ফুকুইজ ওক্টা-ইএমএ + ইচিমোকু

লেখক:চাওঝাং, তারিখঃ ২০২২-০৫-১৬ ১৭ঃ৪৩ঃ৫১ট্যাগঃইএমএ

এই কৌশলটি ৮টি ভিন্ন সময়ের ইএমএ এবং ইচিমোকু ক্লাউডের উপর ভিত্তি করে যা ১ ঘন্টা ৪ ঘন্টা এবং দৈনিক সময় ফ্রেমে ভাল কাজ করে।

# ইচিমোকুর সংক্ষিপ্ত ভূমিকা #

ইচিমোকু ক্লাউড প্রযুক্তিগত সূচকগুলির একটি সংগ্রহ যা সমর্থন এবং প্রতিরোধের স্তরগুলি, পাশাপাশি গতি এবং প্রবণতার দিক দেখায়। এটি একাধিক গড় গ্রহণ করে এবং একটি চার্টে তাদের প্লট করে এটি করে। এটি একটি

# ইএমএর সংক্ষিপ্ত ভূমিকা # একটি এক্সপোনেনশিয়াল মুভিং এভারেজ (ইএমএ) হ'ল একটি ধরণের মুভিং এভারেজ (এমএ) যা সাম্প্রতিকতম ডেটা পয়েন্টগুলিতে বৃহত্তর ওজন এবং তাত্পর্য রাখে। এক্সপোনেনশিয়াল মুভিং এভারেজকে এক্সপোনেনশিয়ালি ওয়েটেড মুভিং এভারেজও বলা হয়। একটি এক্সপোনেনশিয়ালি ওয়েটেড মুভিং এভারেজ একটি সাধারণ মুভিং এভারেজ (এসএমএ) এর চেয়ে সাম্প্রতিক মূল্য পরিবর্তনের প্রতি আরও উল্লেখযোগ্যভাবে প্রতিক্রিয়া দেখায়, যা সময়ের সমস্ত পর্যবেক্ষণের জন্য সমান ওজন প্রয়োগ করে।

# কিভাবে ব্যবহার করবেন # কৌশল নিজেই প্রবেশ পয়েন্ট দেবে, আপনি মনিটর এবং ম্যানুয়ালি মুনাফা নিতে পারেন ((প্রস্তাবিত), অথবা আপনি প্রস্থান সেটআপ ব্যবহার করতে পারেন।

