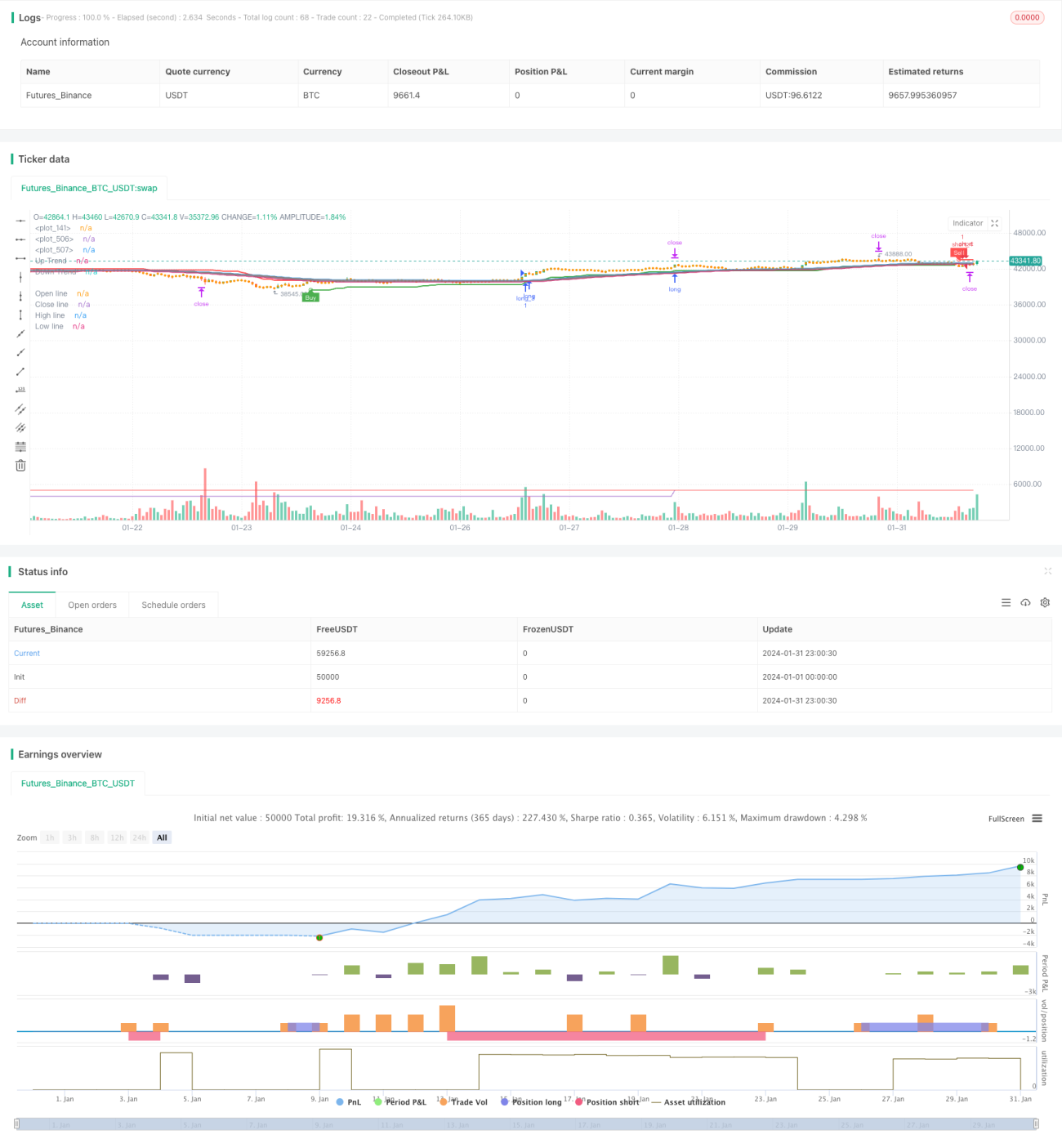

三重確認トレンド追跡戦略

概要

三重確認トレンド追跡戦略は、移動平均線、イチモク雲(意憶線)、スーパートレンドの3大指標のシグナルを組み合わせることで、トレンドを高い確率で捉えます。3つの指標すべてが同時に買いまたは売りシグナルを発した場合、戦略は即座にエントリーしてトレンドに追随し、トレンドが反転した場合には迅速に損切りし、逆張りで空売りを行います。

