Strategi Trading Pemisahan Long Short Indikator RSI

Ikhtisar

Strategi ini mengidentifikasi fenomena divergensi bullish dan bearish menggunakan indikator RSI untuk membuat keputusan trading. Ide intinya adalah ketika harga mencapai titik terendah baru tetapi RSI menunjukkan titik tertinggi baru, terbentuk sinyal "divergensi bullish" yang menunjukkan dasar telah terbentuk, sehingga posisi long diambil. Sebaliknya, ketika harga mencapai titik tertinggi baru tetapi RSI menunjukkan titik terendah baru, terbentuk sinyal "divergensi bearish" yang menunjukkan puncak telah terbentuk, sehingga posisi short diambil.

Prinsip Strategi

Strategi ini terutama menggunakan indikator RSI untuk mengidentifikasi divergensi bullish dan bearish antara harga dan RSI. Metode spesifiknya adalah sebagai berikut:

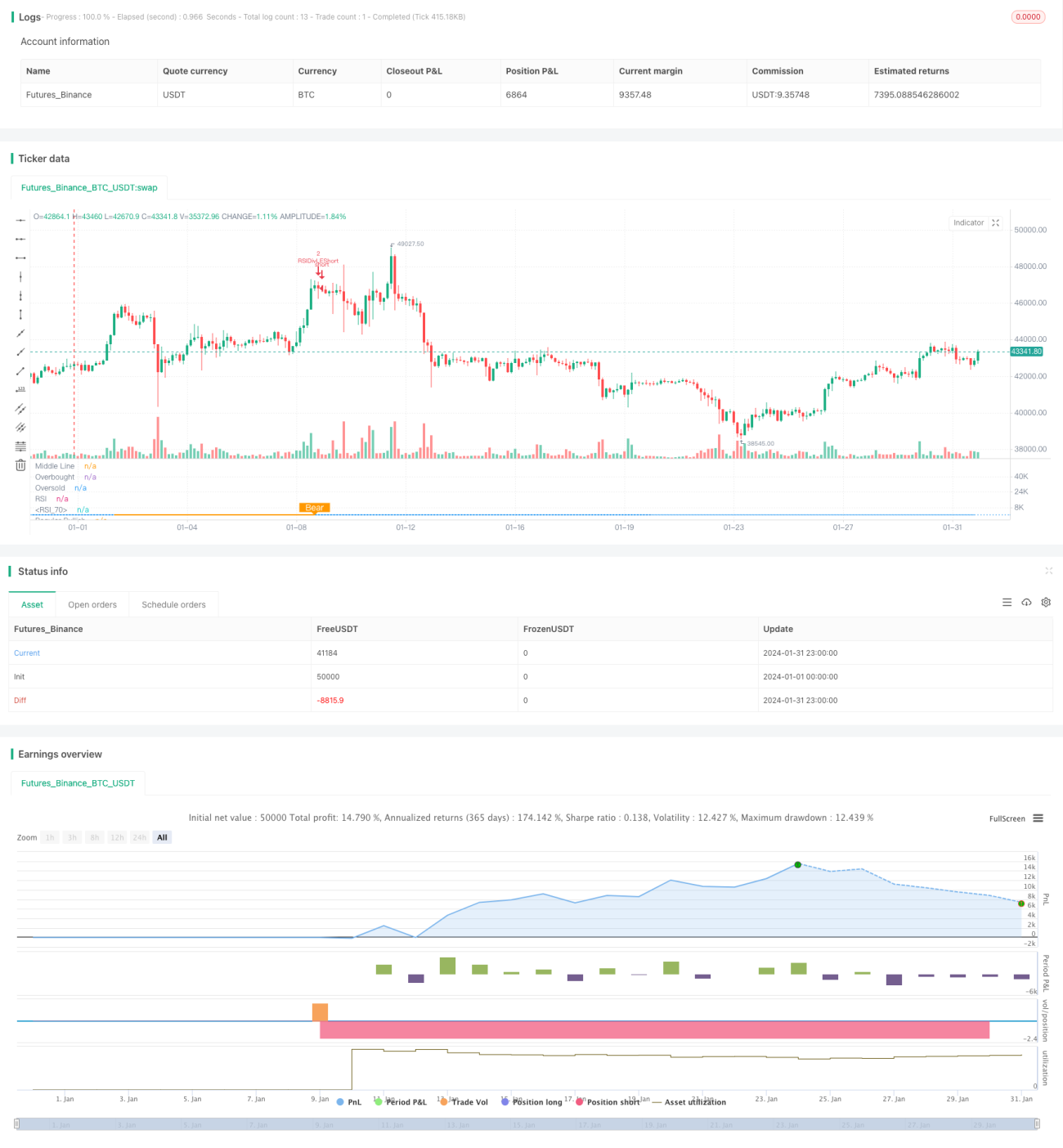

- Menggunakan parameter RSI 13, dengan data sumber harga penutupan.

- Menentukan rentang lookback kiri untuk divergensi bullish adalah 14 hari, dan rentang lookback kanan adalah 2 hari.

- Menentukan rentang lookback kiri untuk divergensi bearish adalah 47 hari, dan rentang lookback kanan adalah 1 hari.

- Ketika harga menciptakan titik terendah yang lebih rendah, namun RSI menciptakan titik terendah yang lebih tinggi, kondisi divergensi bullish terpenuhi, menghasilkan sinyal long.

- Ketika harga menciptakan titik tertinggi yang lebih tinggi, namun RSI menciptakan titik tertinggi yang lebih rendah, kondisi divergensi bearish terpenuhi, menghasilkan sinyal short.

Dengan mengidentifikasi fenomena divergensi bullish dan bearish antara harga dan indikator RSI, titik balik pergerakan harga dapat ditangkap lebih awal, sehingga keputusan trading dapat diambil.

Keunggulan Strategi

Strategi ini memiliki keunggulan utama sebagai berikut:

- Mengidentifikasi fenomena divergensi bullish dan bearish antara harga dan RSI, memungkinkan prediksi lebih awal terhadap titik balik tren harga dan memanfaatkan peluang trading.

