ダブルMA順張りブレイクアウト戦略

概要

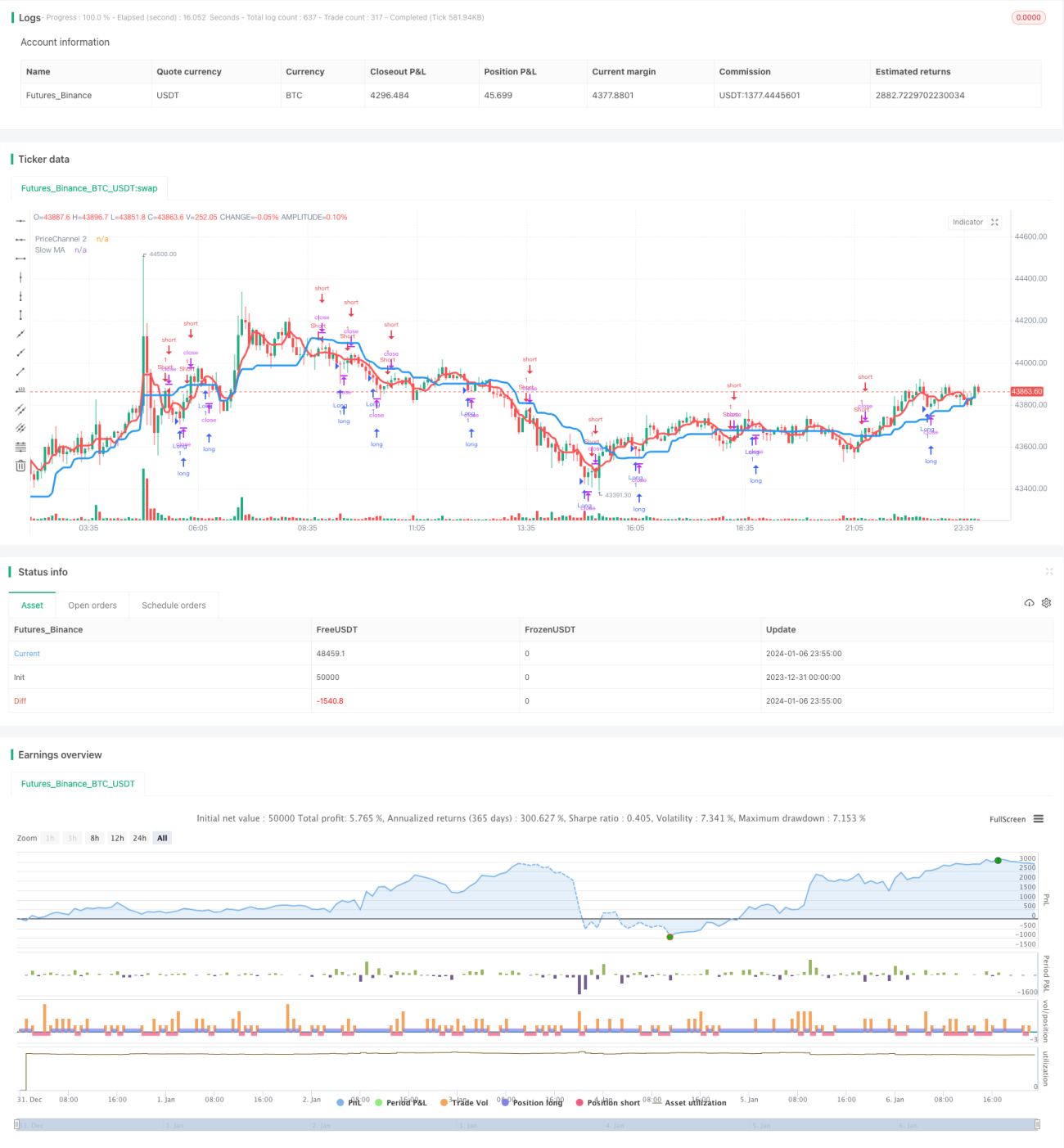

ダブルMA順張りブレイク戦略は、異なる期間の2本の移動平均線を利用してトレンドを判断し、エントリーする定量取引戦略です。主に遅いMAで全体トレンドの方向を判断し、速いMAでエントリーのフィルターとして機能します。大勢のトレンド方向が一致した場合に、反転ローソク足でエントリーし、高い勝率と収益率を追求します。

