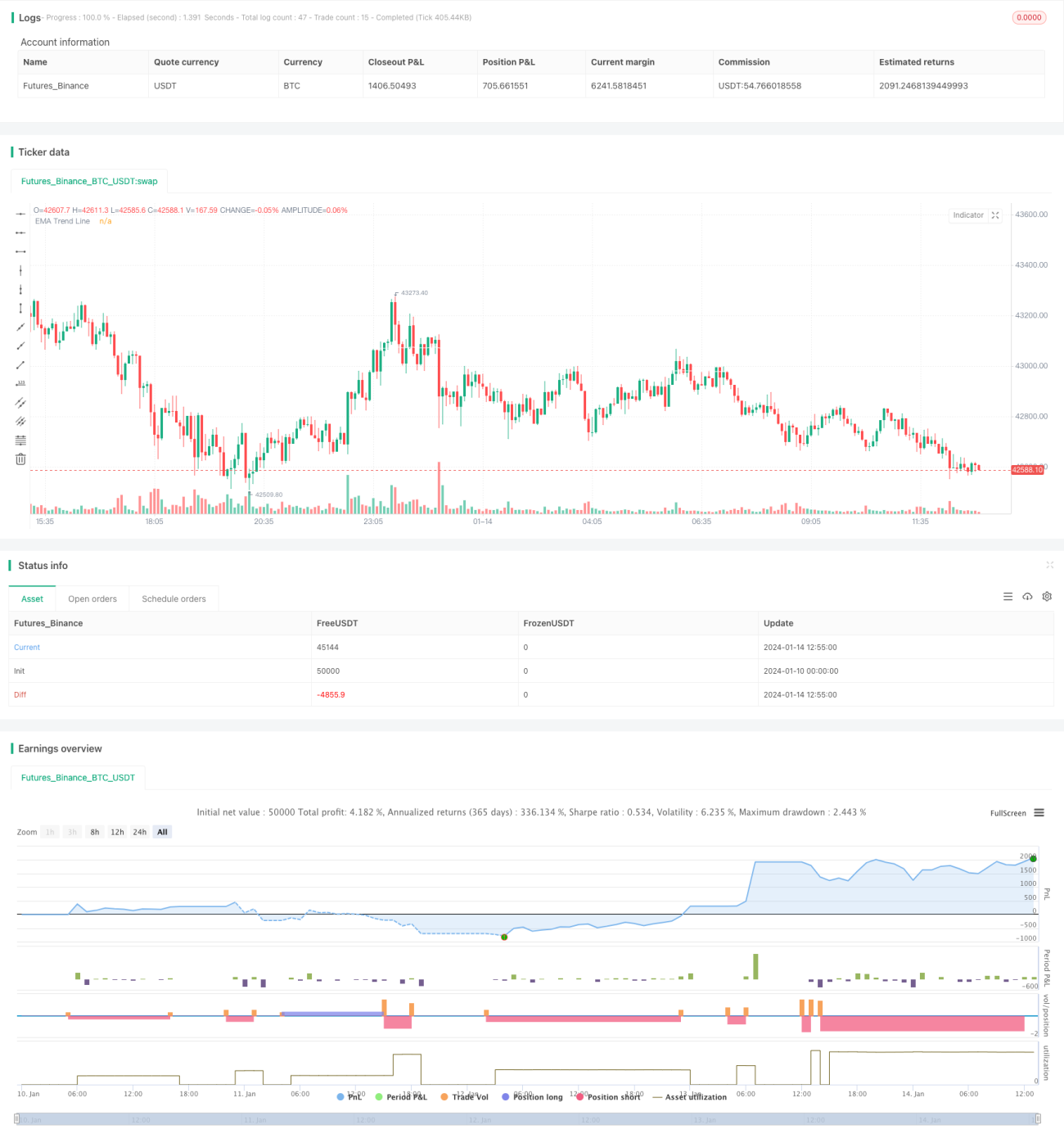

Strategi Mengikuti Tren dengan Kombinasi EMA Ganda dan RSI

Ikhtisar

Strategi ini menggabungkan indikator EMA ganda dan RSI untuk mengidentifikasi tren harga dan masuk pada saat terjadi pembalikan arah tren. Secara spesifik, strategi ini menggunakan EMA dengan periode lebih panjang untuk menentukan arah tren utama, sementara RSI digunakan untuk mendeteksi kondisi overbought dan oversold jangka pendek. Ketika harga mengalami pullback searah dengan tren utama, sinyal trading dikeluarkan berdasarkan RSI, kemudian posisi long atau short diambil sesuai arah tren.