戦略の原理

移動平均線による主要トレンドの判断

戦略は52期間の移動平均線を使用して主要トレンドの方向を判断します。価格が移動平均線を上抜けた場合は上昇トレンド、下抜けた場合は下降トレンドと判断します。

イチモク雲による二次的な反転の識別

戦略は同時にイチモク雲(意忘線)を使用して短期的な二次的反転を識別します。イチモク雲の計算方法は移動平均線と似ていますが、CLOSE価格の代わりに始値を用いることで、価格反転情報をより迅速に反映します。価格が下降中のイチモク雲を上抜けた場合、価格が短期的に安定し反発するシグナルを示し、価格が上昇中のイチモク雲を下抜けた場合、価格が短期的に下落するシグナルを示します。

スーパートレンドによる反転ポイントの判断

戦略はさらにスーパートレンド指標を組み合わせて、重要な反転ポイントを判断します。スーパートレンド指標はATR指標のウィンドウ期間と価格データを組み合わせ、チャネルの上限・下限を動的に調整することで、反転のタイミングを判断します。

三重確認によるシグナルフィルター

移動平均線、イチモク雲、スーパートレンドの3つの指標がすべて同時に買いシグナルを発した場合のみ、戦略はロングを行います。3つの指標すべてが同時に売りシグナルを発した場合のみ、ショートを行います。三重の指標確認により、偽シグナルを効果的にフィルタリングし、エントリーの確率を高めます。

優位性分析

多次元的な判断による高確率

戦略は移動平均線、イチモク雲、スーパートレンドの3つの指標を組み合わせ、異なる次元からトレンドと重要ポイントを判断し、高確率なエントリーを確保します。

迅速な反応とリアルタイム追跡

イチモク雲の導入により、戦略は価格の短期的な反転に迅速に対応できます。また、ATR適応型チャネルのスーパートレンド指標は、価格変動をリアルタイムで追跡します。

自動利確・損切りによるリスク管理の効果

戦略には自動利確・損切りのロジックが組み込まれており、ATRに基づいて利確・損切りポイントを動的に調整し、1回の損失を効果的に抑制します。

リスクと解決方法

取引頻度が高すぎるリスク

戦略のシグナルが頻繁に発生するため、過剰取引につながる可能性があります。移動平均線の期間パラメータを適度に大きくして、取引頻度を減らすことができます。

反転の不確実性リスク

イチモク雲とスーパートレンド指標による反転ポイントの判断は確実ではなく、誤判定のリスクがあります。指標パラメータにフィルター条件を追加し、より確率の高い反転シグナルを確保できます。

レンジ相場での損失リスク

レンジ相場では、価格が繰り返しクロスするため、戦略は頻繁にポジションを開き、すぐに損切りすることになり、損失リスクが生じます。レンジ相場を識別し、その局面では戦略の取引を停止することができます。

最適化の方向性

ボラティリティ指標との組み合わせ

ボラティリティ系指標、例えばボリンジャーバンドを組み合わせることを検討できます。価格がボリンジャーバンドの上限・下限に近づいた場合、新規ポジションを避けることで、レンジ相場のリスクを効果的に回避できます。

エントリーフィルター条件の追加

KDJやMACDなどの補助判断指標を追加し、それらも同時にシグナルを発した場合のみエントリーすることで、さらに偽シグナルをフィルタリングし、不要な取引を減らすことができます。

利確・損切り戦略の最適化

トレーリングストップ、指数移動トレーリングストップ、半倉間隔利確などの方法を用いて利確・損切り戦略を最適化し、利益をより安定して大きくすることができます。

まとめ

三重確認トレンド追跡戦略は、移動平均線、イチモク雲、スーパートレンドの3大指標の利点を最大限に活用し、トレンドを高い確率で判断・捕捉します。同時に自動利確・損切りメカニズムを設定することで、1回の損失を効果的に抑制します。さらに他の補助指標を組み合わせてエントリーをフィルタリングしたり、利確・損切り戦略を改良してより実用的な戦略に改善することが期待されます。

- 1