Multi-Timeframe-Handelsstrategie auf Basis von RSI und gleitenden Durchschnitten

Überblick

Der Kerngedanke dieser Strategie besteht darin, gleichzeitig den Relative-Stärke-Index (RSI) und gleitende Durchschnitte unterschiedlicher Zeiträume zu nutzen, um Trendumkehrpunkte zu identifizieren. So können mittel- bis langfristige Trends verfolgt und gleichzeitig kurzfristige Trades durchgeführt werden. Die Strategie kombiniert verschiedene Handelssignale, um die Erfolgsquote zu erhöhen.

Strategieprinzip

- Berechnung des RSI-Indikators sowie des schnellen EMA (Exponential Moving Average) und des langsamen WMA (Weighted Moving Average).

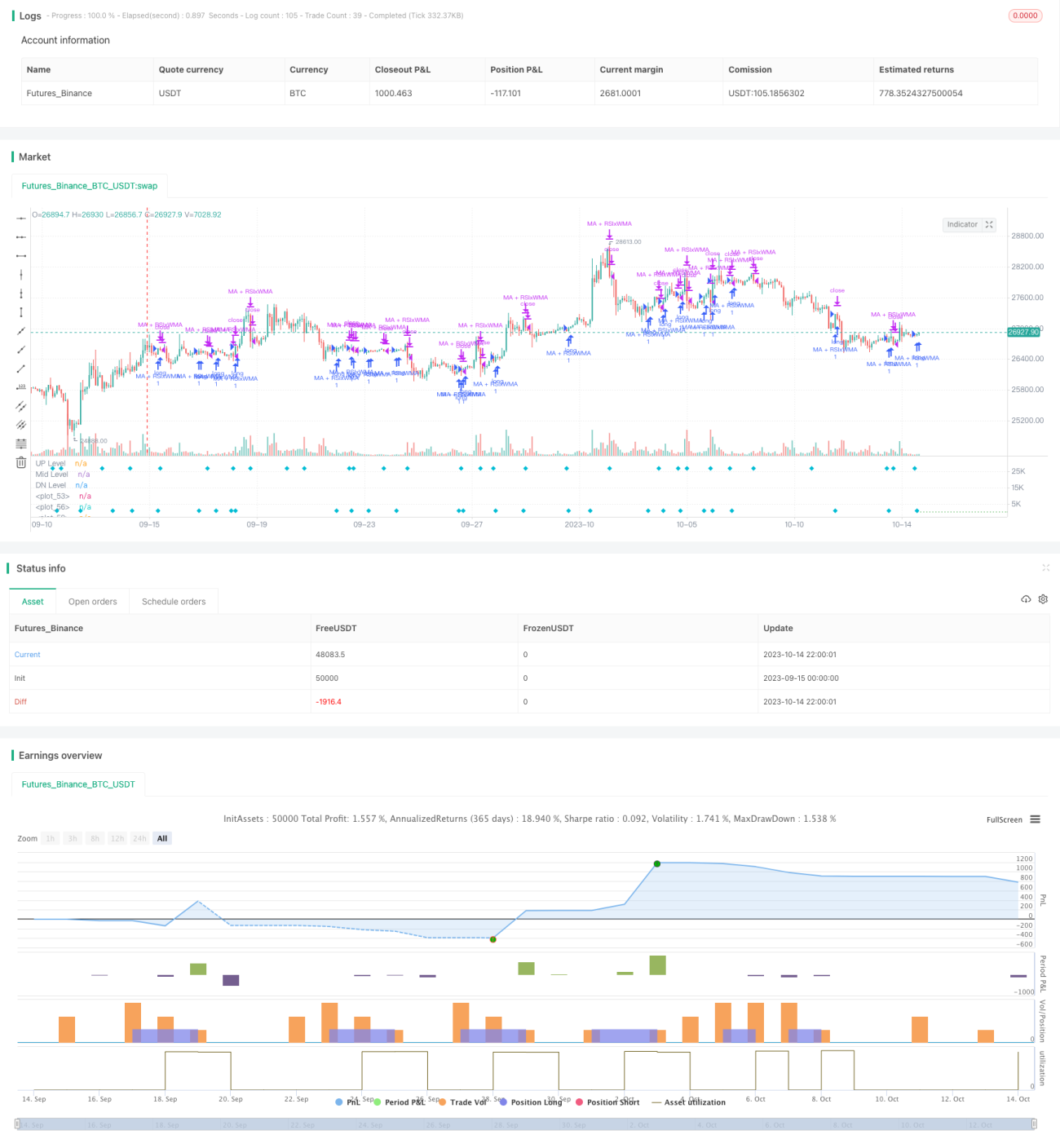

- Wenn die RSI-Linie die WMA-Linie durchbricht, wird ein Kauf-/Verkaufssignal generiert.