- Karena menggunakan analisis indikator, tidak terpengaruh oleh emosi subjektif.

- Menggunakan rentang lookback tetap untuk mengidentifikasi divergensi, menghindari penyesuaian parameter yang terlalu sering.

- Dengan menggabungkan kondisi tambahan seperti RSI harian, dapat mengurangi kemungkinan sinyal palsu.

Risiko dan Solusi

Strategi ini juga memiliki risiko tertentu:

- Divergensi pada indikator RSI belum tentu menandakan pembalikan harga segera; mungkin ada jeda waktu, yang dapat menyebabkan stop loss tersentuh. Solusinya adalah melonggarkan sedikit lebar stop loss untuk memberikan waktu yang cukup bagi harga untuk mengkonfirmasi sinyal divergensi.

- Divergensi yang berlangsung terlalu lama juga dapat meningkatkan risiko. Solusinya adalah menggabungkan indikator RSI jangka panjang seperti harian atau mingguan sebagai filter.

- Divergensi dengan amplitudo terlalu kecil juga tidak dapat mengkonfirmasi pembalikan tren. Perlu memperbesar rentang lookback untuk mencari divergensi RSI yang lebih jelas.

Arahan Optimasi Strategi

Strategi ini juga dapat dioptimalkan dari beberapa arah berikut:

- Mengoptimalkan parameter RSI untuk menemukan kombinasi parameter terbaik.

- Mencoba indikator teknikal lain seperti MACD, KD, dll. untuk mengidentifikasi fenomena divergensi bullish dan bearish.

- Menambahkan kondisi filter periode sideways yang sesuai untuk mengurangi sinyal palsu selama periode sideways.

- Menggabungkan indikator RSI dari beberapa kerangka waktu untuk menemukan kombinasi sinyal terbaik.

Kesimpulan

Strategi trading divergensi bullish dan bearish RSI mengidentifikasi fenomena divergensi antara RSI dan harga untuk menilai titik balik pergerakan harga, sehingga menghasilkan sinyal trading. Strategi ini sederhana dan praktis. Dengan mengoptimalkan pengaturan parameter dan menambahkan filter, probabilitas profit dapat ditingkatkan lebih lanjut. Secara keseluruhan, strategi divergensi RSI adalah strategi trading kuantitatif yang sangat efektif.

- 1