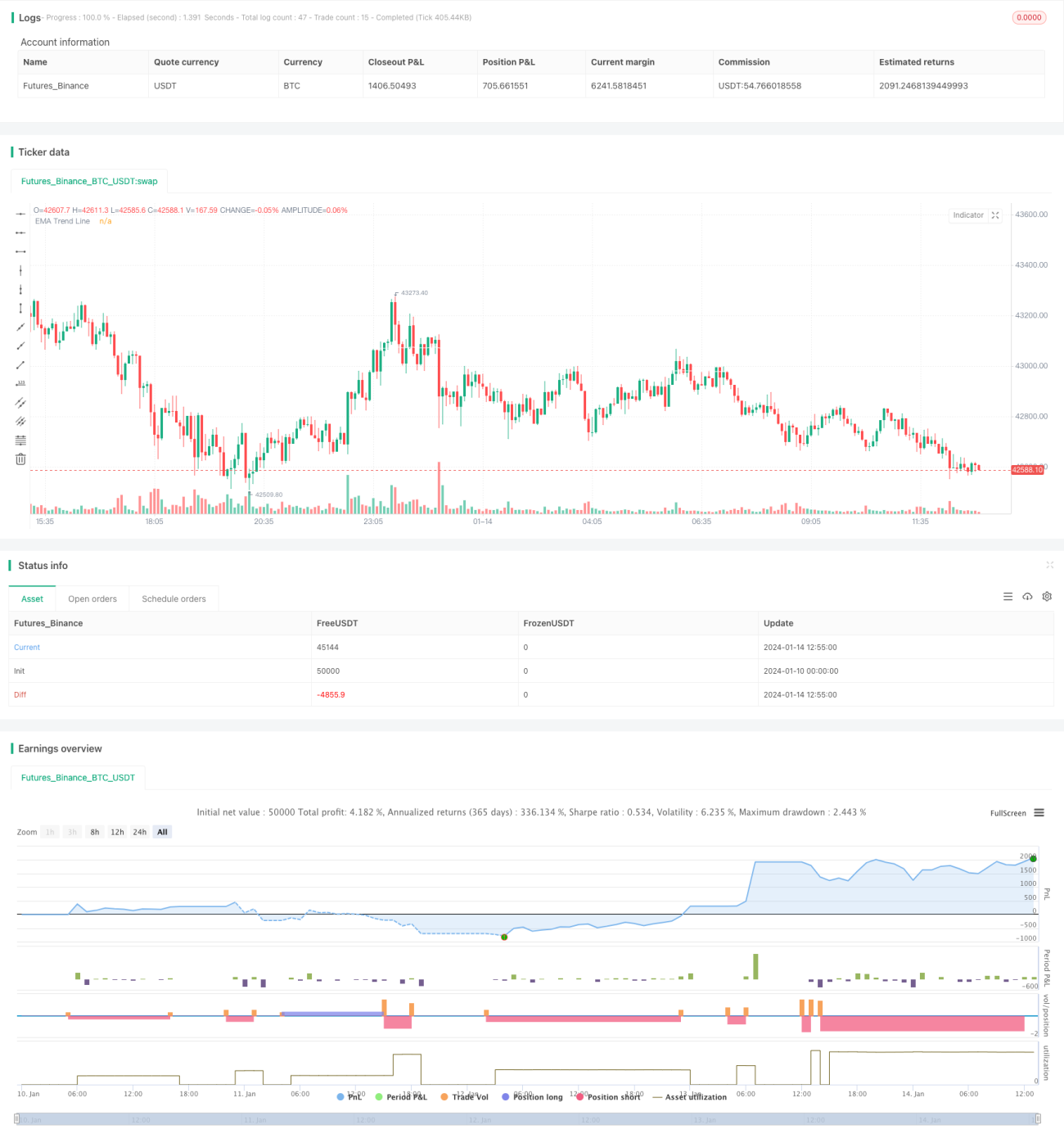

Stratégie de suivi de tendance combinant double EMA et RSI

Aperçu

Cette stratégie combine l'utilisation de doubles EMA et de l'indicateur RSI pour identifier la tendance des prix et entrer en position dès que la direction de la tendance s'inverse. Plus précisément, la stratégie utilise une EMA à long terme pour déterminer la tendance générale, tout en utilisant le RSI pour détecter les conditions de surachat et de survente à court terme. Lorsque le prix effectue un retracement dans la direction de la tendance principale, le RSI génère un signal de transaction, permettant d'acheter ou de vendre à découvert en fonction de la tendance.

