개요

이중 반전 전략은 123 반전과 3일 반전 패턴을 결합한 퀀트 전략으로, 거래 신호의 품질을 높이고 리스크를 줄이는 데 목적이 있습니다. 해당 전략은 차액 지표와 캔들 패턴 지표를 결합한 거래 방식을 사용하며, 두 지표가 동시에 신호를 발생시킬 때 거래를 실행하여 신호의 정확도를 높입니다.

전략 원리

이중 반전 전략은 서로 다른 두 가지 거래 전략을 결합합니다. 먼저 123 반전 전략은 차액 지표를 활용하며, 연속 2일간 종가가 반전되고 스토캐스틱 지표가 임계값을 돌파할 때 신호를 발생시킵니다. 다른 하나는 3일 반전 패턴 전략으로, 3일간의 캔들을 관찰하여 중간일 저점이 형성되고 마지막 날 종가가 전일 고가보다 높을 때 신호를 발생시킵니다. 두 전략이 동시에 같은 방향의 신호를 발생시키면 매수 또는 매도가 실행됩니다.

구체적으로, 123 반전 전략은 9일 스토캐스틱 지표를 사용하여 과매수/과매도 상태를 판단합니다. 가격이 2일 연속 하락하고 스토캐스틱이 50 이하일 때 매수 신호, 2일 연속 상승하고 스토캐스틱이 50 이상일 때 매도 신호를 발생시킵니다. 3일 반전 패턴 전략은 3일 동안 가격이 먼저 상승 후 하락 후 다시 상승하는 패턴이 나타나는지 감지합니다. 이는 단기 과매도가 반전되었음을 나타내는 신호입니다.

이중 반전 전략은 두 전략이 동시에 신호를 발생시킬 때만 포지션을 오픈합니다. 이는 가짜 신호 비율을 크게 낮추어, 시스템이 높은 확률의 기회에서만 거래하도록 합니다.

장점 분석

단일 전략에 비해 이중 반전 전략은 다음과 같은 장점이 있습니다.

- 신호 품질 향상, 가짜 신호 감소

- 이중 지표 검증으로 손실 확률 감소

- 단기 및 중기 반전 기회를 효과적으로 포착

- 이해 및 구현이 용이

리스크 및 해결 방안

이중 반전 전략의 주요 리스크는 일부 기회를 놓칠 수 있다는 점입니다. 신호 조건이 까다롭기 때문에 단일 지표의 거래 기회 중 일부를 놓칠 수 있습니다. 매개변수를 조정하여 한 지표의 조건을 완화함으로써 거래 빈도를 부분적으로 높일 수 있습니다.

또 다른 리스크는 일부 극단적인 시장 상황에서 두 지표가 동시에 실패할 확률이 높아진다는 점입니다. 이러한 경우 손절매 매커니즘을 추가하여 포지션을 신속히 청산하고 손실을 줄일 수 있습니다. 또는 과거 경험을 통해 극단적인 시장 상황의 특징이 확인된 경우 거래 신호를 무시하고 포지션 오픈을 피할 수 있습니다.

최적화 제안

이중 반전 전략은 다음과 같은 측면에서 지속적으로 최적화할 수 있습니다.

- 스토캐스틱 지표 매개변수 조정하여 과매수/과매도 판단 정확도 향상

- 다양한 거래 종목에서 효과를 테스트하여 최적의 적용 대상 탐색

- 머신러닝 모델을 추가하여 신호 정확도 향상

- 거래량 변화,日内 변동성 등 더 많은 시장 통계적 특성을 결합하여 최적의 진입 시점 파악

요약

이중 반전 전략은 반전 거래 아이디어와 캔들 패턴 분석을 성공적으로 결합했습니다. 가격의 단기 및 중기 회귀 본질을 충분히 활용하여 반전이 제공하는 기회를 효과적으로 포착합니다. 단순한 추세 추종 방식과 비교하여 본 전략은 리스크 관리와 수익 사이의 균형을 찾았습니다. 지속적인 최적화와 혁신을 통해 그 투자 가치는 계속해서 입증될 것입니다.

