Estrategia de trading de momentum con múltiples MA

Resumen

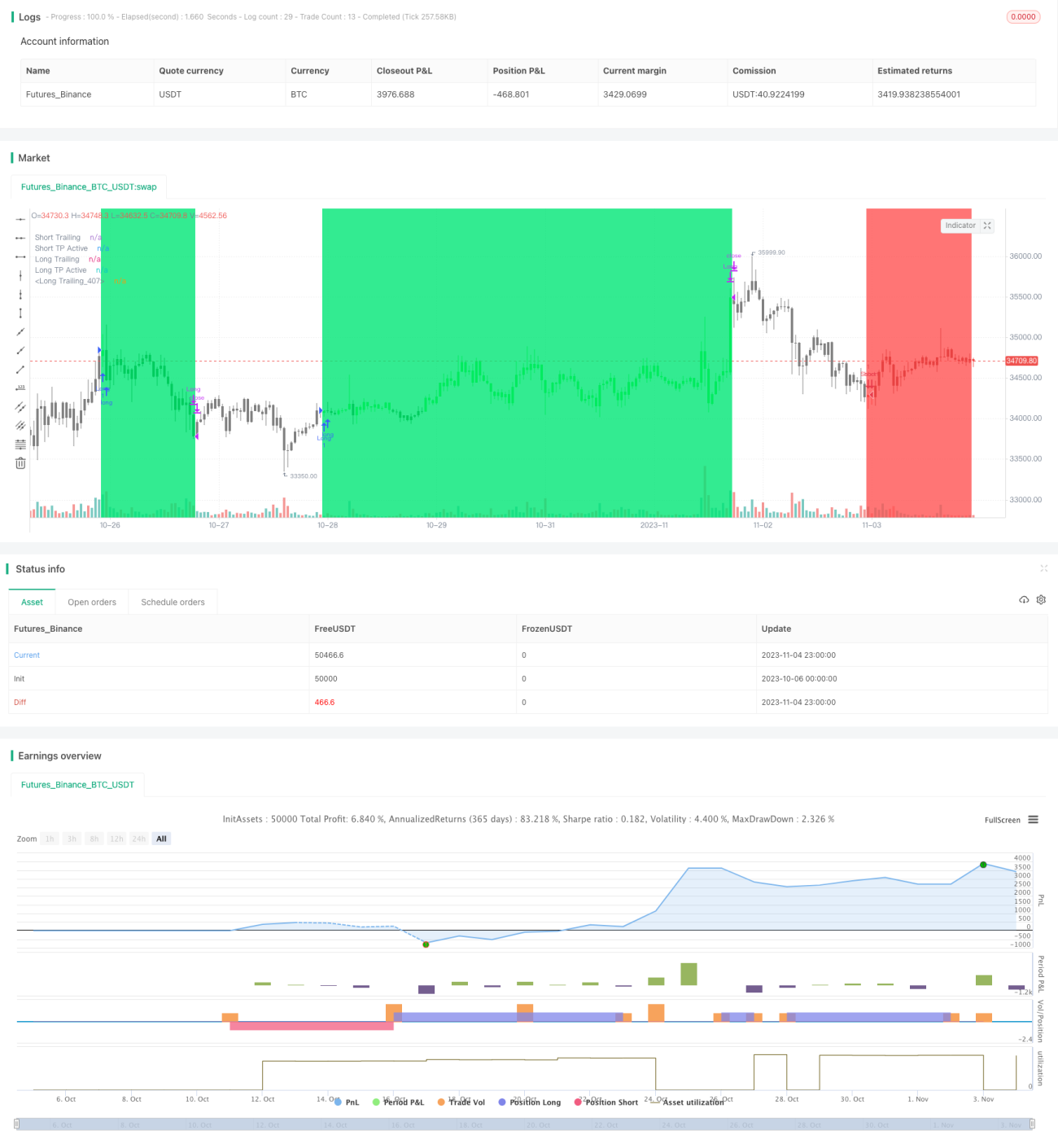

Esta estrategia de trading combina múltiples medias móviles e indicadores de momentum para identificar la dirección y fuerza de una tendencia, abriendo posiciones al inicio de la tendencia y posteriormente utilizando trailing stop, trailing take profit, etc., para optimizar beneficios y controlar riesgos. El objetivo es capturar movimientos de precio significativos en tendencias de mediano y largo plazo.

