Estrategia de trading RSI con separación de posiciones largas y cortas

Resumen

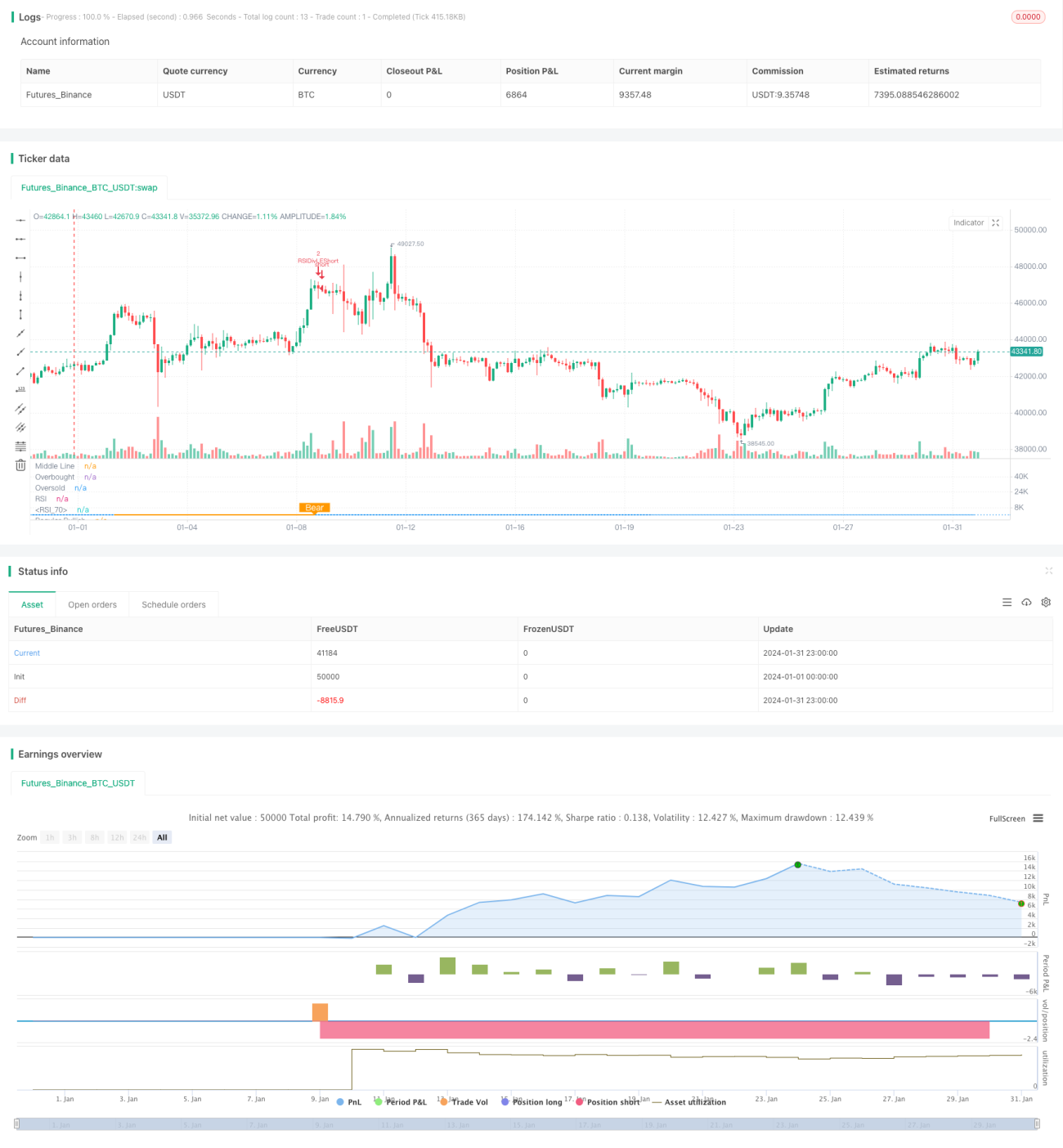

Esta estrategia identifica fenómenos de divergencia alcista y bajista mediante el indicador RSI, tomando decisiones de trading basadas en ello. Su idea central es: cuando el precio alcanza un nuevo mínimo pero el RSI alcanza un nuevo máximo (divergencia alcista), se forma una señal de "divergencia alcista" que indica que se ha formado un suelo, por lo que se abre una posición larga; cuando el precio alcanza un nuevo máximo pero el RSI alcanza un nuevo mínimo (divergencia bajista), se forma una señal de "divergencia bajista" que indica que se ha formado un techo, por lo que se abre una posición corta.

Principio de la estrategia

Esta estrategia utiliza principalmente el indicador RSI para identificar los fenómenos de divergencia entre el precio y el RSI. El método específico es el siguiente:

- Se utiliza el indicador RSI con período 13, tomando como fuente el precio de cierre.

- Para la divergencia alcista, el rango de retroceso hacia la izquierda es de 14 días y hacia la derecha de 2 días.

- Para la divergencia bajista, el rango de retroceso hacia la izquierda es de 47 días y hacia la derecha de 1 día.

- Cuando el precio forma un mínimo más bajo, pero el RSI forma un mínimo más alto, se cumple la condición de divergencia alcista y se genera una señal de compra.

- Cuando el precio forma un máximo más alto, pero el RSI forma un máximo más bajo, se cumple la condición de divergencia bajista y se genera una señal de venta.

Al identificar los fenómenos de divergencia entre el precio y el RSI, se pueden capturar de forma anticipada los puntos de inflexión en la tendencia del precio, tomando decisiones de trading basadas en ello.

Ventajas de la estrategia

Esta estrategia presenta principalmente las siguientes ventajas:

- Identifica los fenómenos de divergencia entre el precio y el RSI, lo que permite anticipar los puntos de inflexión de la tendencia del precio y aprovechar las oportunidades de trading.