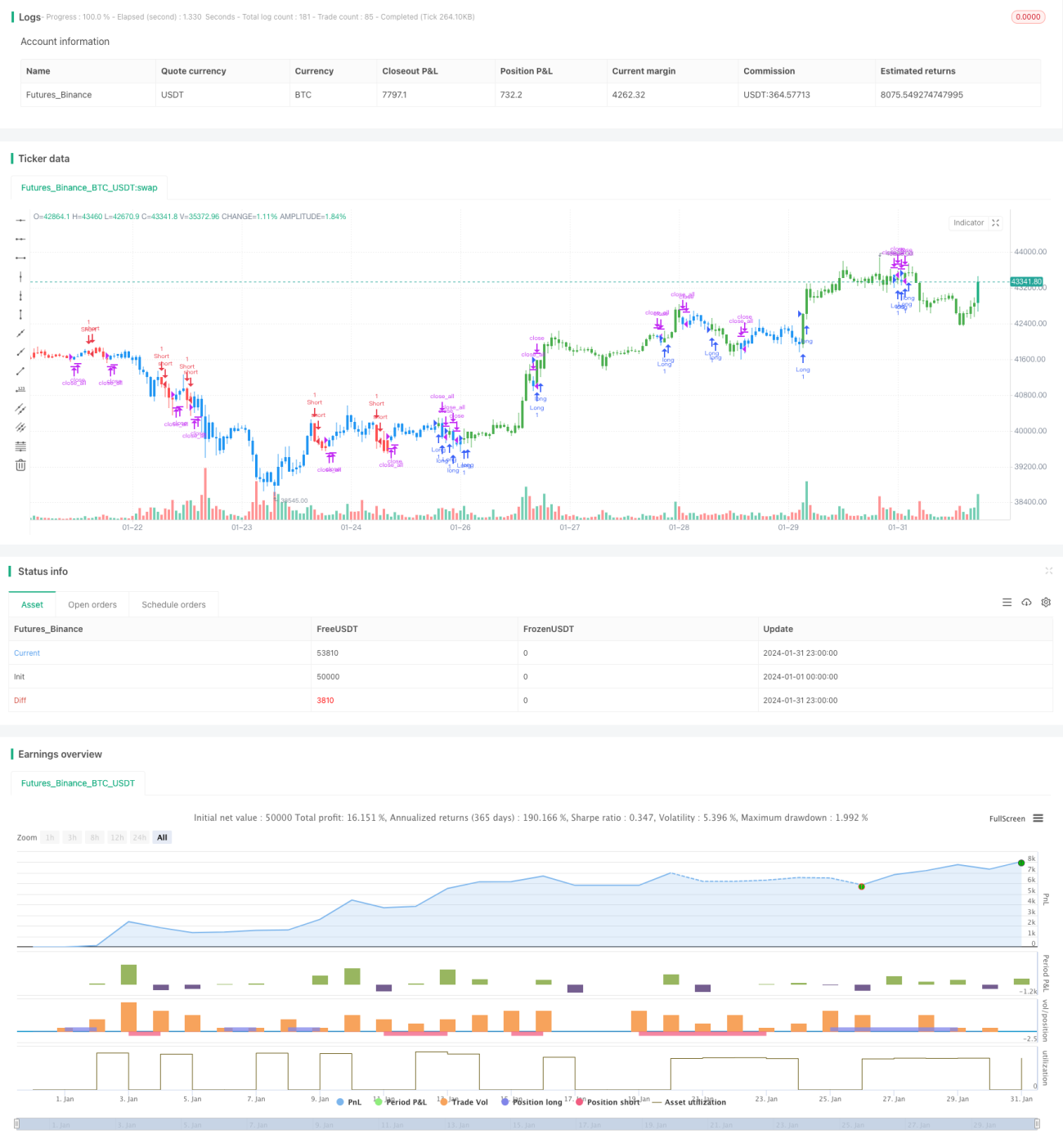

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 17/04/2019

// This is combo strategies for get - 1