ইএমএ (রঙ) = উত্থান প্রবণতা EMA (গ্রে) = bearish প্রবণতা

# শর্ত # ক্রয় = মেঘের উপরে সমস্ত ইমা (রঙ) । সব ইমা ধূসর হয়ে যায়।

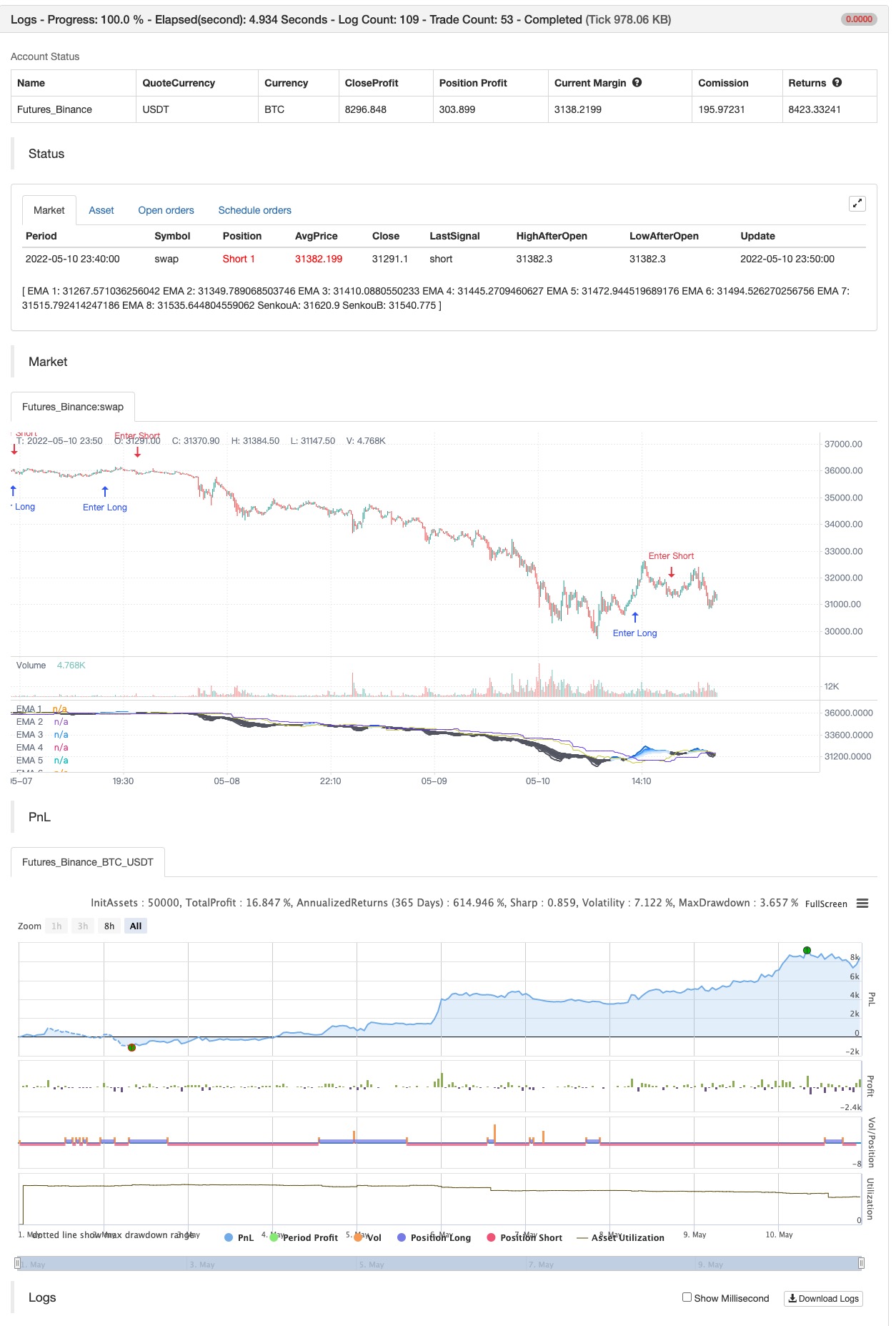

ব্যাকটেস্ট

/*backtest

start: 2022-05-01 00:00:00

end: 2022-05-10 23:59:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Fukuiz

//strategy(title='Fukuiz Octa-EMA + Ichimoku', shorttitle='Fuku octa strategy', overlay=true, process_orders_on_close=true,

// default_qty_type= strategy.cash , default_qty_value=1000, currency=currency.USD, initial_capital=10000 ,commission_type = strategy.commission.percent,commission_value=0.25)

//OCTA EMA ##################################################

// Functions

f_emaRibbon(_src, _e1, _e2, _e3, _e4, _e5, _e6, _e7, _e8) =>

_ema1 = ta.ema(_src, _e1)

_ema2 = ta.ema(_src, _e2)

_ema3 = ta.ema(_src, _e3)

_ema4 = ta.ema(_src, _e4)

_ema5 = ta.ema(_src, _e5)

_ema6 = ta.ema(_src, _e6)

_ema7 = ta.ema(_src, _e7)

_ema8 = ta.ema(_src, _e8)

[_ema1, _ema2, _ema3, _ema4, _ema5, _ema6, _ema7, _ema8]

showRibbon = input(true, 'Show Ribbon (EMA)')

ema1Len = input(5, title='EMA 1 Length')

ema2Len = input(11, title='EMA 2 Length')

ema3Len = input(15, title='EMA 3 Length')

ema4Len = input(18, title='EMA 4 Length')

ema5Len = input(21, title='EMA 5 Length')

ema6Len = input(24, title='EMA 6 Length')

ema7Len = input(28, title='EMA 7 Length')

ema8Len = input(34, title='EMA 8 Length')

[ema1, ema2, ema3, ema4, ema5, ema6, ema7, ema8] = f_emaRibbon(close, ema1Len, ema2Len, ema3Len, ema4Len, ema5Len, ema6Len, ema7Len, ema8Len)

//Plot

ribbonDir = ema8 < ema2

p1 = plot(ema1, color=showRibbon ? ribbonDir ? #1573d4 : color.new(#5d606b, 15) : na, linewidth=2, title='EMA 1')

p2 = plot(ema2, color=showRibbon ? ribbonDir ? #3096ff : color.new(#5d606b, 15) : na, linewidth=2, title='EMA 2')

plot(ema3, color=showRibbon ? ribbonDir ? #57abff : color.new(#5d606b, 15) : na, linewidth=2, title='EMA 3')

plot(ema4, color=showRibbon ? ribbonDir ? #85c2ff : color.new(#5d606b, 15) : na, linewidth=2, title='EMA 4')

plot(ema5, color=showRibbon ? ribbonDir ? #9bcdff : color.new(#5d606b, 30) : na, linewidth=2, title='EMA 5')

plot(ema6, color=showRibbon ? ribbonDir ? #b3d9ff : color.new(#5d606b, 30) : na, linewidth=2, title='EMA 6')

plot(ema7, color=showRibbon ? ribbonDir ? #c9e5ff : color.new(#5d606b, 30) : na, linewidth=2, title='EMA 7')

p8 = plot(ema8, color=showRibbon ? ribbonDir ? #dfecfb : color.new(#5d606b, 30) : na, linewidth=2, title='EMA 8')

fill(p1, p2, color.new(#1573d4, 85))

fill(p2, p8, color.new(#1573d4, 85))

//ichimoku##################################################

//color

colorblue = #3300CC

colorred = #993300

colorwhite = #FFFFFF

colorgreen = #CCCC33

colorpink = #CC6699

colorpurple = #6633FF

//switch

switch1 = input(false, title='Chikou')

switch2 = input(false, title='Tenkan')

switch3 = input(false, title='Kijun')

middleDonchian(Length) =>

lower = ta.lowest(Length)

upper = ta.highest(Length)

math.avg(upper, lower)

