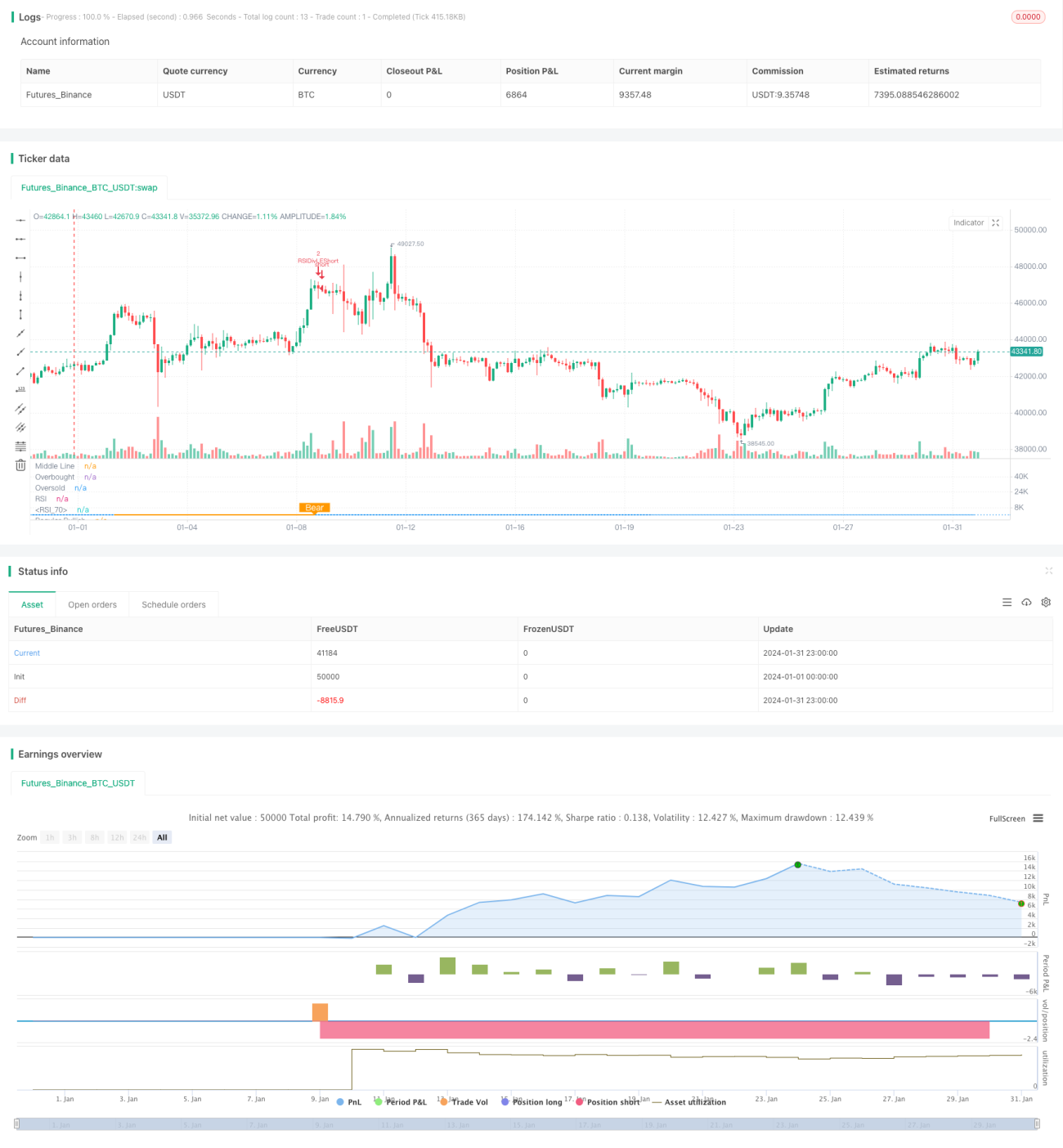

RSI指標の多空分離取引戦略

1

Follow

1802

Followers

概要

本戦略は、RSIインジケーターを用いて買いと売りの乖離現象を識別し、それに基づいて取引判断を行います。核となる考え方は、価格が新安値を付けたにもかかわらずRSIが新高値を示した場合、「買い乖離」シグナルが発生し、底値が形成されたと判断して買いポジションを取ります。逆に、価格が新高値を付けたにもかかわらずRSIが新安値を示した場合、「売り乖離」シグナルが発生し、天井が形成されたと判断して売りポジションを取ります。

戦略の原理

本戦略は主にRSIインジケーターを用いて価格とRSIの間の買い・売り乖離現象を識別します。具体的な方法は以下の通りです。

- RSIインジケーターのパラメータは13、元データは終値を使用します。

- 買い乖離の左方向の遡及範囲を14日、右方向の遡及範囲を2日と定義します。

- 売り乖離の左方向の遡及範囲を47日、右方向の遡及範囲を1日と定義します。

- 価格がより低い安値を更新したが、RSIがより高い安値を示した場合、買い乖離条件を満たし、買いシグナルが発生します。

- 価格がより高い高値を更新したが、RSIがより低い高値を示した場合、売り乖離条件を満たし、売りシグナルが発生します。

価格とRSIの間の買い・売り乖離現象を識別することで、価格トレンドの転換点を事前に捉え、取引判断を行うことができます。

戦略の利点

本戦略には主に以下の利点があります。

- 価格とRSIの間の買い・売り乖離現象を識別することで、価格トレンドの転換点を事前に判断し、取引機会を捉えることができます。

- 指標分析を利用しているため、主観的な感情の影響を受けません。

- 固定された遡及区間で乖離現象を識別するため、パラメータ調整の頻度が少なくて済みます。

- 日足のRSIなどの追加条件を組み合わせることで、誤取引の確率を減らすことができます。

リスクと解決方法

本戦略には以下のようなリスクも存在します。

- RSIのダイバージェンスが発生しても必ずしも価格が即座に反転するとは限らず、タイムラグが生じる可能性があり、その結果ストップロスが発動されるリスクがあります。解決策としては、ストップロスの幅を適度に広げ、価格が乖離シグナルを確定させるための十分な時間を確保することです。

- 乖離現象が長時間続くとリスクが増大します。解決策としては、より長期の日足または週足のRSIをフィルター条件として組み合わせることです。

- 乖離の幅が小さすぎるとトレンド転換を確定できません。そのため、遡及区間を適度に拡大し、より明確なRSI乖離を探す必要があります。

戦略の最適化方向

本戦略は以下の方向で最適化が可能です。

- RSIパラメータを最適化し、最適なパラメータの組み合わせを探す。

- MACDやKDなどの他のテクニカル指標を試し、買い・売り乖離現象を識別する。

- 適切なレンジ相場のフィルター条件を追加し、レンジ相場での誤取引を減らす。

- より多くの時間足のRSIを組み合わせ、最適な組み合わせシグナルを探す。

まとめ

RSIによる買い・売り乖離取引戦略は、RSIと価格の間の買い・売り乖離現象を識別することで、価格トレンドの転換点を判断し、それに基づいて取引シグナルを生成します。本戦略はシンプルで実用的であり、パラメータ設定の最適化やフィルター条件の追加により、収益確率をさらに高めることができます。総じて、RSIによる買い・売り乖離戦略は非常に効果的な定量取引戦略です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1