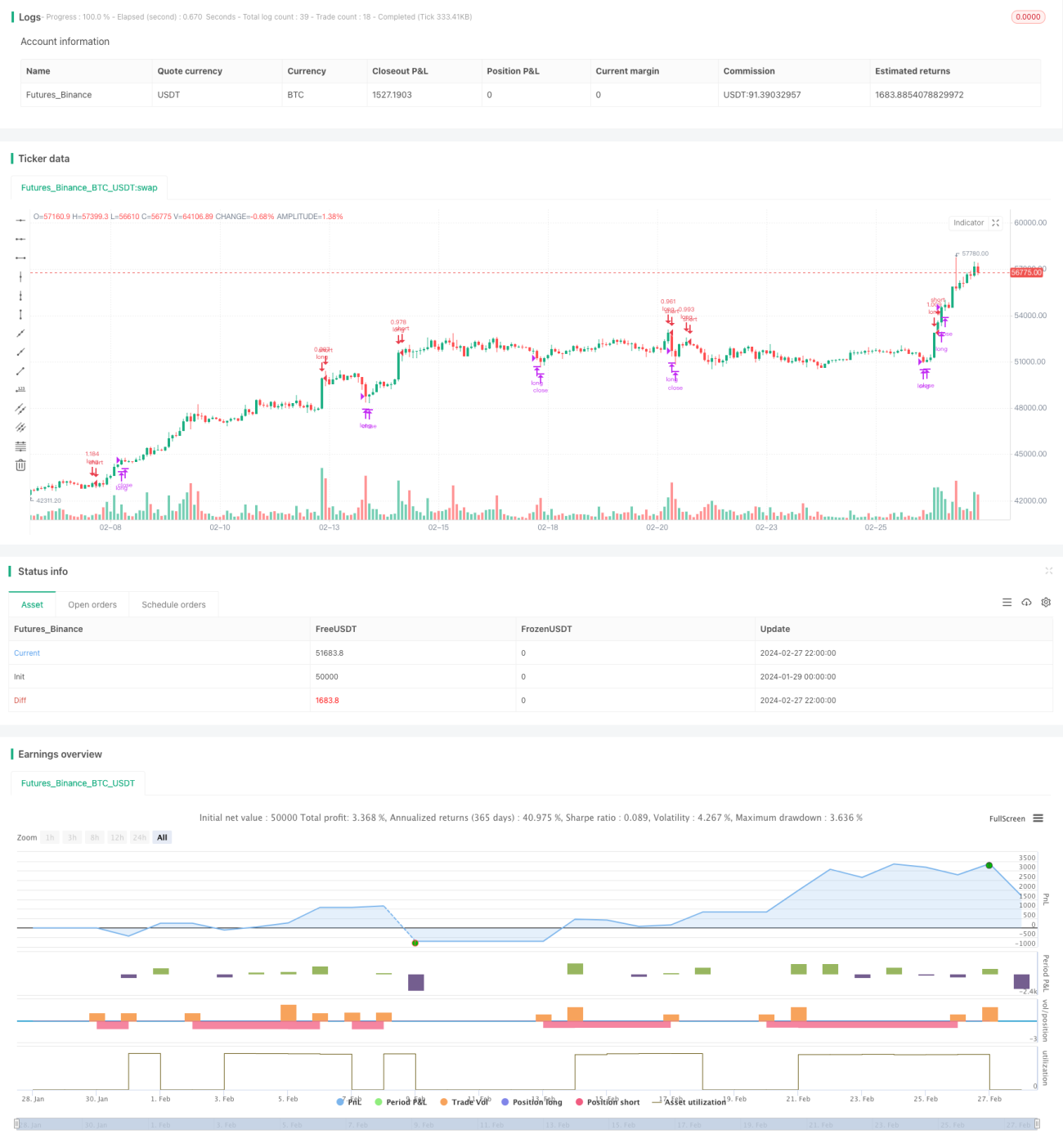

モメンタム指標と移動平均線を組み合わせたロング戦略

1

Follow

1802

Followers

概要

本戦略はMACDモメンタム指標とDMIトレンド指標を組み合わせ、条件を満たした場合にロングポジションを取ります。エグジットは固定利確とカスタマイズされたボラティリティトレーリングストップにより利益を確定します。

原理

エントリーはMACDとDMI指標に依存します。

- MACDがプラス(MACDラインがシグナルラインより上)の場合、市場の上昇モメンタムが強まっていることを示します。

- DMIにおいてDI+がDI-より高い場合、市場が上昇トレンドにあることを示します。

これら2つの条件が同時に満たされた場合、ロングポジションを開始します。

ポジションのエグジットには2つの基準があります。

- 固定利確:クローズ価格が設定されたパーセンテージ上昇したときに利確します。

- ボラティリティトレーリングストップ:ATRと最近の最高値から動的に調整されるストップ位置を計算します。これにより、市場のボラティリティに応じてトレーリングストップロスを設定できます。

利点

- MACDとDMIの組み合わせにより、市場のトレンド方向を比較的信頼性高く判断でき、誤った取引を減らせます。

- 利確条件に固定利確とボラティリティストップを組み合わせることで、柔軟に利益を確定できます。

リスク

- MACDとDMIはどちらも偽シグナルを発生させる可能性があり、不要な損失を招く恐れがあります。

- 固定利確により利益を最大化できない可能性があります。

- ボラティリティストップのトレール速度が適切に調整されず、過激または保守的になる可能性があります。

最適化の方向性

- 他の指標(例:KDJ指標による買われすぎ/売られすぎの判断)を追加してエントリーシグナルをフィルタリングすることを検討できます。

- 異なるパラメータをテストし、より良い利確・ストップ効果を得ることができます。

- 取引対象に応じて移動平均線などのパラメータを調整し、システムを最適化できます。

まとめ

本戦略は複数の指標を組み合わせて市場のトレンドと条件を判断し、確率の高い有利な状況で参入します。利確条件も最適化されており、一定の利益を確保しつつ、利益確定の柔軟性も考慮されています。パラメータ調整とさらなるリスク管理により、本戦略は安定した出力を提供する定量取引システムとなり得ます。

Source

Pine

/*backtest

start: 2024-01-29 00:00:00

end: 2024-02-28 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='(MACD + DMI Scalping with Volatility Stop',title='MACD + DMI Scalping with Volatility Stop by (Coinrule)', overlay=true, initial_capital = 100, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.1)

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1