戦略の原理

この戦略は主に以下の要素で構成されています。

トレンド判断: 21期間のMA(遅いMAとして定義)を計算します。このMAは比較的安定しており、全体のトレンド方向を判断するために使用します。価格が上昇する際にこのMAに近づけば上昇トレンド、下落する際に近づけば下降トレンドと判断します。

エントリーフィルター: 5期間のMA(速いMAとして定義)を計算します。価格が遅いMAをブレイクしたときに、同時に速いMAもブレイクした場合のみ、売買シグナルが発生します。この設計は、偽のブレイクの可能性をさらにフィルタリングするためのものです。

ローソク足フィルター: 戦略は、その期間のローソク足が陰線の場合のみ買い、または陽線の場合のみ売りを行います。これは反転ローソク足でエントリーすることで成功率が高まると考えられるためです。同時に、短期RSI指標を組み合わせることで、過度な買われすぎや売られすぎの領域でのエントリーを回避します。

ポジション追加フィルター: 暗号通貨市場向けに、戦略はさらに3倍のボラティリティブレイクによるポジション追加条件を追加し、大きな下落局面での売られすぎの機会を選別します。

ストップロス設計: 戦略はトレーリングストップロスをサポートします。ポジション保有中は、設定したストップロス割合に基づいてリアルタイムでストップロス水準を更新します。

優位性分析

この戦略には以下のような利点があります。

- ダブルMAの設計はシンプルで実用的であり、容易に理解・習得できます。

- 速いMAと遅いMAの組み合わせによるフィルターで、信頼性の高いトレンド判断が可能です。

- 反転ローソク足でのエントリーにより、取引勝率が向上します。

- 全体的な方法論は保守的で堅実であり、あらゆる時間軸の取引に適しています。

- トレーリングストップロスに対応しており、リスクをコントロールできます。

- 特に暗号通貨市場の特性を考慮し、売られすぎ時のポジション追加機会を組み込むことで、超過収益が期待できます。

リスク分析

この戦略には以下のようなリスクも存在します。

- ダブルMAがレンジ相場の場合、小さな損益が繰り返し発生する可能性があります。

- 反転ローソク足でのエントリーは、特定の時間帯では勝率が低くなる場合があります。

- 暗号通貨市場のボラティリティが高いため、ストップロスが発動する確率が高くなります。

- 売られすぎ時のポジション追加機会はそれほど多くなく、リターンの変動が大きくなります。

これらのリスクに対しては、以下のような最適化が考えられます。

- エントリー条件を追加し、無効なレンジ相場での取引を回避します。

- ローソク足の期間を調整するか、他の指標によるフィルターを追加します。

- ストップロスアルゴリズムを最適化し、中心付近でのストップロスを追跡します。

- 売られすぎ時のポジション追加戦略の実際の効果を評価します。

最適化の方向性

この戦略は主に以下の点で最適化が可能です。

-

パラメータ最適化: より体系的なバックテストを通じて、速いMAと遅いMAの期間パラメータの組み合わせを最適化し、全体的なリスク対リターン比を向上させます。

-

パターン認識: KDJやMACDなど他の指標を追加し、より信頼性の高い反転シグナルを識別します。

-

ストップロス最適化: フローティングストップロスやトレーリングストップロスなどのアルゴリズムを開発し、ストップロスが発動する確率を低減します。

-

機械学習: より多くの過去データを収集・ラベリングし、機械学習手法を用いて自動的に取引ルールを生成します。

-

定量ポジション管理: 市場の状態に応じて、ポジション管理戦略を自動調整します。

まとめ

ダブルMA順張りブレイク戦略は、全体的に見てシンプルで実用的なトレンド追従戦略です。複雑な機械学習アルゴリズムと比較して、この戦略は説明や習得が容易であり、信頼性も比較的高いです。パラメータ最適化、機能拡張、機械学習の導入により、この戦略は大きな改善の可能性を秘めており、定量取引の良い出発点となります。

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title = "Noro's Trend MAs Strategy v2.0 +CB", shorttitle = "Trend MAs str 2.0", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

//Settings- 1