Beispiel für die Größe der Aktienkurvenposition

Schriftsteller:ChaoZhang, Datum: 2022-05-13 22:25:44Tags:Gemeinsame MarktorganisationSMA

Der Zweck der Aktienkurve ist es, das Risiko im Handel zu minimieren, wenn sich die Aktienkurve in einem Abwärtstrend befindet. Diese Strategie hat zwei Modi, um den Abwärtstrend der Aktienkurve zu bestimmen: Durch die Erstellung von zwei einfachen gleitenden Durchschnitten der Aktienkurve eines Portfolios - eine kurzfristige und eine längerfristige - und durch Handeln an ihren Kreuzungen. Wenn der schnelle SMA unter dem langsamen SMA liegt, wird ein Aktienabwärtstrend erkannt (smafastequity < smaslowewequity). Die zweite Methode besteht darin, die Kreuzungen des Eigenkapitals selbst mit dem längerfristigen SMA (Eigenkapital < smasloweequity) zu verwenden.

Wenn "Handel mit der Aktienkurve" aktiviert ist, wird die Positionsgröße um einen bestimmten Prozentsatz reduziert, wenn das Eigenkapital nach einer ausgewählten Regel "unter Wasser" ist.

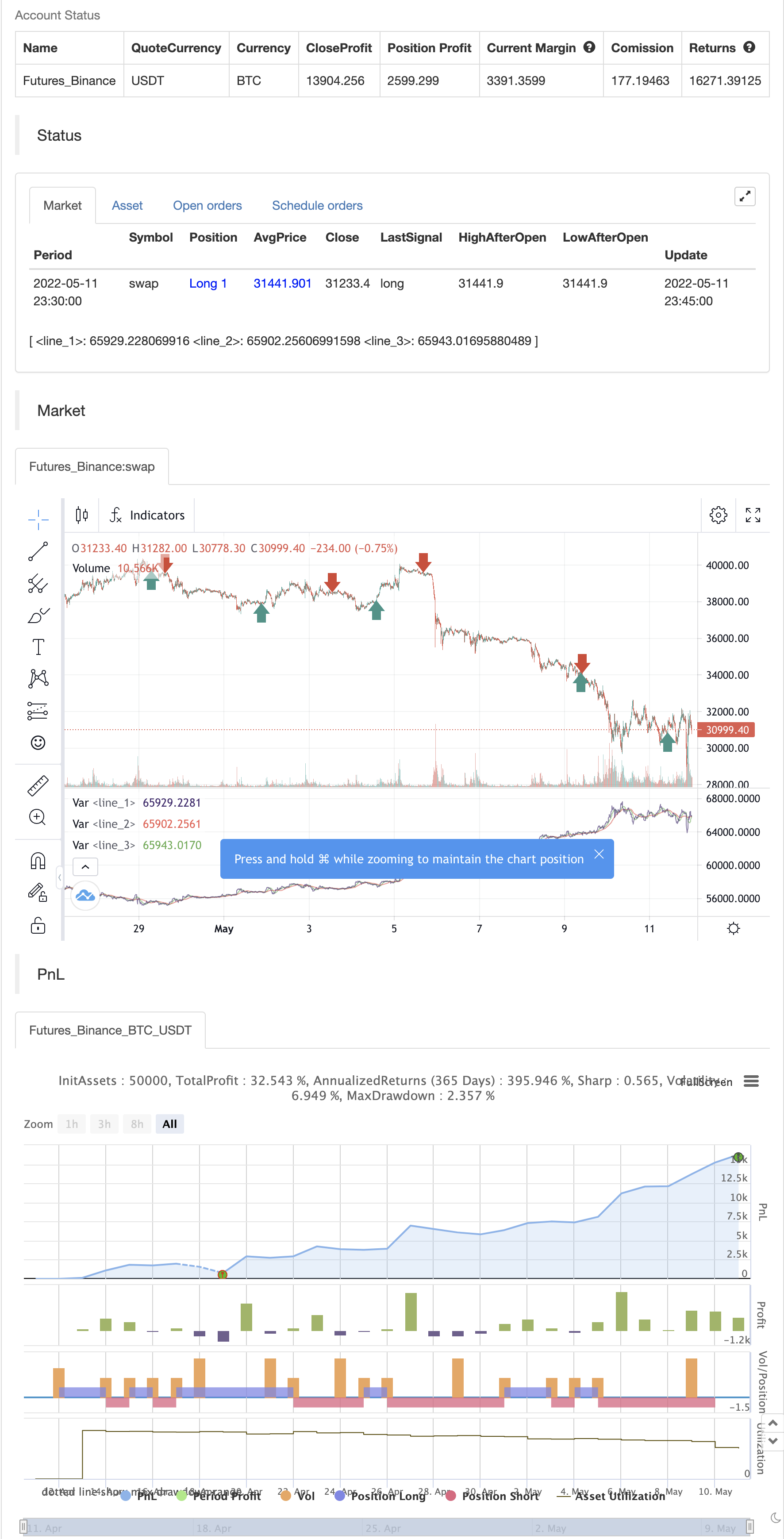

Zurückprüfung

/*backtest

start: 2022-04-12 00:00:00

end: 2022-05-11 23:59:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © shardison

//@version=5

//EXPLANATION

//"Trading the equity curve" as a risk management method is the

//process of acting on trade signals depending on whether a system’s performance

//is indicating the strategy is in a profitable or losing phase.

//The point of managing equity curve is to minimize risk in trading when the equity curve is in a downtrend.

//This strategy has two modes to determine the equity curve downtrend:

//By creating two simple moving averages of a portfolio's equity curve - a short-term

//and a longer-term one - and acting on their crossings. If the fast SMA is below

//the slow SMA, equity downtrend is detected (smafastequity < smaslowequity).

