Stratégie de suivi de tendance basée sur la moyenne mobile adaptative

Aperçu

Cette stratégie utilise l'indicateur de moyenne mobile adaptative de Kaufman (KAMA) pour concevoir un système de trading de suivi de tendance. Ce système permet de suivre rapidement la tendance lorsqu'elle se forme et de filtrer le bruit en période de range. Par ailleurs, le système intègre le système de retournement parabolique (PSAR) et le stop suiveur basé sur l'Average True Range (ATR Trailing Stop) comme mécanismes de stop-loss, offrant ainsi une solide capacité de gestion des risques.

Principe de la stratégie

-

La longueur de l'indicateur KAMA est ajustée dynamiquement en fonction de la volatilité du marché sur une période récente. Lorsque la variation de prix dépasse le bruit récent, la fenêtre de la moyenne mobile exponentielle (EMA) se raccourcit ; lorsque la variation de prix est inférieure au bruit récent, la fenêtre s'allonge. Cela permet au KAMA de suivre rapidement la tendance tout en filtrant le bruit en période de range.

-

Le système utilise principalement le KAMA le plus rapide (KAMA 1) pour déterminer la direction de la tendance. Lorsque KAMA 1 monte, on prend une position longue ; lorsqu'il descend, on prend une position courte. Pour filtrer les faux signaux, un filtre KAMA est défini. Un signal de trading est généré uniquement lorsque la variation de KAMA 1 dépasse un écart-type de la volatilité récente.

-

En ce qui concerne le stop loss, le système propose trois méthodes optionnelles : stop basé sur le retournement du KAMA, stop basé sur le retournement du PSAR, et stop suiveur ATR. L'investisseur peut choisir une ou plusieurs combinaisons selon ses préférences.

Analyse des avantages

-

La conception unique de l'indicateur KAMA permet au système de capturer rapidement les nouvelles tendances, de cesser de trader en période de range, de contrôler efficacement la fréquence des transactions et de réduire les pertes inutiles dues au slippage et aux frais.

-

Le système intègre plusieurs mécanismes de stop-loss. L'investisseur peut choisir la méthode de stop appropriée en fonction de son appétence au risque, maîtrisant ainsi les pertes unitaires.

-

Le système repose entièrement sur les indicateurs et les lignes de stop, évitant les problèmes courants d'entrée sur des décalages de prix.

-

La multiplicité des paramètres et des combinaisons de conditions offre une grande flexibilité de personnalisation. L'utilisateur peut optimiser le système en fonction des différents instruments et périodes.

Analyse des risques

-

Le système ne prend pas en compte le risque systémique ; en cas de conditions de marché extrêmes, il ne parvient pas à contrôler efficacement les pertes.

-

Les paramètres du système peuvent nécessiter des ajustements selon l'instrument et la période considérés, sous peine de produire des résultats trop agressifs ou trop conservateurs.

-

Si l'on se fie uniquement au KAMA comme stop-loss, on risque de rester piégé en période de range. Cela nécessite une combinaison avec le PSAR ou le stop suiveur ATR.

Directions d'optimisation

-

Ajouter des indicateurs de filtre de tendance, comme l'ADX ou l'indice de volatilité implicite, pour éviter les faux signaux en période de range et lors des transitions de tendance.

-

Optimiser et backtester les paramètres pour un instrument et une période donnés, afin d'améliorer la robustesse. Les dimensions d'optimisation incluent la combinaison des paramètres KAMA, les paramètres de stop-loss, etc.

-

Tester l'utilisation de modèles d'apprentissage automatique pour remplacer l'optimisation des paramètres. Utiliser un grand volume de données historiques pour entraîner des réseaux de neurones ou des arbres de décision capables de déterminer les points d'achat/vente et les niveaux de stop-loss.

-

Tenter d'adapter la stratégie à d'autres instruments, comme les crypto-monnaies. Cela pourrait nécessiter des ajustements de paramètres ou l'ajout d'autres indicateurs auxiliaires.

Résumé

Cette stratégie intègre le jugement de tendance via le KAMA et plusieurs méthodes de stop-loss, permettant de suivre efficacement la direction de la tendance tout en contrôlant les risques. Le caractère unique du KAMA permet à la stratégie de détecter rapidement les nouvelles tendances et d'éviter les faux signaux. Les paramètres personnalisables et optimisables offrent une grande marge de manœuvre pour des ajustements individuels. En optimisant les paramètres pour un seul instrument et une seule période, et en intégrant des modèles d'apprentissage automatique, la performance de la stratégie pourrait encore être améliorée.

