Stratégie de trading de séparation haussière et baissière basée sur l'indicateur RSI

Aperçu

Cette stratégie identifie les phénomènes de divergence haussière et baissière à l'aide de l'indicateur RSI pour prendre des décisions de trading. L'idée centrale est que lorsque le prix atteint un nouveau plus bas mais que le RSI enregistre un nouveau plus haut, cela constitue un signal de « divergence haussière », indiquant qu'un plancher s'est formé, et il convient d'acheter. À l'inverse, lorsque le prix atteint un nouveau plus haut mais que le RSI enregistre un nouveau plus bas, cela constitue un signal de « divergence baissière », indiquant qu'un sommet s'est formé, et il convient de vendre à découvert.

Principe de la stratégie

Cette stratégie utilise principalement l'indicateur RSI pour identifier les divergences entre le prix et le RSI. La méthode est la suivante :

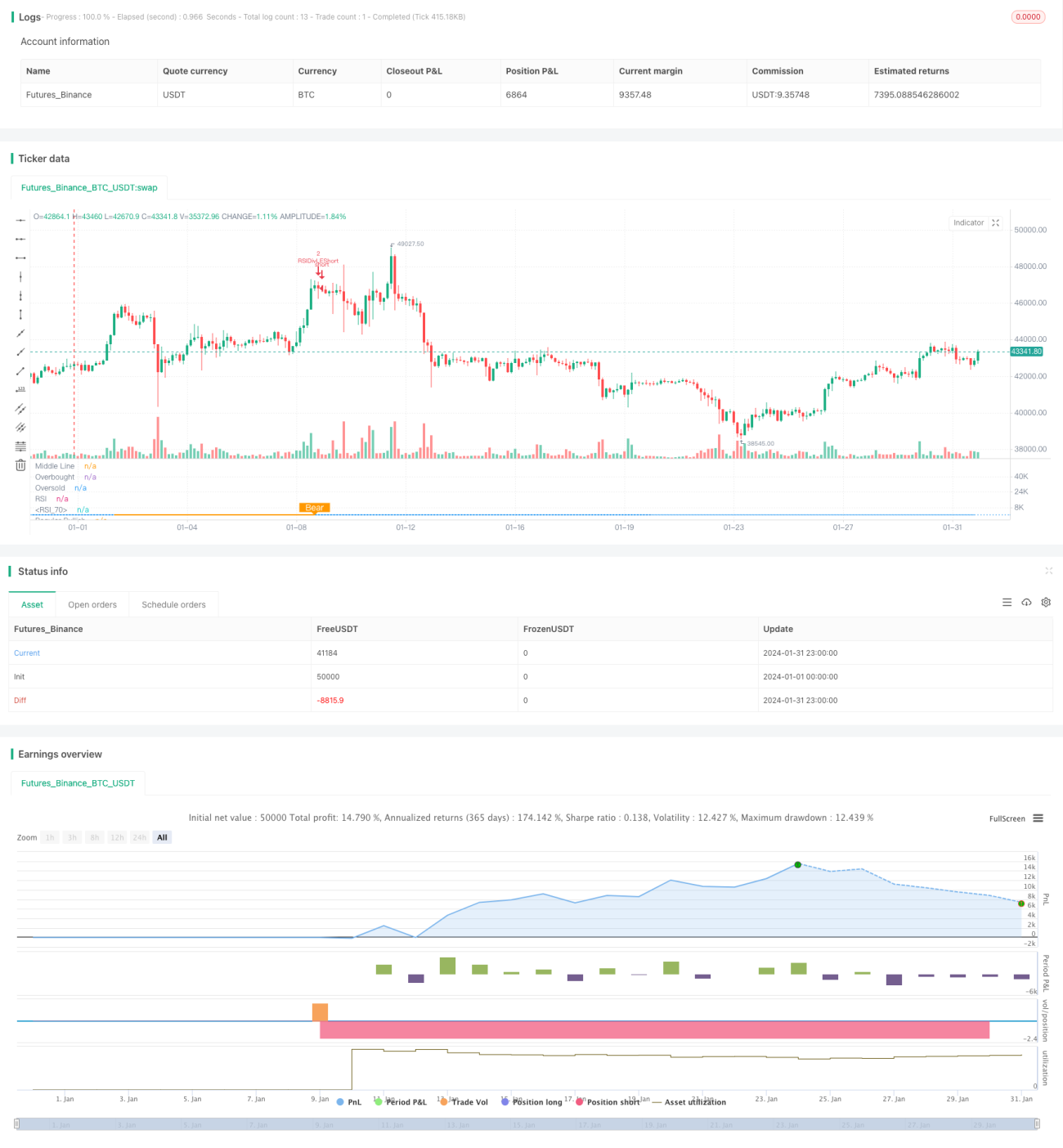

- Utiliser l'indicateur RSI avec une période de 13 et la source de données étant le prix de clôture.

- Définir la fenêtre de rétrospection gauche pour la divergence haussière à 14 jours et la fenêtre de rétrospection droite à 2 jours.

- Définir la fenêtre de rétrospection gauche pour la divergence baissière à 47 jours et la fenêtre de rétrospection droite à 1 jour.

- Lorsque le prix forme un plus bas plus bas, mais que le RSI forme un plus bas plus haut, la condition de divergence haussière est remplie, générant un signal d'achat.

- Lorsque le prix forme un plus haut plus haut, mais que le RSI forme un plus haut plus bas, la condition de divergence baissière est remplie, générant un signal de vente à découvert.

En identifiant les phénomènes de divergence entre le prix et le RSI, il est possible de détecter à l'avance les points de retournement de la tendance des prix et de prendre des décisions de trading.

Avantages de la stratégie

Cette stratégie présente principalement les avantages suivants :

- L'identification des divergences entre le prix et le RSI permet d'anticiper les points de retournement de tendance et de saisir les opportunités de trading.