- Al basarse en el análisis de indicadores, no se ve afectada por emociones subjetivas.

- Utiliza rangos de retroceso fijos para identificar las divergencias, evitando ajustes frecuentes de parámetros.

- La combinación con condiciones adicionales como el RSI diario reduce la probabilidad de señales falsas.

Riesgos y soluciones

Esta estrategia también conlleva ciertos riesgos:

- Una divergencia en el RSI no necesariamente implica una reversión inmediata del precio; puede haber un desfase temporal, lo que aumenta el riesgo de que se active un stop loss. La solución es ampliar adecuadamente el margen del stop loss para darle al precio suficiente tiempo para confirmar la señal de divergencia.

- Si el fenómeno de divergencia se prolonga demasiado, también aumenta el riesgo. La solución es incorporar indicadores RSI de plazos más largos, como diarios o semanales, como filtro adicional.

- Una divergencia de magnitud demasiado pequeña tampoco puede confirmar un cambio de tendencia; es necesario ampliar el rango de retroceso para buscar divergencias RSI más evidentes.

Direcciones de optimización de la estrategia

Esta estrategia se puede optimizar en los siguientes aspectos:

- Optimizar los parámetros del RSI para encontrar la mejor combinación.

- Probar otros indicadores técnicos como MACD, KDJ, etc., para identificar fenómenos de divergencia.

- Agregar condiciones de filtro para períodos de consolidación, reduciendo las señales falsas en rangos laterales.

- Combinar RSI de múltiples marcos temporales para encontrar la mejor combinación de señales.

Resumen

La estrategia de trading por divergencia del RSI identifica los fenómenos de divergencia entre el RSI y el precio para determinar los puntos de inflexión de la tendencia y generar señales de trading. Esta estrategia es simple y práctica; optimizando los parámetros y agregando filtros, se puede mejorar aún más la probabilidad de ganancias. En general, la estrategia de divergencia del RSI es una estrategia de trading cuantitativo muy efectiva.

- 1