Stratégie de trading momentum basée sur plusieurs moyennes mobiles

Aperçu

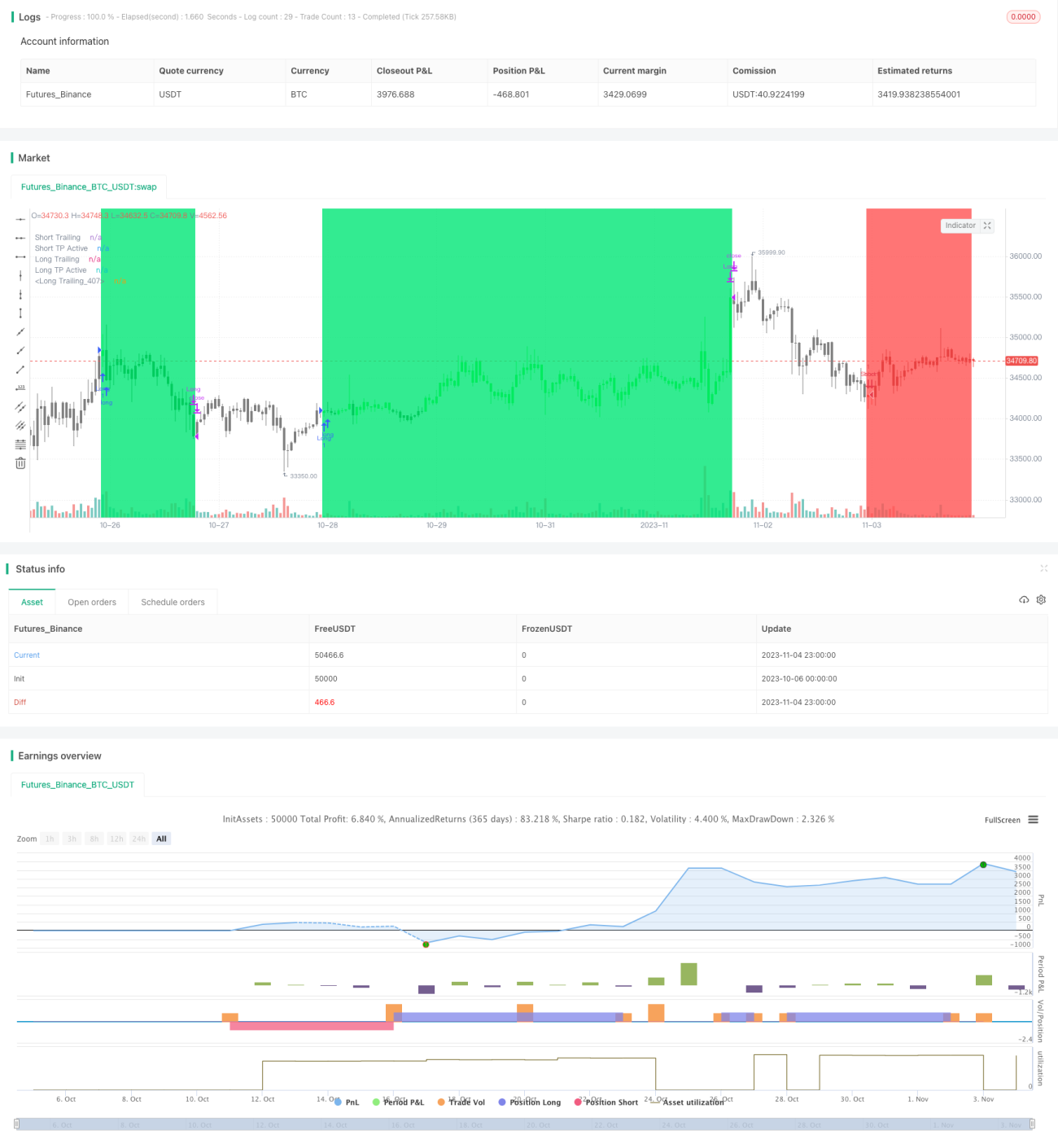

Cette stratégie de trading combine plusieurs moyennes mobiles avec un indicateur de momentum pour identifier la direction et la force d'une tendance. Elle prend position au début de la tendance, puis utilise un stop suiveur et un take profit suiveur pour optimiser les profits et contrôler les risques. L'objectif est de capturer des mouvements de prix importants dans les tendances à moyen et long terme.