- Étant basée sur une analyse d'indicateurs, elle n'est pas influencée par les émotions subjectives.

- Elle utilise des fenêtres de rétrospection fixes pour identifier les divergences, évitant ainsi des ajustements fréquents des paramètres.

- L'ajout de conditions supplémentaires telles que le RSI journalier réduit la probabilité de faux signaux.

Risques et solutions

Cette stratégie comporte également certains risques :

- Une divergence du RSI n'implique pas nécessairement un retournement immédiat des prix ; il peut y avoir un décalage temporel, ce qui risque de déclencher un stop-loss. La solution consiste à élargir légèrement la marge du stop-loss pour donner au prix suffisamment de temps pour confirmer le signal de divergence.

- Un phénomène de divergence qui se prolonge trop longtemps augmente également le risque. La solution consiste à utiliser le RSI sur des périodes plus longues (journalier ou hebdomadaire) comme filtre supplémentaire.

- Une divergence trop faible ne permet pas de confirmer le retournement de tendance ; il est nécessaire d'élargir la fenêtre de rétrospection pour rechercher des divergences RSI plus marquées.

Pistes d'optimisation de la stratégie

Cette stratégie peut également être optimisée dans les directions suivantes :

- Optimiser les paramètres du RSI pour trouver la meilleure combinaison.

- Tester d'autres indicateurs techniques comme le MACD, le KD, etc., pour identifier les divergences.

- Ajouter des conditions de filtrage appropriées pendant les périodes de range pour réduire les faux signaux en période de volatilité latérale.

- Combiner le RSI sur plusieurs périodes pour trouver la meilleure combinaison de signaux.

Résumé

La stratégie de trading basée sur les divergences RSI identifie les phénomènes de divergence entre le RSI et le prix pour détecter les points de retournement de tendance et générer des signaux de trading. Cette stratégie est simple et pratique ; en optimisant les paramètres et en ajoutant des filtres, il est possible d'améliorer encore la probabilité de profit. Dans l'ensemble, la stratégie de divergence RSI est une stratégie de trading quantitatif très efficace.

- 1