Estrategia de seguimiento de tendencias basada en la media móvil adaptativa

Resumen

Esta estrategia utiliza el indicador de Media Móvil Adaptativa de Kaufman (KAMA) para diseñar un sistema de trading de seguimiento de tendencia. El sistema puede seguir rápidamente la tendencia cuando se forma, y filtrar el ruido en mercados laterales. Además, el sistema integra el sistema de Parabólico SAR (PSAR) y el Stop Loss Dinámico basado en el Rango Verdadero Promedio (ATR Trailing Stop) como mecanismos de stop loss, proporcionando una sólida capacidad de control de riesgos.

Principio de la Estrategia

-

La longitud del indicador KAMA se ajusta dinámicamente según la volatilidad del mercado en el período reciente. Cuando el cambio de precio es mayor que el ruido reciente, la ventana de la EMA se acorta; cuando el cambio de precio es menor que el ruido reciente, la ventana de la EMA se alarga. Esto permite que KAMA siga rápidamente la tendencia y filtre el ruido en mercados laterales.

-

El sistema determina principalmente la dirección de la tendencia basándose en la KAMA más rápida (KAMA 1). Cuando KAMA 1 sube, se toma una posición larga; cuando baja, se toma una posición corta. Para filtrar falsos rompimientos, se establece un filtro KAMA. Solo se genera una señal de trading cuando el cambio de KAMA 1 supera una desviación estándar de la volatilidad reciente.

-

En cuanto al stop loss, el sistema ofrece tres opciones de stop loss: basado en la reversión de KAMA, reversión de PSAR y stop loss dinámico ATR. Los inversores pueden personalizar y elegir una o una combinación de ellas.

Análisis de Ventajas

-

El diseño único del indicador KAMA permite que el sistema detecte rápidamente nuevas tendencias, detenga las operaciones en mercados laterales, controle efectivamente la frecuencia de trading y reduzca el deslizamiento y las comisiones innecesarias.

-

El sistema incorpora múltiples mecanismos de stop loss. Los inversores pueden elegir el esquema de stop loss adecuado según su tolerancia al riesgo, controlando eficazmente las pérdidas por operación.

-

El sistema se basa completamente en indicadores y líneas de stop loss, evitando el problema común de entrar en operaciones desplazadas.

-

Los múltiples parámetros y combinaciones de condiciones ofrecen un gran espacio para la personalización del sistema. Los usuarios pueden optimizarlo según el activo y el período específicos.

Análisis de Riesgos

-

El sistema no considera el riesgo sistémico, por lo que no puede controlar eficazmente las pérdidas en condiciones extremas del mercado.

-

Los parámetros del sistema pueden necesitar ajustes según diferentes activos y períodos; de lo contrario, se obtendrán resultados demasiado agresivos o demasiado conservadores.

-

Si se depende únicamente del indicador KAMA como stop loss, es fácil quedar atrapado en mercados laterales. Esto requiere combinarlo con PSAR o stop loss dinámico ATR para resolverlo.

Direcciones de Optimización

-

Agregar indicadores de filtro de tendencia, como ADX o volatilidad implícita, para evitar señales falsas durante períodos de lateralidad y transición de tendencia.

-

Optimizar y realizar backtesting de los parámetros para un solo activo y un período fijo, mejorando la estabilidad. Las dimensiones de optimización incluyen la combinación de parámetros KAMA, parámetros de stop loss, etc.

-

Intentar utilizar modelos de Machine Learning en lugar de la optimización de parámetros. Entrenar redes neuronales o modelos de árbol de decisión con grandes cantidades de datos históricos para determinar los momentos de compra/venta y los stop loss.

-

Probar la estrategia en otros activos, como criptomonedas. Esto puede requerir ajustar los parámetros o agregar otros indicadores auxiliares.

Resumen

Esta estrategia integra la determinación de tendencia de KAMA y múltiples métodos de stop loss, pudiendo seguir eficazmente la dirección de la tendencia y controlar el riesgo. La singularidad del indicador KAMA permite que la estrategia detecte rápidamente la dirección de nuevas tendencias y evite problemas de falsos rompimientos. Los parámetros personalizables y optimizables ofrecen un gran margen para ajustes individualizados. Si se optimizan los parámetros para un solo activo y un solo período, y se integran modelos de Machine Learning, es probable que se mejore aún más el rendimiento de la estrategia.

