マイク分解とマルチタイムフレーム移動平均線戦略

概要

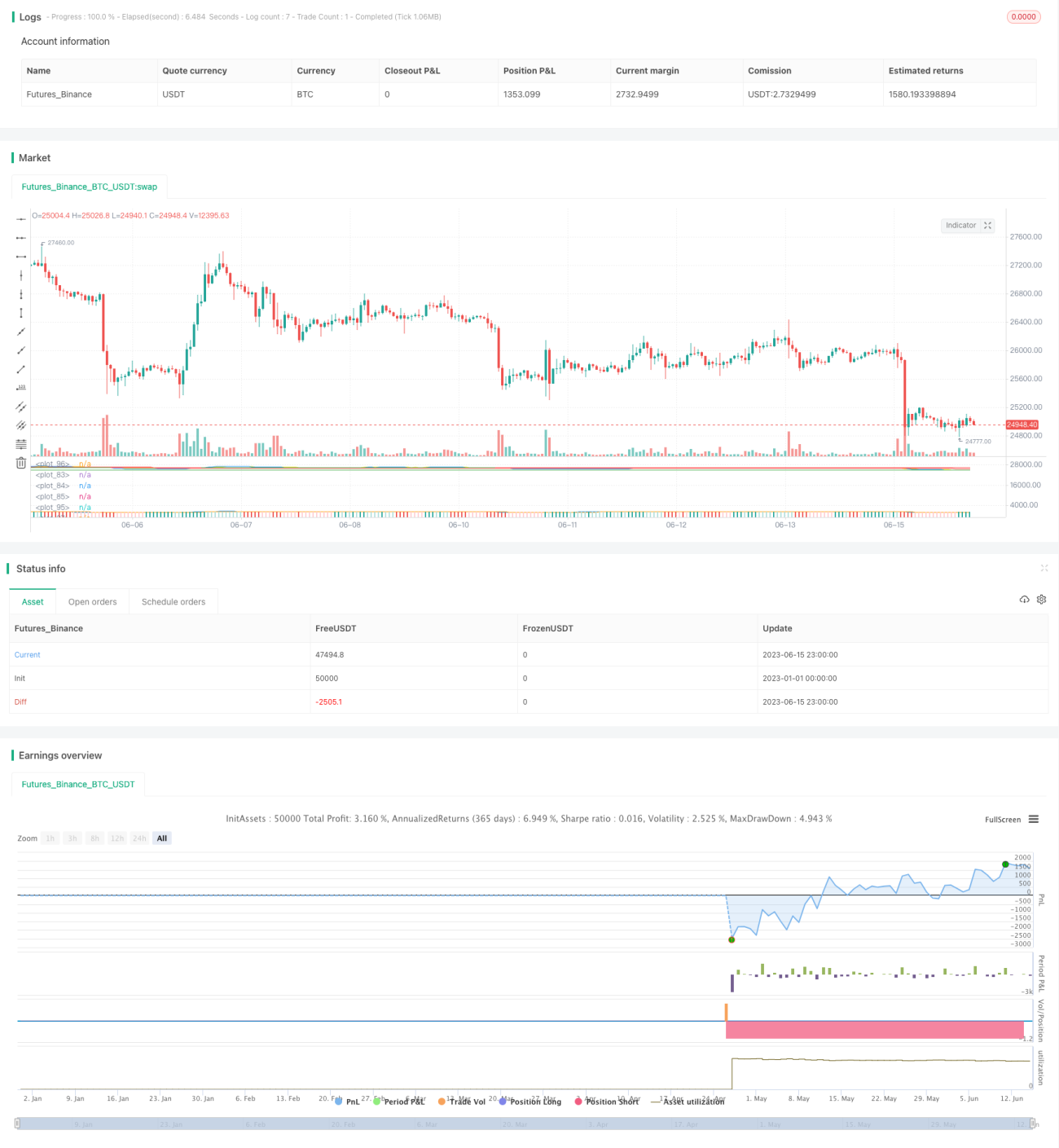

本戦略は、MACD(マックD)インジケーターとマルチタイムフレーム移動平均線を融合し、トレンドとトレンド反転シグナルを組み合わせたロング・ショート双方向取引戦略です。トレンド相場で追加利益を得ると同時に、反転の機会を捉えることができます。

戦略の仕組み

-

2組の異なる期間のEMA移動平均線をマルチタイムフレームフィルターとして使用し、ロング・ショートの方向を判断します。15分の短期EMAが1時間の長期EMAを上回っている場合は強気フィルター、15分の短期EMAが1時間の長期EMAを下回っている場合は弱気フィルターとします。

-

MACDにダイバージェンス(ヒストグラムと価格の乖離)が形成された場合、反転の可能性があると判断します。

-

強気フィルターが有効な場合、強気ダイバージェンス(価格が新高値を更新したがMACDは新高値を更新していない)を発見したら、MACDがゼロラインを上抜けるのを待って買いエントリー。弱気フィルターが有効な場合、弱気ダイバージェンス(価格が新安値を更新したがMACDは新安値を更新していない)を発見したら、MACDがゼロラインを下抜けるのを待って売りエントリー。

-

ストップロスはトレーリングストップ方式で、最高値・最安値の変動幅に基づいて計算します。テイクプロフィットはストップロスの一定倍率とします。

-

MACDヒストグラムがゼロラインをクロスした時点でポジションをクローズします。

優位性分析

-

マルチタイムフレームEMAの組み合わせにより、大きな周期のトレンドを判断でき、逆張り取引を回避できます。

-

MACDダイバージェンスは価格反転の機会を捉えることができ、反転戦略に適しています。

-

動的トレーリングストップは利益を確定し、損失の拡大を防ぎます。

-

ストップロスに基づいてテイクプロフィットの距離を計算することで、期待リターンを得られます。

リスク分析

-

EMA移動平均線の組み合わせをフィルターとして使用するため、レンジ相場では方向判断を誤る可能性があります。

-

MACDダイバージェンス後の反発幅が不十分で、利益を得られない可能性があります。

-

ストップロスの距離設定が不適切な場合、緩すぎたり狭すぎたりする可能性があります。

-

反転の余地が不十分で、利益が制限される可能性があります。

-

反転エントリーのタイミングを適切に捉える必要があり、早すぎても遅すぎても損失につながる可能性があります。

最適化の方向性

-

異なるパラメータのEMAをテストし、より正確なトレンド判断を得ることができます。

-

MACDのパラメータをより感度の高い組み合わせに調整してみることも可能です。

-

異なるストップロス・テイクプロフィット比率の設定をテストできます。

-

より高次のタイムフレームEMAを追加して全体的なトレンドを判断するなど、偽の反発に陥らないよう追加のフィルター条件を組み込むことができます。

-

反転エントリーの確認条件を最適化し、反転トレンドが十分に成熟していることを確認できます。

まとめ

本戦略は、トレンドフィルター、トレンド反転シグナル、動的ストップロス・テイクプロフィット管理などを総合的に活用し、順張りにも逆張りにも対応できます。パラメータ調整やフィルター条件の最適化により、より幅広い市場環境に適応し、リスク管理のもとで安定した収益を得ることが可能です。本戦略は一定の汎用性と実用価値を持ち、マルチタイムフレームとインジケーターの融合活用の代表的な例と言えます。

- 1