Estrategia de compra que combina el indicador de momentum con la media móvil

Resumen

Esta estrategia combina el indicador de momento MACD y el indicador direccional DMI, y realiza operaciones largas cuando se cumplen las condiciones. Sus salidas establecen un take profit fijo y un trailing stop basado en la volatilidad personalizada para asegurar las ganancias.

Principio

Las entradas de esta estrategia dependen de los indicadores MACD y DMI:

- Cuando el MACD es positivo (la línea MACD está por encima de la línea de señal), indica que el impulso alcista del mercado se está fortaleciendo.

- Cuando el DI+ del DMI es superior al DI-, indica que el mercado se encuentra en una fase de tendencia alcista.

Cuando ambas condiciones se cumplen simultáneamente, se abre una posición larga.

Las salidas de posición tienen dos criterios:

- Take profit fijo: se toma ganancia cuando el precio de cierre alcanza el porcentaje establecido.

- Trailing stop basado en volatilidad: se calcula una posición de stop loss dinámica utilizando el ATR y el precio máximo reciente. Esto permite un trailing stop loss ajustado según la volatilidad del mercado.

Ventajas

- La combinación de MACD y DMI permite juzgar de manera relativamente fiable la dirección de la tendencia del mercado, reduciendo operaciones erróneas.

- La condición de take profit combina un take profit fijo y un stop loss basado en volatilidad, lo que permite asegurar ganancias de forma flexible.

Riesgos

- Tanto el MACD como el DMI pueden generar señales falsas, provocando pérdidas innecesarias.

- El take profit fijo puede impedir maximizar las ganancias.

- La velocidad del trailing stop basado en volatilidad podría ajustarse de manera inadecuada, resultando demasiado agresiva o conservadora.

Direcciones de optimización

- Se podría considerar la inclusión de otros indicadores para filtrar las señales de entrada, por ejemplo, utilizando el indicador KDJ para determinar si hay sobrecompra o sobreventa.

- Se pueden probar diferentes parámetros para obtener un mejor efecto de take profit y stop loss.

- Se pueden ajustar parámetros como las medias móviles según el activo específico para optimizar el sistema.

Conclusión

Esta estrategia integra múltiples indicadores para juzgar la tendencia y las condiciones del mercado, interviniendo en situaciones con alta probabilidad de ser favorables. Las condiciones de take profit también han sido optimizadas, considerando tanto la garantía de ciertas ganancias como la flexibilidad para asegurarlas. Mediante el ajuste de parámetros y una gestión de riesgos adicional, esta estrategia puede convertirse en un sistema de trading cuantitativo de salida estable.

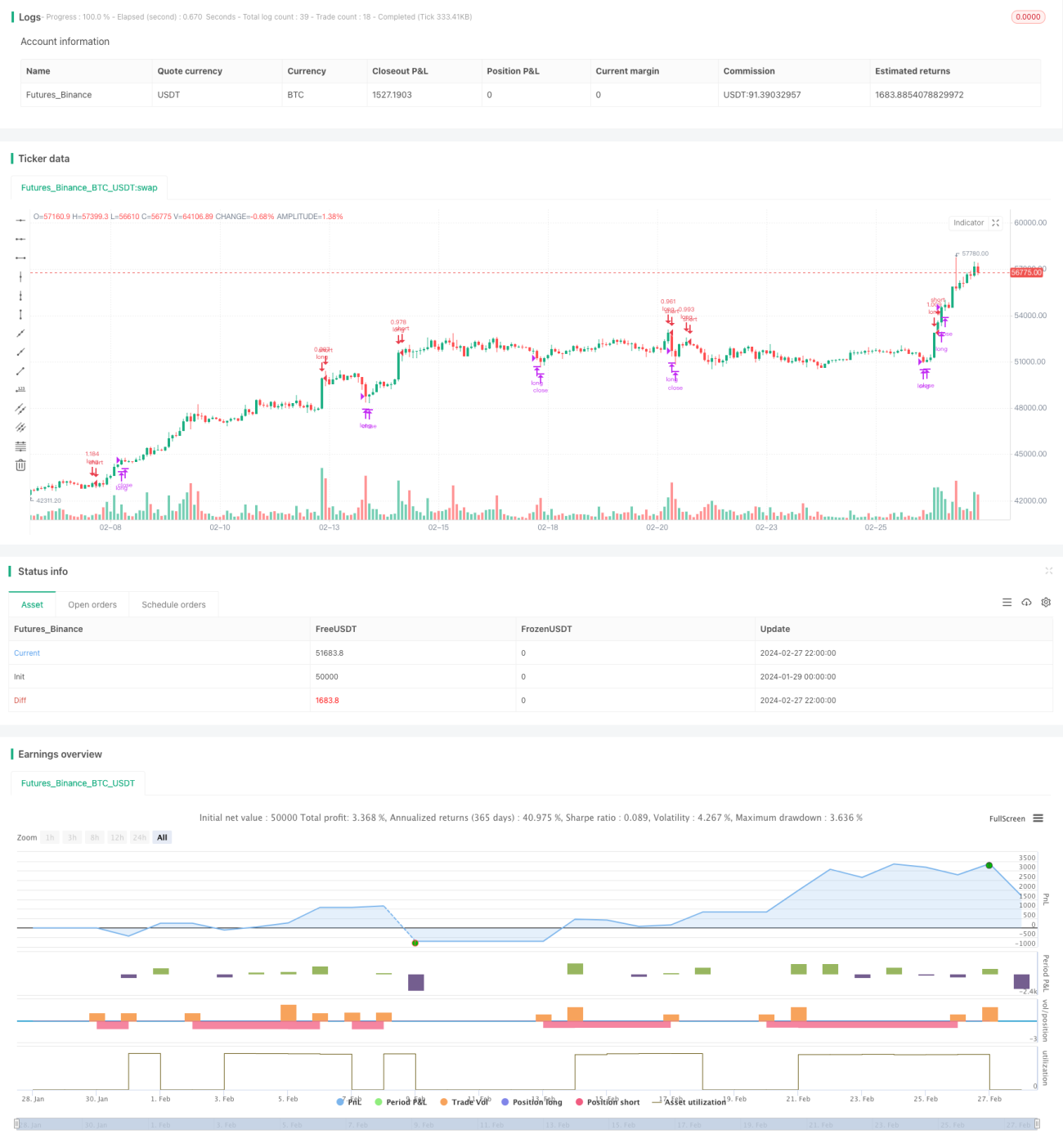

/*backtest

start: 2024-01-29 00:00:00

end: 2024-02-28 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='(MACD + DMI Scalping with Volatility Stop',title='MACD + DMI Scalping with Volatility Stop by (Coinrule)', overlay=true, initial_capital = 100, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.1)

- 1