- Wenn der schnelle EMA den langsamen WMA durchbricht, wird ein Kauf-/Verkaufssignal generiert.

- Wenn sowohl RSI als auch EMA gleichzeitig den WMA durchbrechen, entsteht ein starkes Kauf-/Verkaufssignal.

- Zusätzlich kann ein Ausbruch des Preises durch einen unterstützenden gleitenden Durchschnitt das Hauptsignal verstärken.

- Setzen von Stop-Loss- und Take-Profit-Bedingungen.

Diese Strategie kombiniert Ausbruchssignale mehrerer technischer Indikatoren und nutzt gleitende Durchschnitte mit unterschiedlichen Parametern, um Trends verschiedener Zeiträume zu identifizieren, wodurch die Zuverlässigkeit erhöht wird. Der RSI bewertet überkaufte/überverkaufte Zustände, der schnelle EMA den kurzfristigen Trend, der langsame WMA den mittelfristigen Trend, und der Preisausbruch durch den unterstützenden gleitenden Durchschnitt bestätigt den Trend. Die Kombination mehrerer Signale verbessert die Effektivität der Strategie.

Vorteile

- Durch die Umkehreigenschaften des RSI können Chancen in überkauften/überverkauften Bereichen genutzt werden.

- Der unterstützende gleitende Durchschnitt dient als Trendfilter und vermeidet Fehlausbrüche.

- Die Kombination mehrerer Zeiträume ermöglicht sowohl die Verfolgung langfristiger Trends als auch die Erfassung kurzfristiger Chancen.

- Die Integration mehrerer Indikatorsignale kann die Erfolgsquote erhöhen.

- Die Implementierung von Stop-Loss- und Take-Profit-Strategien ermöglicht ein aktives Risikomanagement.

Risikoanalyse

- Der RSI neigt zu Fehlsignalen, die durch den unterstützenden gleitenden Durchschnitt gefiltert werden müssen.

- Rücksetzer innerhalb eines übergeordneten Trends können gegenläufige Handelssignale auslösen – hier ist Vorsicht geboten.

- Die Parametereinstellungen (z. B. RSI-Zeitraum, Längen der gleitenden Durchschnitte) müssen optimiert werden.

- Stop-Loss-Punkte sind sorgfältig zu setzen, um nicht in Verlustpositionen gefangen zu werden.

Diese Risiken können durch Parameteroptimierung, strenge Stop-Loss-Regeln und die Berücksichtigung des übergeordneten Trends gemindert werden.

Optimierungsmöglichkeiten

- Optimierung der RSI-Parameter zur Ermittlung der optimalen Periodenlänge.

- Testen verschiedener Kombinationen gleitender Durchschnitte.

- Einbindung eines Volatilitätsindikators wie ATR zur dynamischen Anpassung von Stop-Loss und Take-Profit.

- Hinzufügen eines Volumenmanagement-Moduls.

- Einsatz maschinellen Lernens zur Parameteroptimierung und Bewertung der Signalqualität.

Zusammenfassung

Diese Strategie vereint Trendfolge- und Extremumkehr-Ansätze und nutzt eine Multi-Zeitrahmen-Analyse sowie eine Kombination mehrerer Indikatoren, um die Erfolgswahrscheinlichkeit zu steigern. Entscheidend sind eine gute Risikokontrolle, optimierte Parametereinstellungen und die Berücksichtigung des übergeordneten Trends. Insgesamt ist die Strategie praxistauglich und anpassungsfähig. Zukünftig können weitere fortgeschrittene Techniken zur Qualitätssteigerung eingesetzt werden.

- 1