ダブル移動平均線ボリンジャーバンドトレンドフォロー戦略

概要

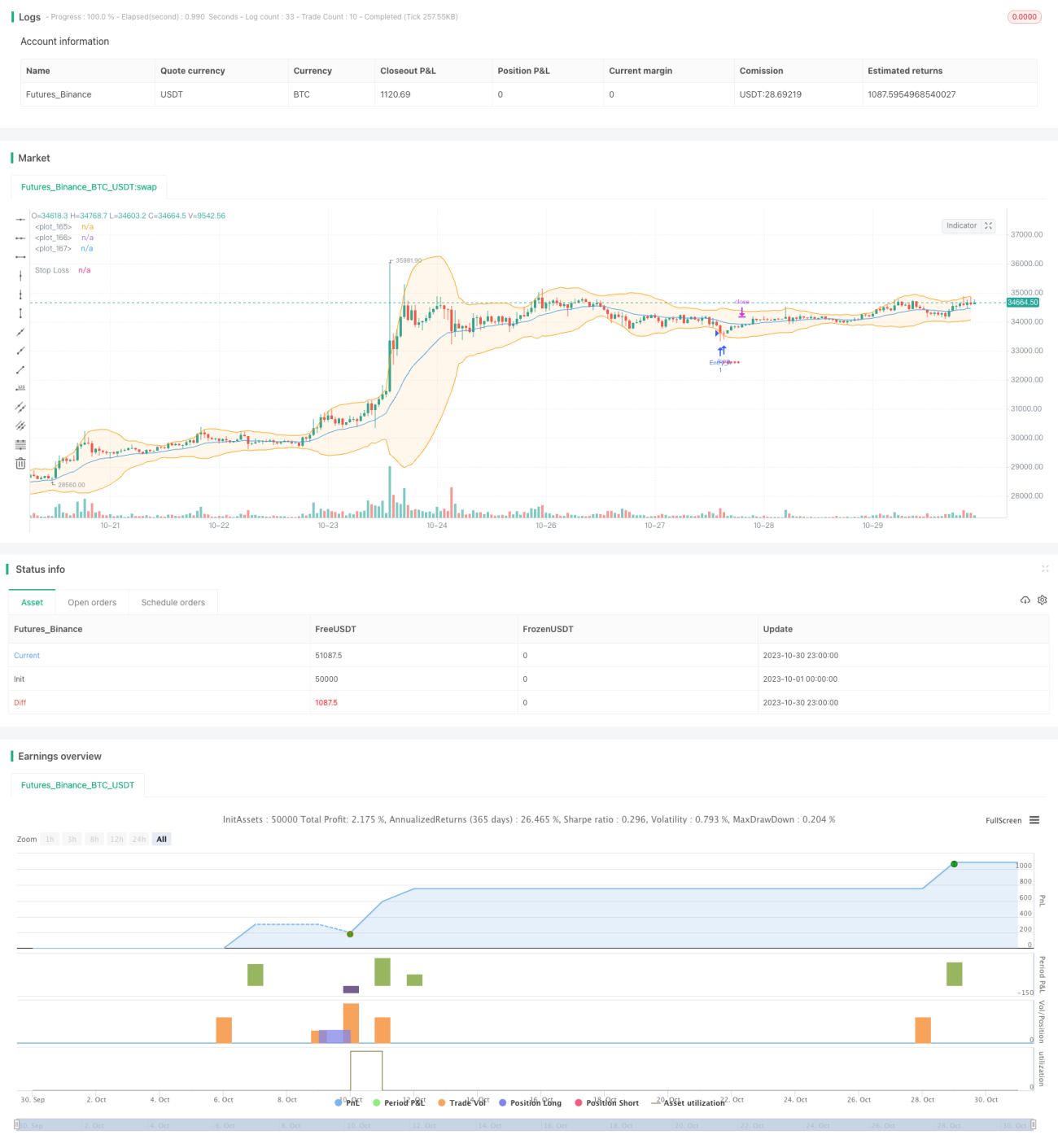

本戦略は、ボリンジャーバンドの二重移動平均線に基づくトレンドフォロー型の取引判断を行います。ボリンジャーバンドの上下バンドの収束と拡散を利用してトレンドの変化を判断し、下限バンド付近で買い、上限バンド付近で売ることで安値買い高値売りを実現し、利益確定を行います。