Principio de la Estrategia

-

Se utilizan dos conjuntos de medias móviles con diferentes parámetros para construir líneas rápidas y lentas:

- La línea rápida está compuesta por una media móvil exponencial de 5 períodos y una media móvil ponderada de 25 períodos, representando la tendencia de corto plazo.

- La línea lenta está compuesta por una media móvil exponencial de 28 períodos y una media móvil ponderada de 72 períodos, representando la tendencia de mediano-largo plazo.

-

Cuando la línea rápida cruza por encima de la línea lenta, indica que la tendencia de corto plazo comienza a ser más fuerte que la de mediano-largo plazo, siendo una señal de entrada.

-

Se combina con el indicador de momentum RSI, entrando solo cuando el RSI está en niveles bajos (señal de compra) o altos (señal de venta), para filtrar falsas rupturas.

-

Una vez dentro, se utiliza un trailing stop para limitar las pérdidas y un trailing take profit para asegurar las ganancias.

-

Cuando la línea rápida cruza por debajo de la línea lenta, advierte una reversión de tendencia, momento en el que se sale mediante el stop o el take profit.

Análisis de Ventajas

- La combinación de doble media móvil filtra el ruido e identifica la dirección y fuerza del tramo medio de la tendencia.

- Solo se abren posiciones al inicio de la tendencia, evitando pérdidas innecesarias por falsas rupturas.

- El indicador de momentum combinado filtra las entradas, mejorando la calidad de las mismas.

- El trailing stop limita las pérdidas individuales, reduciendo el impacto de pérdidas puntuales.

- El trailing take profit permite obtener ganancias considerables y agregar beneficios en condiciones de mercado favorables.

Análisis de Riesgos

- La doble media móvil tiene rezago en los puntos de inflexión de la tendencia, pudiendo perder oportunidades de reversión.

- Se pueden acortar los períodos de las medias móviles para hacerlas más sensibles.

- Las falsas rupturas pueden provocar entradas innecesarias.

- Se pueden añadir más indicadores de filtro.

- La distancia del stop o take profit no está optimizada, pudiendo ser demasiado amplia o demasiado ajustada.

- Se puede optimizar mediante backtesting para encontrar la mejor distancia.

- Estrategia direccional, solo apta para mercados en tendencia.

- Se puede decidir si usar la estrategia según las condiciones generales del mercado.

Direcciones de Optimización

- Optimizar los parámetros de las medias móviles para encontrar la mejor combinación que represente la tendencia.

- Añadir indicadores de filtro de tendencia, como el ATR dinámico para stops, el indicador de flujo de dinero, etc.

- Optimizar los parámetros de stop y take profit para encontrar la mejor combinación.

- Añadir juicio sobre grandes movimientos del mercado para decidir si activar la estrategia.

- Incorporar juicio multitemporal, utilizando la dirección de la tendencia de mayor marco temporal para guiar la estrategia de corto plazo.

Resumen

Esta estrategia integra medias móviles e indicadores de momentum, con el objetivo de identificar y realizar entradas tempranas en tendencias emergentes, gestionando el riesgo y los beneficios mediante stops y take profits móviles. Aunque aún es necesario optimizar parámetros y reglas para adaptarse a un rango más amplio de condiciones de mercado, ya cuenta con un marco básico y una dirección para capturar tendencias de mediano y largo plazo. Mediante una optimización continua, esta estrategia tiene el potencial de convertirse en un sistema de seguimiento de tendencias estable y eficiente.

- 1