123リバーサルと平滑RSIを組み合わせたトレーディング戦略

概要

この戦略は、123反転パターンとスムースRSIインジケーターを組み合わせることで、トレンド反転ポイントをより正確に捉え、勝率を高めることを目指します。どの時間足のどの銘柄にも適用可能な、非常に汎用性の高いトレンド反転売買戦略です。

戦略の原理

-

123反転パターンの判断:前2本の終値が高値・安値を形成し、3本目の終値が前日の終値を上回った場合、底値反転シグナルとなります。前2本の終値が安値・高値を形成し、3本目の終値が前日の終値を下回った場合、天井反転シグナルとなります。

-

スムースRSIインジケーターの判断:スムースRSIは加重移動平均を用いることで、通常のRSIの遅延性を低減します。RSIが設定した高閾値ラインを上抜けた場合、買いシグナル。RSIが設定した低閾値ラインを下抜けた場合、売りシグナルとなります。

-

戦略シグナル:123反転パターンとスムースRSIのシグナルが同方向のときのみ、売買シグナルが発生します。ロングシグナルは、123反転で底値シグナルが発生し、かつRSIが高閾値を上抜けたとき。ショートシグナルは、123反転で天井シグナルが発生し、かつRSIが低閾値を下抜けたときです。

戦略の優位性

-

トレンド判断指標RSIと反転パターンを組み合わせることで、トレンド反転ポイントをより正確に判断できます。

-

スムースRSIは平滑化処理により、通常のRSIが抱える遅延問題を軽減します。

-

123反転パターンはシンプルで明確であり、判断や実装が容易です。

-

パラメータを柔軟に調整可能で、様々な銘柄や時間足に適用でき、幅広い用途があります。

-

容易に最適化・改良が可能で、高い拡張性を持ちます。

戦略のリスク

-

123反転パターンは比較的単純であり、小さな値動きの調整に敏感でないため、偽のシグナルを発生させる可能性があります。

-

スムースRSIの最適化が不十分だと、パラメータ調整で過学習(オーバーフィッティング)に陥りやすいです。

-

反転パターンとRSIのシグナルが同方向でなければシグナルが発生しないため、シグナルの発生頻度が低くなる可能性があります。

-

取引コストが考慮されていないため、少額資金では利益を出しにくい場合があります。

-

ストップロス(損切り)の仕組みがないため、1回の損失をコントロールできません。

戦略の最適化の方向性

-

スムースRSIのパラメータを最適化し、最適なパラメータの組み合わせを見つける。

-

他のインジケーターやパターンを追加してフィルタリングし、シグナルの質を高める。

-

ストップロス(損切り)の仕組みを追加し、1回の損失をコントロールする。

-

取引コストを考慮し、異なる資金量に適応できるようにパラメータを調整する。

-

異なる銘柄や時間足でのパラメータ設定をテストし、最適なパラメータの組み合わせを探す。

-

自動パラメータ最適化機能を追加する。

まとめ

この戦略は全体的に明確でシンプルな考え方に基づいており、反転パターンとトレンド判断指標を組み合わせることで、潜在的なトレンド反転ポイントを効果的に判断できます。広範囲に適用可能で最適化が容易であるという利点がある一方、一定のリスクも存在するため、注意して対策を講じるとともに、継続的な最適化が必要です。総じて、この戦略は汎用性が高く実用的な短期反転売買戦略であり、十分に研究・応用する価値があります。

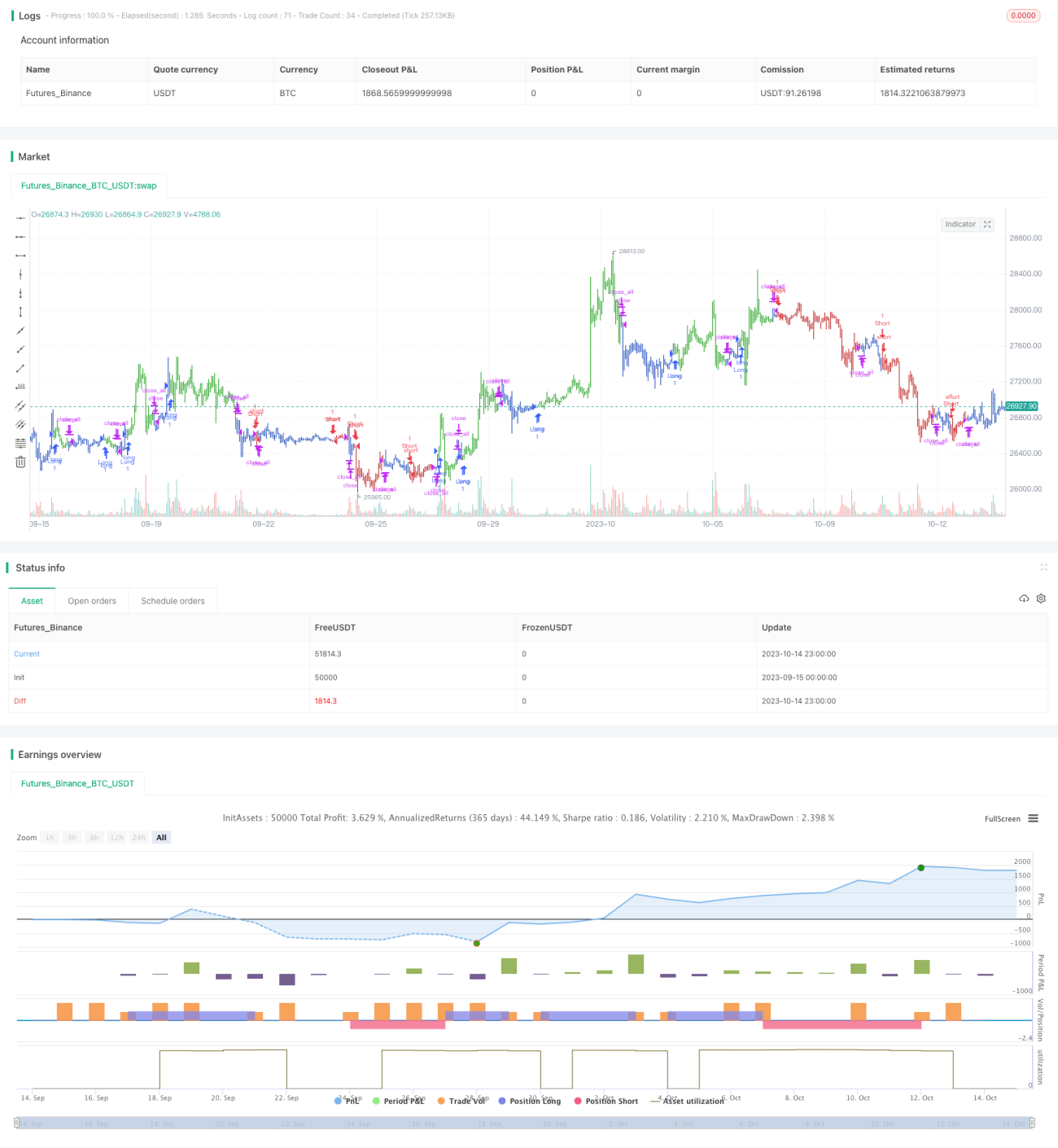

/*backtest

start: 2023-09-15 00:00:00

end: 2023-10-15 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 20/07/2021

// This is combo strategies for get a cumulative signal. - 1