//The second method is by using the crossings of equity itself with the longer-period SMA (equity < smasloweequity).

//When "Reduce size by %" is active, the position size will be reduced by a specified percentage

//if the equity is "under water" according to a selected rule. If you're a risk seeker, select "Increase size by %"

//- for some robust systems, it could help overcome their small drawdowns quicker.

//strategy("Use Trading the Equity Curve Postion Sizing", shorttitle="TEC", default_qty_type = strategy.percent_of_equity, default_qty_value = 10, initial_capital = 100000)

//TRADING THE EQUITY CURVE INPUTS

useTEC = input.bool(true, title="Use Trading the Equity Curve Position Sizing")

defulttraderule = useTEC ? false: true

initialsize = input.float(defval=10.0, title="Initial % Equity")

slowequitylength = input.int(25, title="Slow SMA Period")

fastequitylength = input.int(9, title="Fast SMA Period")

seedequity = 100000 * .10

if strategy.equity == 0

seedequity

else

strategy.equity

slowequityseed = strategy.equity > seedequity ? strategy.equity : seedequity

fastequityseed = strategy.equity > seedequity ? strategy.equity : seedequity

smaslowequity = ta.sma(slowequityseed, slowequitylength)

smafastequity = ta.sma(fastequityseed, fastequitylength)

equitycalc = input.bool(true, title="Use Fast/Slow Avg", tooltip="Fast Equity Avg is below Slow---otherwise if unchecked uses Slow Equity Avg below Equity")

sizeadjstring = input.string("Reduce size by (%)", title="Position Size Adjustment", options=["Reduce size by (%)","Increase size by (%)"])

sizeadjint = input.int(50, title="Increase/Decrease % Equity by:")

equitydowntrendavgs = smafastequity < smaslowequity

slowequitylessequity = strategy.equity < smaslowequity

equitymethod = equitycalc ? equitydowntrendavgs : slowequitylessequity

if sizeadjstring == ("Reduce size by (%)")

sizeadjdown = initialsize * (1 - (sizeadjint/100))

else

sizeadjup = initialsize * (1 + (sizeadjint/100))

c = close

qty = 100000 * (initialsize / 100) / c

if useTEC and equitymethod

if sizeadjstring == "Reduce size by (%)"

qty := (strategy.equity * (initialsize / 100) * (1 - (sizeadjint/100))) / c

else

qty := (strategy.equity * (initialsize / 100) * (1 + (sizeadjint/100))) / c

//EXAMPLE TRADING STRATEGY INPUTS

CMO_Length = input.int(defval=9, minval=1, title='Chande Momentum Length')

CMO_Signal = input.int(defval=10, minval=1, title='Chande Momentum Signal')

chandeMO = ta.cmo(close, CMO_Length)

cmosignal = ta.sma(chandeMO, CMO_Signal)

SuperTrend_atrPeriod = input.int(10, "SuperTrend ATR Length")

SuperTrend_Factor = input.float(3.0, "SuperTrend Factor", step = 0.01)

Momentum_Length = input.int(12, "Momentum Length")

price = close

mom0 = ta.mom(price, Momentum_Length)

mom1 = ta.mom( mom0, 1)

[supertrend, direction] = ta.supertrend(SuperTrend_Factor, SuperTrend_atrPeriod)

stupind = (direction < 0 ? supertrend : na)

stdownind = (direction < 0? na : supertrend)

//TRADING CONDITIONS

longConditiondefault = ta.crossover(chandeMO, cmosignal) and (mom0 > 0 and mom1 > 0 and close > stupind) and defulttraderule

if (longConditiondefault)

strategy.entry("DefLong", strategy.long)

shortConditiondefault = ta.crossunder(chandeMO, cmosignal) and (mom0 < 0 and mom1 < 0 and close < stdownind) and defulttraderule

if (shortConditiondefault)

strategy.entry("DefShort", strategy.short)

longCondition = ta.crossover(chandeMO, cmosignal) and (mom0 > 0 and mom1 > 0 and close > stupind) and useTEC

if (longCondition)

strategy.entry("AdjLong", strategy.long)

shortCondition = ta.crossunder(chandeMO, cmosignal) and (mom0 < 0 and mom1 < 0 and close < stdownind) and useTEC

if (shortCondition)

strategy.entry("AdjShort", strategy.short)

plot(strategy.equity)

plot(smaslowequity, color=color.new(color.red, 0))

plot(smafastequity, color=color.new(color.green, 0))

- NMVOB-S

- Bollinger Bands Stochastischer Oszillator-Strategie

- Z-Score mit Signalen

- TMA-Überlagerung

- Bollinger-Bänder Standardabweichungs-Breakout-Strategie

- Hurst künftige Linien der Abgrenzungsstrategie

- Mobo-Bänder

- Indikator für die Druckdynamik

- Nik Stoch

- Doppelzeitliche Dynamikstrategie

- MTF Ob+Os der KMU

- Ein intelligenter MACD

- Strategie des OCC R5.1

- Willkommen auf dem Bärenmarkt.

- - Ich weiß.

- Drehpunkte Hoch-Niedrig-Multi-Zeitrahmen

- Geistertrends verfolgen Strategiedatenbanken

- Geistertrends verfolgen Strategien für die Geschäftsbank

- Geistertrend-Verfolgungsstrategien

- Regenbogen-Oszillator

- KLineChart-Demo

- Villa Dynamic Pivot Supertrend-Strategie

- Crodls Supertrend

- RSI von zdmre

- FTL - Bereichsfilter X2 + EMA + UO

- BRAHMASTRA

- Mobo-Bänder

- SAR + 3SMMA mit SL & TP

- SSS

- Vorlage für Warnmeldungen für den Mondstart [Indikator]