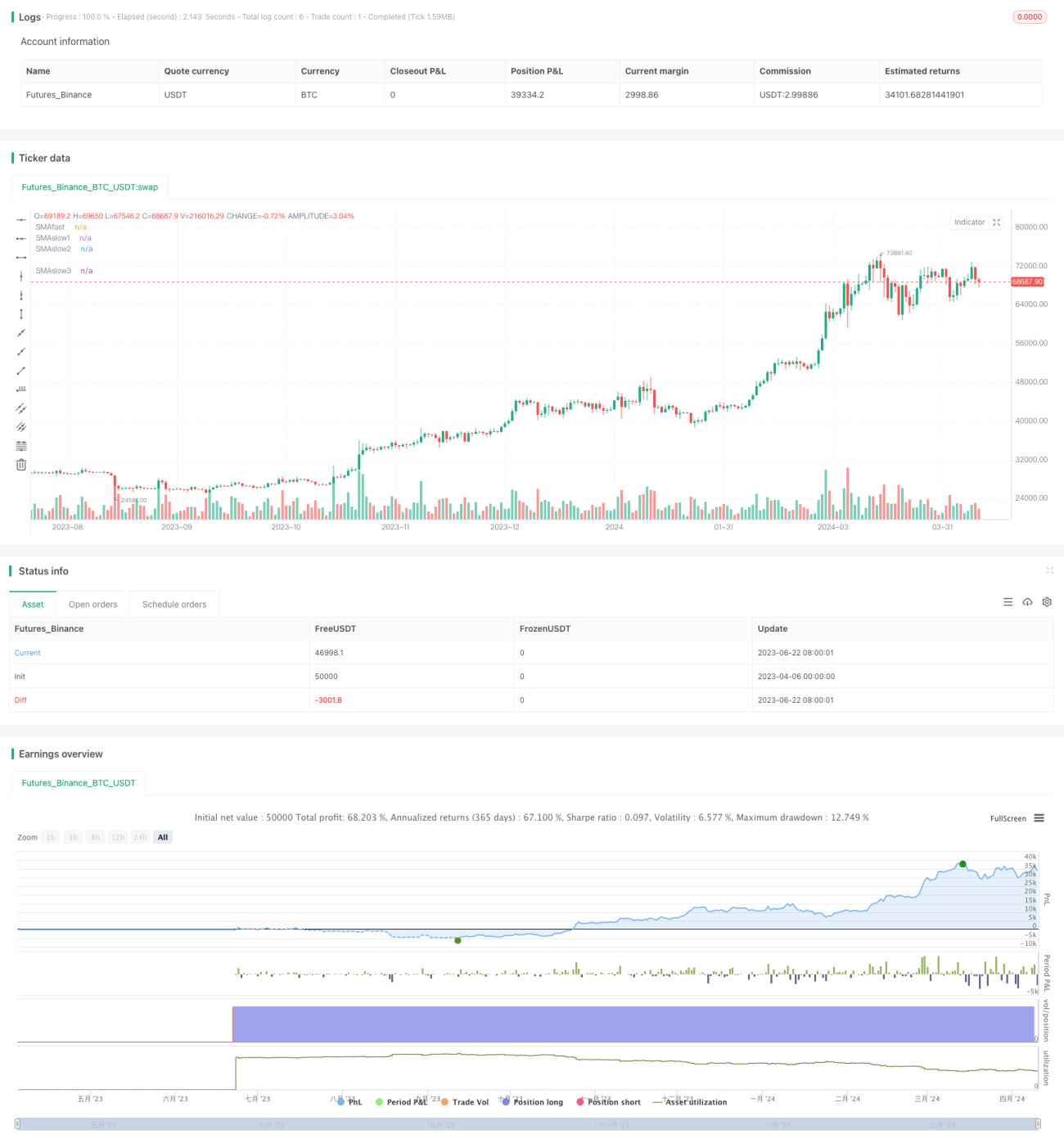

Chiến lược này sử dụng giao cắt đường trung bình động và chỉ báo MACD làm tín hiệu giao dịch chính. Chiến lược lấy giao cắt giữa đường trung bình động nhanh và nhiều đường trung bình động chậm làm tín hiệu mở lệnh, đồng thời kết hợp dấu hiệu dương/âm của biểu đồ cột MACD chậm làm cơ sở xác định xu hướng. Chiến lược thiết lập nhiều mức chốt lời và cắt lỗ khi mở lệnh, đồng thời liên tục điều chỉnh vị trí cắt lỗ khi thời gian nắm giữ tăng lên để khóa lợi nhuận.