Principe de la stratégie

-

Une EMA sur 200 périodes est utilisée pour juger de la tendance générale. Le franchissement à la hausse de la ligne EMA par le prix est un signal haussier, le franchissement à la baisse est un signal baissier.

-

Le RSI est paramétré sur 10 périodes. Un croisement à la hausse du RSI au-dessus de 40 est un signal de survente, un croisement à la baisse sous 60 est un signal de surachat.

-

Lorsque la tendance générale est haussière (prix au-dessus de l'EMA), si le RSI passe en dessous de 40 (signal de survente), on prend une position longue.

-

Lorsque la tendance générale est baissière (prix en dessous de l'EMA), si le RSI passe au-dessus de 60 (signal de surachat), on prend une position courte.

-

Le stop-loss est fixé à 4 fois l'ATR. Le take-profit est fixé à 2 fois le stop-loss, ce qui donne un ratio risque/récompense de 2:1.

Analyse des avantages

Le principal avantage de cette stratégie est qu'elle combine à la fois des indicateurs de tendance et de retournement, permettant d'entrer en position lors des retracements de tendance, ce qui peut offrir de bonnes performances. Les avantages spécifiques sont les suivants :

-

L'utilisation d'un système à double EMA pour déterminer la direction principale de la tendance permet de suivre efficacement la tendance des prix.

-

Le RSI permet d'identifier les conditions de surachat et de survente à court terme, aidant à déterminer le moment d'entrée.

-

Le stop-loss basé sur l'ATR s'adapte à la volatilité du marché, ce qui favorise la gestion des risques.

-

Le respect strict des principes de trading de tendance réduit les transactions inutiles et diminue le risque systémique.

Analyse des risques

Cette stratégie présente principalement les risques suivants :

-

Lorsque la tendance devient hésitante ou s'affaiblit, des signaux erronés peuvent survenir. Il convient alors d'évaluer la situation avec prudence avant d'entrer.

-

Dans des conditions de marché extrêmes, le stop-loss basé sur l'ATR peut être trop large ou trop serré, nécessitant un ajustement dynamique. On peut également envisager d'utiliser d'autres méthodes de stop-loss.

-

La fréquence de génération des signaux de transaction peut être élevée, il faut donc vérifier si elle correspond à ses préférences de fréquence de trading.

-

Il est important de vérifier si les paramètres du RSI sont appropriés et d'effectuer une optimisation périodique.

Pistes d'optimisation

Les principales pistes d'optimisation de cette stratégie sont les suivantes :

-

Tester l'ajout d'autres indicateurs de tendance, comme le MACD, pour aider à déterminer la direction de la tendance.

-

Tester d'autres indicateurs de retournement, comme le KDJ ou les bandes de Bollinger, en combinaison avec le RSI pour trouver de meilleurs signaux de transaction.

-

Introduire des algorithmes d'apprentissage automatique pour ajuster automatiquement les paramètres et permettre un stop-loss et un take-profit dynamiques.

-

Intégrer des indicateurs de sentiment, des informations fondamentales, etc., pour améliorer la robustesse globale du système.

Conclusion

Dans l'ensemble, cette stratégie est une stratégie de trading à court terme très typique combinant suivi de tendance et indicateurs de retournement. En utilisant une double EMA pour déterminer la tendance générale et en exploitant les caractéristiques de retournement du RSI pour capturer les opportunités de pullback, la stratégie combine les avantages de différents indicateurs, créant un effet de complémentarité. Si des améliorations sont apportées ultérieurement par l'optimisation des paramètres, la fusion de modèles, etc., le potentiel d'amélioration des performances de cette stratégie est encore important.

- 1