//Functions

conversionPeriods = input.int(9, minval=1)

basePeriods = input.int(26, minval=1)

laggingSpan2Periods = input.int(52, minval=1)

displacement = input.int(26, minval=1)

Tenkan = middleDonchian(conversionPeriods)

Kijun = middleDonchian(basePeriods)

xChikou = close

SenkouA = middleDonchian(laggingSpan2Periods)

SenkouB = (Tenkan[basePeriods] + Kijun[basePeriods]) / 2

//Plot

A = plot(SenkouA[displacement], color=color.new(colorpurple, 0), title='SenkouA')

B = plot(SenkouB, color=color.new(colorgreen, 0), title='SenkouB')

plot(switch1 ? xChikou : na, color=color.new(colorpink, 0), title='Chikou', offset=-displacement)

plot(switch2 ? Tenkan : na, color=color.new(colorred, 0), title='Tenkan')

plot(switch3 ? Kijun : na, color=color.new(colorblue, 0), title='Kijun')

fill(A, B, color=color.new(colorgreen, 90), title='Ichimoku Cloud')

//Buy and Sell signals

fukuiz = math.avg(ema2, ema8)

white = ema2 > ema8

gray = ema2 < ema8

buycond = white and white[1] == 0

sellcond = gray and gray[1] == 0

bullish = ta.barssince(buycond) < ta.barssince(sellcond)

bearish = ta.barssince(sellcond) < ta.barssince(buycond)

buy = bearish[1] and buycond and fukuiz > SenkouA[displacement] and fukuiz > SenkouB

sell = bullish[1] and sellcond and fukuiz > SenkouA[displacement] and fukuiz > SenkouB

sell2=ema2 < ema8

buy2 = white and fukuiz > SenkouA[displacement] and fukuiz > SenkouB

//$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

//Back test

startYear = input.int(defval=2017, title='Start Year', minval=2000, maxval=3000)

startMonth = input.int(defval=1, title='Start Month', minval=1, maxval=12)

startDay = input.int(defval=1, title='Start Day', minval=1, maxval=31)

endYear = input.int(defval=2023, title='End Year', minval=2000 ,maxval=3000)

endMonth = input.int(defval=12, title='End Month', minval=1, maxval=12)

endDay = input.int(defval=31, title='End Day', minval=1, maxval=31)

start = timestamp(startYear, startMonth, startDay, 00, 00)

end = timestamp(endYear, endMonth, endDay, 23, 59)

period() => time >= start and time <= end ? true : false

if buy2

strategy.entry("Enter Long", strategy.long)

else if sell2

strategy.entry("Enter Short", strategy.short)

- পরপর MACD গোল্ডেন এবং ডেথ ক্রস উপর ভিত্তি করে ট্রেডিং কৌশল

- উন্নত বোলিংজার ব্যান্ডস আরএসআই ট্রেডিং কৌশল

- ট্রিপল ইএমএ ক্রসওভার কৌশল

- এক্সপোনেন্সিয়াল মুভিং এভারেজ ক্রসওভার লিভারেজ কৌশল

- GM-8 & ADX ডাবল মুভিং এভারেজ কৌশল

- RSI/MACD/ATR এর সাথে EMA ক্রসওভার কৌশল উন্নত

- Z-Score ট্রেন্ড অনুসরণকারী কৌশল

- EMA-র দীর্ঘ প্রবেশের সাথে ঝুঁকি ব্যবস্থাপনা কৌশল

- ভিডব্লিউএপি ট্রেডিং কৌশল

- ওয়েভট্রেন্ড ক্রস লেজিবিয়ার কৌশল

- আলফা ট্রেডিংবট ট্রেডিং কৌশল

- গতির উপর ভিত্তি করে ZigZag

- ভিউম্যানচু সিফার বি + ডিভার্জেন্স কৌশল

- কনসেপ্ট ডুয়াল সুপারট্রেন্ড

- সুপার স্কালপার

- ব্যাকটেস্টিং- সূচক

- প্রচলিত

- এসএমএ বিটিসি খুনি

- এমএল সতর্কতা টেমপ্লেট

- বিরতি সহ ফিবোনাচি অগ্রগতি

- আরএসআই এমটিএফ ওব+ও

- সিসিআই এমটিএফ ওব+ও

- আরও স্মার্ট ম্যাকডি

- ওসিসি কৌশল R5.1

- বিয়ার মার্কেটে স্বাগতম [30 মিনিট]

- সিডবস

- পিভট পয়েন্ট উচ্চ নিম্ন মাল্টি টাইম ফ্রেম

- ভূত প্রবণতা ট্র্যাকিং কৌশল ডাটাবেস

- ভূত প্রবণতা কৌশলগত ট্রেসিং ব্যবসা পুস্তিকা

- ভূত ট্রেন্ড ট্র্যাকিং কৌশল

- রেইনবো ওসিলেটর