Nguyên lý chiến lược

- Đường trung bình động nhanh cắt lên đường trung bình động chậm 1, đồng thời giá đóng cửa nằm trên đường trung bình động chậm 2, biểu đồ cột MACD lớn hơn 0, vào lệnh mua;

- Đường trung bình động nhanh cắt xuống đường trung bình động chậm 1, đồng thời giá đóng cửa nằm dưới đường trung bình động chậm 2, biểu đồ cột MACD nhỏ hơn 0, vào lệnh bán;

- Khi mở lệnh, thiết lập nhiều mức chốt lời và cắt lỗ, mức chốt lời được đặt dựa trên khẩu vị rủi ro, mức cắt lỗ được điều chỉnh liên tục theo thời gian nắm giữ, từng bước khóa lợi nhuận;

- Chu kỳ đường trung bình động, tham số MACD, mức chốt lời/cắt lỗ đều có thể linh hoạt điều chỉnh để thích ứng với các môi trường thị trường khác nhau.

Chiến lược này tận dụng giao cắt đường trung bình động để bắt xu hướng, đồng thời sử dụng chỉ báo MACD để xác nhận hướng, tăng cường độ tin cậy của việc xác định xu hướng. Việc thiết lập nhiều mức chốt lời và cắt lỗ giúp kiểm soát rủi ro và lợi nhuận tốt hơn.

Ưu điểm của chiến lược

- Giao cắt đường trung bình động là phương pháp bám xu hướng kinh điển, có thể kịp thời bắt được sự hình thành xu hướng;

- Sử dụng nhiều đường trung bình động giúp đánh giá toàn diện hơn về cường độ và tính bền vững của xu hướng;

- Chỉ báo MACD có thể nhận diện xu hướng và đánh giá động lượng hiệu quả, là sự bổ sung mạnh mẽ cho giao cắt đường trung bình động;

- Việc thiết lập nhiều mức chốt lời và cắt lỗ động vừa kiểm soát rủi ro, vừa cho phép lợi nhuận chạy, tăng cường tính ổn định của hệ thống;

- Tham số có thể điều chỉnh, khả năng thích ứng cao, có thể linh hoạt cài đặt theo các loại tài sản và khung thời gian khác nhau.

Rủi ro của chiến lược

- Giao cắt đường trung bình động có rủi ro trễ tín hiệu, có thể bỏ lỡ xu hướng sớm hoặc mua đuổi đỉnh;

- Việc cài đặt tham số không phù hợp có thể dẫn đến giao dịch quá mức hoặc thời gian nắm giữ quá dài, làm tăng chi phí và rủi ro;

- Việc đặt mức cắt lỗ quá tích cực có thể dẫn đến cắt lỗ sớm, mức chốt lời quá bảo thủ có thể ảnh hưởng đến lợi nhuận;

- Biến động xu hướng đột ngột hoặc thị trường bất thường có thể khiến chiến lược mất hiệu quả.

Những rủi ro này có thể được kiểm soát bằng cách tối ưu hóa tham số, điều chỉnh khối lượng, thêm các điều kiện bổ sung, v.v. Tuy nhiên, không có chiến lược nào có thể tránh hoàn toàn rủi ro, nhà đầu tư cần thận trọng.

Hướng tối ưu hóa chiến lược

- Có thể xem xét đưa thêm các chỉ báo khác như RSI, Bollinger Bands, v.v., để xác nhận thêm xu hướng và tín hiệu;

- Có thể tối ưu hóa chi tiết hơn việc thiết lập mức chốt lời và cắt lỗ, chẳng hạn như xem xét ATR hoặc chốt lời/cắt lỗ theo tỷ lệ phần trăm;

- Có thể điều chỉnh tham số động dựa trên biến động thị trường, tăng khả năng thích ứng;

- Có thể đưa vào mô-đun quản lý vị thế, điều chỉnh khối lượng dựa trên tình trạng rủi ro;

- Có thể tập hợp chiến lược, xây dựng danh mục chiến lược để phân tán rủi ro.

Thông qua tối ưu hóa và cải tiến liên tục, chiến lược có thể trở nên ổn định và đáng tin cậy hơn, thích ứng tốt hơn với môi trường thị trường thay đổi. Tuy nhiên, cần thận trọng khi tối ưu hóa, tránh quá khớp dữ liệu.

Tổng kết

Chiến lược này kết hợp giao cắt đường trung bình động và chỉ báo MACD, xây dựng một hệ thống giao dịch tương đối hoàn chỉnh. Thiết kế nhiều đường trung bình động và thao tác đa chiều tăng cường khả năng bắt xu hướng và kiểm soát rủi ro của hệ thống. Logic chiến lược rõ ràng, dễ hiểu và dễ triển khai, phù hợp để tối ưu hóa và cải tiến thêm. Tuy nhiên, trong ứng dụng thực tế vẫn cần thận trọng, chú ý kiểm soát rủi ro. Với tối ưu hóa và cấu hình hợp lý, chiến lược này có thể trở thành công cụ giao dịch ổn định và hiệu quả.

- 1