戦略の原理

本戦略は、ボリンジャーバンドのシンプルバージョンとエンハンスドバージョンの2つを同時に適用します。

シンプルバージョンのボリンジャーバンドは終値のSMAで中央線を計算し、エンハンスドバージョンは終値のEMAで中央線を計算します。

上下のバンドはいずれも中央線 ± N倍の標準偏差で算出されます。

戦略は、ボリンジャーバンドの上下バンド間のスプレッドを基にトレンドを判断します。スプレッドが設定した閾値より小さい場合、トレンド域に入っているとみなし、トレンドフォロー取引を開始します。

具体的には、価格が下限バンドに近づいたときに買い(ロング)エントリーし、上限バンドに近づいたときに売りでポジションをクローズします。損切りは固定パーセント方式とし、必要に応じてトレーリングストップも選択可能です。

目標利益は、中央線または上限バンド付近でのクローズを選択するかによって決まります。

また、本戦略では利益確定時のみ売却するオプションも選択でき、損失の拡大を防ぎます。

優位性分析

本戦略には以下の優位性があります。

-

二重ボリンジャーバンドの組み合わせによる判断効率の向上

シンプルバージョンとエンハンスドバージョンを適用することで、両者の効果を比較し、より優れたバージョンを選択できるため、判断効率が向上します。

-

ボリンジャーバンドのバンド幅によるトレンド度合いの判断

ボリンジャーバンドのバンド幅が狭まるとき、トレンド相場に入ったことを示し、このタイミングでトレンドフォロー取引を行うと勝率が高まります。

-

柔軟な利確・損切りの方法

固定パーセントの損切りで1回の損失をコントロールします。また、中央線または上限バンド付近での利確、トレーリングストップの有効化により、さらなる利益の確保が可能です。

-

損失拡大防止の保護機能

利益確定時のみ売却することで、損失の拡大を防ぐことができます。

リスク分析

本戦略には以下のリスクも存在します。

-

ドローダウンリスク

トレンドフォロー取引自体には一定のドローダウンリスクが伴い、連続的な損失に耐える心理的負担が生じます。

-

レンジ相場リスク

ボリンジャーバンドのバンド幅が広いとき、相場がレンジに入っている可能性があり、その場合本戦略の効果は低下します。トレンドが再形成されるまで取引を休止する必要があります。

-

損切り発動リスク

固定パーセントの損切りは過激すぎる場合があり、ATRベースの損切りなど、より穏やかな方法への調整が求められます。

最適化の方向性

本戦略は以下の点から最適化が可能です。

-

ボリンジャーバンドパラメータの最適化

異なる移動平均パラメータや標準偏差倍率をテストし、異なる市場に適したボリンジャーバンドパラメータの組み合わせを見つけることができます。

-

他のインジケーターによるフィルターの追加

ボリンジャーバンドのシグナルに加えて、MACDやKDなどのインジケーターによるフィルターを追加することで、レンジ相場での取引を減らせます。

-

利確・損切り戦略の最適化

異なるトレーリングストップ方式や、振幅・ATRなどの指標に基づく損切りポイントの最適化をテストできます。

-

資金管理の最適化

1回の取引におけるポジションサイズ管理や、異なるナンピン戦略のテストが可能です。

まとめ

本戦略は二重ボリンジャーバンドの利点を統合し、バンド幅からトレンド度合いを判断し、トレンド中に安値で買い、高値で売るトレーリング取引を行います。同時に、科学的な損切りメカニズムを設定してリスクをコントロールします。パラメータの最適化や他のインジケーターによるフィルター追加により、安定性をさらに高めることが可能です。

- 1