Principe de la stratégie

-

Deux groupes de moyennes mobiles avec des paramètres différents sont utilisés pour construire une ligne rapide et une ligne lente :

- La ligne rapide est composée d'une moyenne mobile exponentielle sur 5 périodes et d'une moyenne mobile pondérée sur 25 périodes, représentant la tendance à court terme.

- La ligne lente est composée d'une moyenne mobile exponentielle sur 28 périodes et d'une moyenne mobile pondérée sur 72 périodes, représentant la tendance à moyen et long terme.

-

Lorsque la ligne rapide croise au-dessus de la ligne lente, cela indique que la tendance à court terme commence à être plus forte que la tendance à moyen et long terme, ce qui constitue un signal d'entrée.

-

L'indicateur de momentum RSI est utilisé en complément : l'entrée n'est effectuée que lorsque le RSI est en zone basse (signal d'achat) ou en zone haute (signal de vente), afin de filtrer les faux signaux de cassure.

-

Une fois en position, un stop suiveur est utilisé pour limiter les pertes, et un take profit suiveur pour verrouiller les gains.

-

Lorsque la ligne rapide croise en dessous de la ligne lente, cela signale un retournement de tendance, et la position est fermée par le stop ou le take profit.

Analyse des avantages

- La combinaison de deux moyennes mobiles filtre le bruit et identifie la direction et la force du mouvement au milieu de la tendance.

- L'entrée n'a lieu qu'au début de la tendance, évitant les pertes inutiles dues aux faux signaux de cassure.

- L'indicateur de momentum associé améliore la qualité des entrées.

- Le stop suiveur réduit les pertes unitaires, limitant l'impact des points défavorables.

- Le take profit suiveur permet de réaliser des gains substantiels et d'ajouter aux profits lorsque le marché est favorable.

Analyse des risques

- La combinaison de deux moyennes mobiles peut être en retard au niveau des points de retournement de tendance, ce qui pourrait faire manquer des opportunités de retournement.

- Solution : raccourcir les périodes des moyennes mobiles pour les rendre plus sensibles.

- Les faux signaux de cassure peuvent entraîner des entrées non justifiées.

- Solution : ajouter davantage d'indicateurs de filtrage.

- Les distances de stop ou de take profit non optimisées peuvent être trop lâches ou trop serrées.

- Solution : optimiser les paramètres via un backtest pour trouver les distances optimales.

- Stratégie directionnelle, adaptée uniquement aux marchés en tendance.

- Solution : décider d'utiliser ou non la stratégie en fonction des conditions générales du marché.

Pistes d'optimisation

- Optimiser les paramètres des moyennes mobiles pour trouver la meilleure combinaison représentant la tendance.

- Ajouter des indicateurs de filtrage de tendance, par exemple un stop dynamique basé sur l'ATR, l'indicateur de volume d'énergie, etc.

- Optimiser les paramètres de stop et de take profit pour trouver la meilleure combinaison.

- Ajouter une évaluation des grandes tendances du marché pour décider d'activer ou non la stratégie.

- Ajouter une analyse multi-périodes en utilisant la direction de la tendance de plus grande échelle pour guider la stratégie à court terme.

Conclusion

Cette stratégie intègre les moyennes mobiles et les indicateurs de momentum dans le but d'identifier des entrées précoces lors de l'émergence de tendances, et de gérer les risques et les profits par un stop et un take profit opportuns. Bien qu'elle nécessite encore une optimisation des paramètres et des règles pour s'adapter à des conditions de marché plus larges, elle possède déjà le cadre de base et l'orientation d'une stratégie de suivi de tendance à moyen et long terme. Grâce à des améliorations continues, cette stratégie a le potentiel de devenir une stratégie de suivi de tendance stable et efficace.

- 1