Advanced EMA Momentum Trend Trading Strategy

Overview

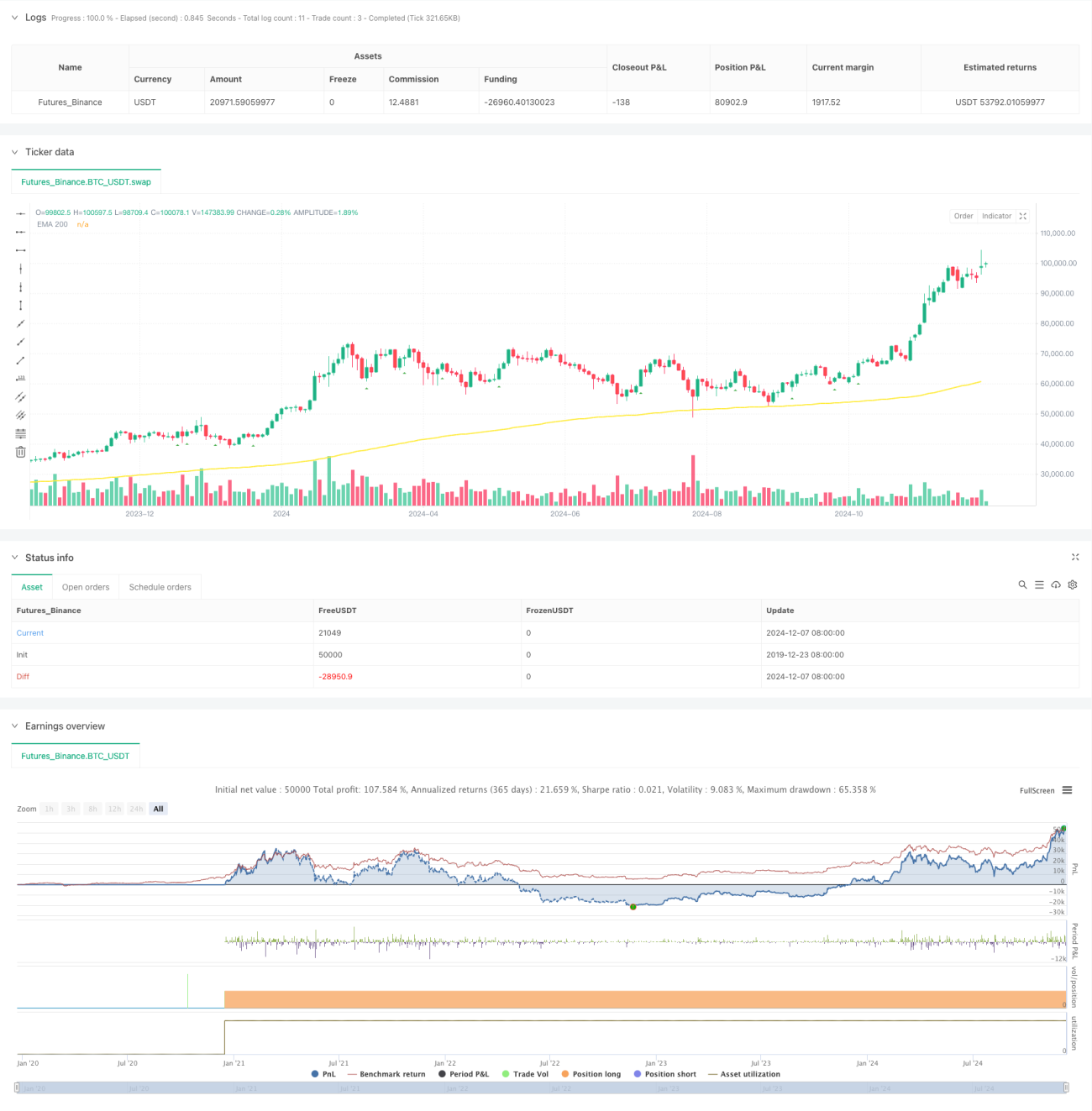

This strategy is a trend-following system based on Exponential Moving Average (EMA) and momentum indicators. It generates trading signals through the combination of momentum breakthrough signals and EMA trend filters, executing trades when market trends are clearly defined. The strategy includes a comprehensive risk management module, flexible trading time filters, and detailed statistical analysis functions to enhance stability and reliability.

Strategy Principles

The core logic of the strategy is based on several key elements:

- Momentum Signal Identification: Calculates momentum values over a user-defined period, generating long signals when momentum breaks above the threshold and short signals when it breaks below.

- EMA Trend Filter: Uses 200-period EMA as trend criterion, allowing long positions above EMA and short positions below.

- Time Filter: Configurable trading sessions with GMT timezone adjustment support for better adaptation to different market trading hours.

- Risk Control: Supports stop-loss and take-profit settings based on ATR or fixed percentage, with daily trade limits.

Strategy Advantages

- Strong Trend Following Capability: Effectively captures major trend movements through dual confirmation of EMA and momentum.

- Comprehensive Risk Management: Offers multiple stop-loss options, including ATR-based dynamic stops and fixed percentage stops.

- Thorough Statistical Analysis: Real-time tracking of multiple performance metrics, including long/short win rates and risk-reward ratios.

- Flexible Parameters: Key parameters can be optimized for different market characteristics.

Strategy Risks

-

Choppy Market Risk: May generate frequent false breakout signals in sideways markets.

Suggested Solution: Add oscillator filters or increase breakthrough thresholds. -

Slippage Risk: May face significant slippage during highly volatile periods.

Suggested Solution: Set reasonable stop-loss ranges and avoid trading during high volatility periods. -

Overtrading Risk: Frequent signals may lead to excessive trading.

Suggested Solution: Set appropriate daily trade limits.

Strategy Optimization Directions

- Dynamic Parameter Optimization: Automatically adjust momentum thresholds and EMA periods based on market volatility.

- Multi-timeframe Analysis: Add trend confirmation across multiple timeframes to improve signal reliability.

- Market Environment Recognition: Incorporate volatility analysis module to adapt parameters to different market conditions.

- Signal Strength Classification: Grade breakthrough signals and adjust position sizes based on signal strength.

Summary

This is a well-designed trend-following strategy that captures market opportunities through the combination of momentum breakthrough and EMA trends. The strategy features a complete risk management system and powerful statistical analysis functions, offering good practicality and scalability. Through continuous optimization and improvement, this strategy has the potential to maintain stable performance across different market environments.

- 1