RSI 지표 매수/매도 분리 트레이딩 전략

1

Follow

1802

Followers

개요

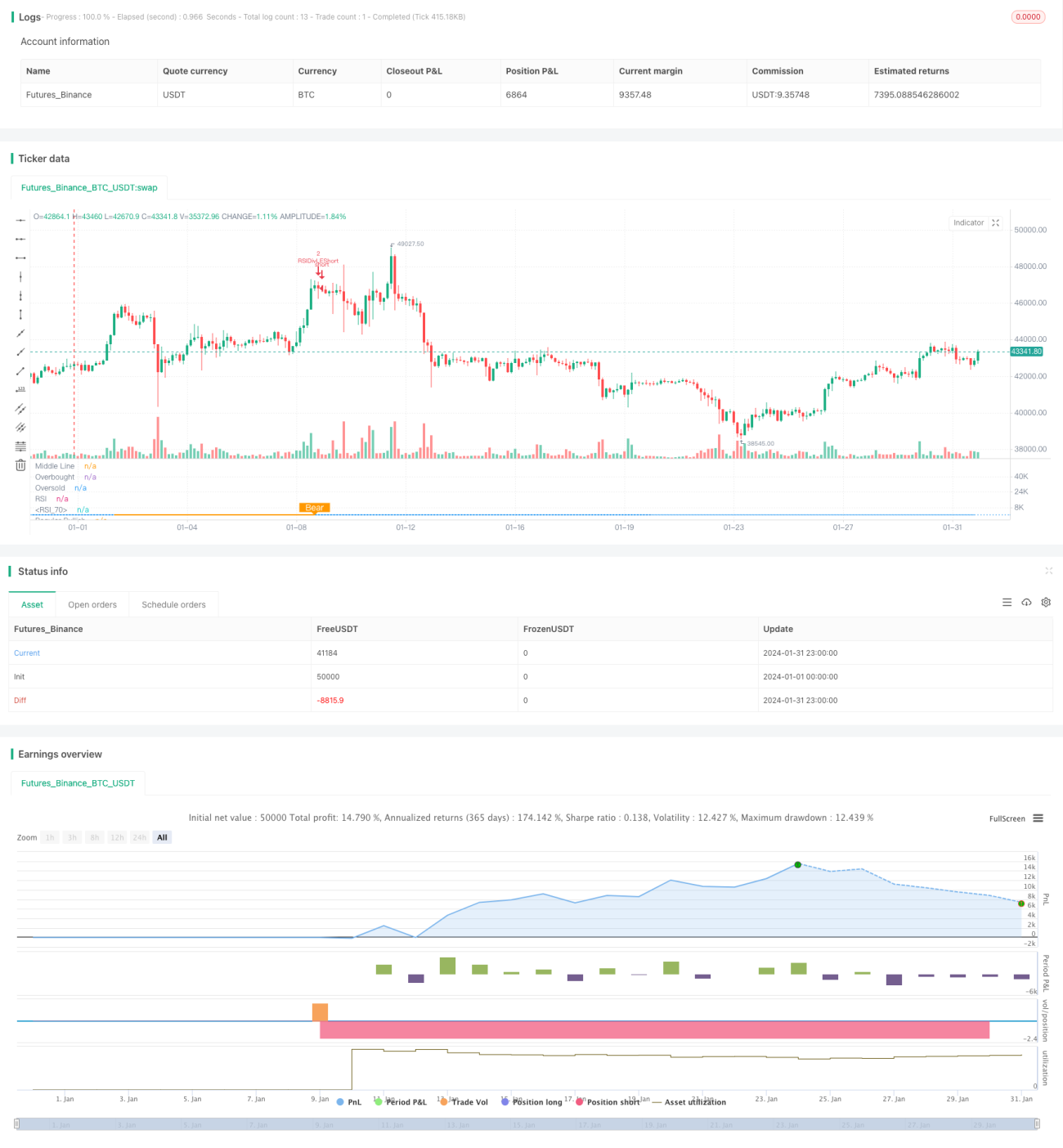

이 전략은 RSI 지표를 사용하여 강세 및 약세 다이버전스 현상을 식별하고 이를 기반으로 매매 결정을 내립니다. 핵심 아이디어는 가격이 새로운 저점을 기록했지만 RSI 지표가 새로운 고점을 기록할 때 ‘강세 다이버전스’ 신호가 발생하며 이는 바닥이 형성되었음을 의미하여 매수하고, 가격이 새로운 고점을 기록했지만 RSI 지표가 새로운 저점을 기록할 때 ‘약세 다이버전스’ 신호가 발생하며 이는 고점이 형성되었음을 의미하여 매도하는 것입니다.