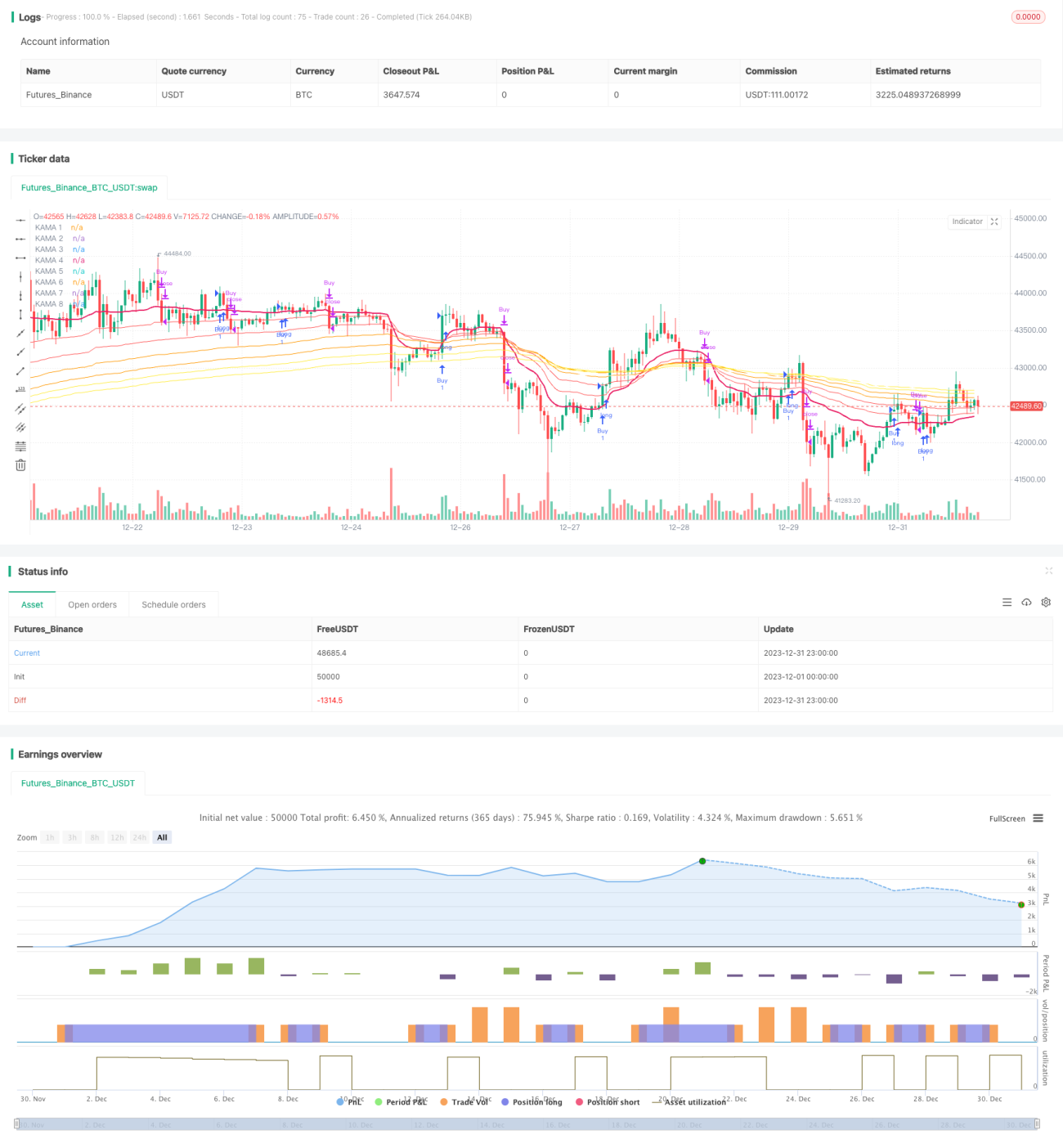

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © BenHampson

// @version=4

// Credit to:- 1