Prinsip Strategi

- Menggunakan EMA 200 periode untuk menentukan arah tren utama. Harga menembus ke atas EMA dianggap sinyal bullish, menembus ke bawah EMA dianggap sinyal bearish.

- Parameter RSI diatur ke 10 periode. RSI menembus ke atas 40 adalah sinyal oversold, menembus ke bawah 60 adalah sinyal overbought.

- Ketika tren utama naik (harga di atas EMA), jika terjadi sinyal oversold dari RSI menembus ke bawah 40, lakukan posisi long.

- Ketika tren utama turun (harga di bawah EMA), jika terjadi sinyal overbought dari RSI menembus ke atas 60, lakukan posisi short.

- Stop loss ditetapkan sebesar 4 kali ATR. Take profit ditetapkan sebesar 2 kali stop loss, sehingga rasio risk-reward menjadi 2:1.

Analisis Keunggulan

Keunggulan terbesar dari strategi ini adalah menggabungkan indikator tren dan reversal secara bersamaan, sehingga dapat masuk tepat saat terjadi pullback dalam tren, menghasilkan performa yang baik. Keunggulan spesifiknya antara lain:

- Menggunakan sistem EMA ganda untuk menentukan arah tren utama, sehingga mampu melacak tren harga secara efektif.

- RSI dapat mengidentifikasi kondisi overbought dan oversold jangka pendek, membantu menentukan titik masuk.

- Stop loss ditetapkan berdasarkan ATR, sehingga dapat menyesuaikan lebar stop loss sesuai volatilitas pasar, mendukung manajemen risiko.

- Mematuhi prinsip trading tren secara ketat, mengurangi trading yang tidak perlu dan menurunkan risiko sistemik.

Analisis Risiko

Risiko utama strategi ini antara lain:

- Dalam kondisi tren yang melemah atau sideways, sinyal trading yang salah dapat muncul. Perlu mempertimbangkan situasi dengan hati-hati sebelum masuk.

- Dalam kondisi pasar ekstrem, stop loss yang ditetapkan oleh ATR bisa terlalu besar atau terlalu kecil, sehingga perlu penyesuaian dinamis. Dapat juga dipertimbangkan untuk mengganti dengan metode stop loss lain.

- Frekuensi kemunculan sinyal trading mungkin cukup tinggi, perlu diperhatikan apakah sesuai dengan preferensi frekuensi trading Anda.

- Perlu dipastikan parameter RSI sudah tepat, dan sebaiknya dilakukan optimasi parameter secara berkala.

Arah Optimalisasi

Arah utama yang dapat dioptimalkan dari strategi ini antara lain:

- Dapat menguji penambahan indikator tren lain, seperti MACD, untuk membantu menentukan arah tren.

- Dapat menguji indikator reversal lain, seperti KDJ, Bollinger Bands, dan menggabungkannya dengan RSI untuk mencari sinyal trading yang lebih baik.

- Dapat memperkenalkan algoritma machine learning untuk menyesuaikan parameter secara adaptif, sehingga mencapai stop loss dan take profit dinamis.

- Dapat mempertimbangkan lebih banyak faktor seperti indikator sentimen, berita, dan lainnya untuk meningkatkan ketahanan sistem secara keseluruhan.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi jangka pendek yang sangat khas, menggabungkan pengikut tren dan indikator reversal. Dengan menggunakan EMA ganda untuk menentukan tren utama, serta memanfaatkan karakter reversal RSI untuk menangkap peluang pullback dalam tren. Dari segi prinsip, strategi ini menggabungkan kelebihan berbagai indikator, membentuk efek saling melengkapi yang baik. Jika di masa depan ditingkatkan melalui optimasi parameter, penggabungan model, dan lainnya, efek strategi ini masih memiliki potensi peningkatan yang besar.

- 1