전략 원리

이 전략은 주로 RSI 지표를 사용하여 가격과 RSI 간의 다이버전스 현상을 식별하며, 구체적인 방법은 다음과 같습니다.

- RSI 지표의 파라미터는 13이며, 소스 데이터는 종가입니다.

- 강세 다이버전스의 좌측 회고 범위는 14일, 우측 회고 범위는 2일로 정의합니다.

- 약세 다이버전스의 좌측 회고 범위는 47일, 우측 회고 범위는 1일로 정의합니다.

- 가격이 더 낮은 저점을 기록했지만 RSI 지표가 더 높은 저점을 기록할 때 강세 다이버전스 조건이 충족되어 매수 신호가 발생합니다.

- 가격이 더 높은 고점을 기록했지만 RSI 지표가 더 낮은 고점을 기록할 때 약세 다이버전스 조건이 충족되어 매도 신호가 발생합니다.

가격과 RSI 지표 간의 다이버전스 현상을 식별함으로써 가격 추세의 전환점을 사전에 포착하여 매매 결정을 내릴 수 있습니다.

전략 장점

이 전략은 주로 다음과 같은 장점이 있습니다.

- 가격과 RSI 지표 간의 다이버전스 현상을 식별하여 가격 추세의 전환점을 사전에 판단하고 거래 기회를 포착할 수 있습니다.

- 지표 분석을 사용하기 때문에 주관적인 감정에 영향을 받지 않습니다.

- 고정된 회고 구간을 사용하여 다이버전스를 식별하므로 잦은 파라미터 조정을 피할 수 있습니다.

- 일봉 RSI 등 추가 조건을 결합하여 오거래 확률을 줄일 수 있습니다.

리스크 및 해결 방법

이 전략에는 다음과 같은 리스크도 존재합니다.

- RSI 지표의 다이버전스가 반드시 즉각적인 가격 반전을 의미하는 것은 아니며 시간 차이가 발생할 수 있어 손절매가 발동될 위험이 있습니다. 해결 방법은 손절매 폭을 적절히 완화하여 가격이 다이버전스 신호를 확인할 충분한 시간을 주는 것입니다.

- 다이버전스 현상이 너무 오래 지속되면 리스크가 증가할 수 있습니다. 해결 방법은 더 장기적인 일봉 또는 주봉 RSI 지표를 필터 조건으로 결합하는 것입니다.

- 다이버전스의 폭이 너무 작으면 추세 전환을 확인하기 어려우므로 회고 구간을 적절히 확대하여 더 명확한 RSI 다이버전스를 탐색해야 합니다.

전략 최적화 방향

이 전략은 다음과 같은 방향으로 최적화할 수 있습니다.

- RSI 파라미터를 최적화하여 최적의 파라미터 조합을 찾습니다.

- MACD, KD 등 다른 기술적 지표를 시도하여 다이버전스 현상을 식별합니다.

- 적절한 횡보장 필터 조건을 추가하여 횡보장에서의 오거래를 줄입니다.

- 더 많은 시간 프레임의 RSI 지표를 결합하여 최적의 조합 신호를 찾습니다.

요약

RSI 다이버전스 매매 전략은 RSI 지표와 가격 간의 다이버전스 현상을 식별하여 가격 추세의 전환점을 판단하고 이를 기반으로 매매 신호를 구축합니다. 이 전략은 간단하고 실용적이며, 파라미터 설정 최적화와 필터 조건 추가를 통해 수익 확률을 더욱 높일 수 있습니다. 전반적으로 RSI 다이버전스 전략은 매우 효과적인 퀀트 매매 전략입니다.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1