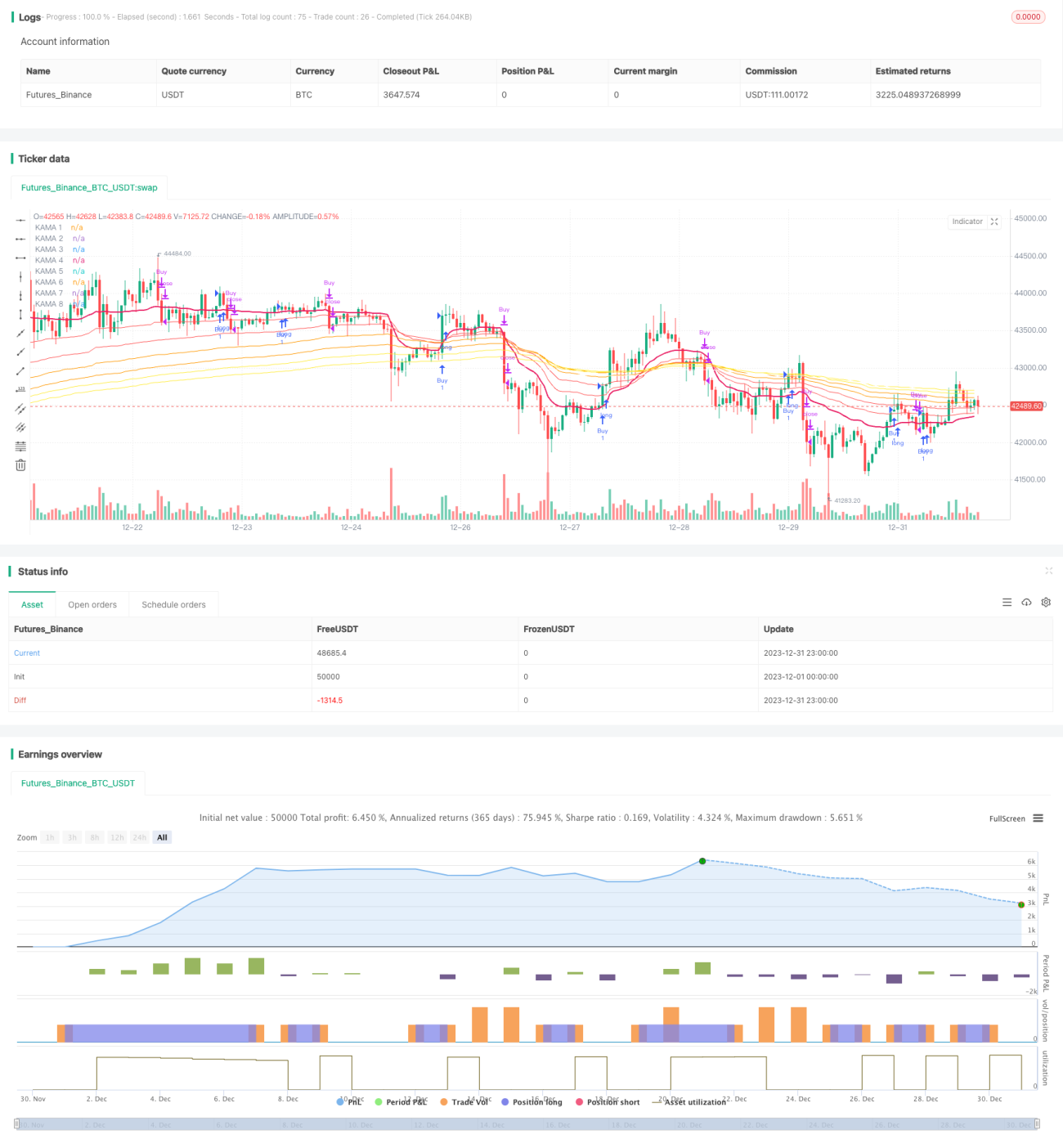

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © BenHampson

// @version=4

// Credit to:- 1