Strategi Perdagangan Ayunan Berdasarkan Purata Bergerak Berganda

Gambaran Keseluruhan

Strategi ini merupakan strategi dagangan ayunan (oscillation) berdasarkan dua purata bergerak. Ia menggunakan persilangan purata bergerak pantas dan purata bergerak perlahan sebagai isyarat beli dan jual. Apabila purata bergerak pantas melintasi ke atas purata bergerak perlahan, isyarat beli dijana; apabila purata bergerak pantas melintasi ke bawah purata bergerak perlahan, isyarat jual dijana. Strategi ini sesuai untuk pasaran yang tidak menentu (oscillating market) dan boleh meraih keuntungan daripada pergerakan harga jangka pendek.

Prinsip Strategi

Strategi ini menggunakan RMA dengan panjang 6 sebagai purata bergerak pantas, dan HMA dengan panjang 4 sebagai purata bergerak perlahan. Ia menilai trend harga dan menjana isyarat dagangan berdasarkan persilangan antara garis pantas dan garis perlahan.

Apabila garis pantas melintasi ke atas garis perlahan, ia menunjukkan harga berubah daripada menurun kepada meningkat dalam jangka pendek, yang merupakan masa yang sesuai untuk pertukaran cip (chip switching). Oleh itu, strategi menjana isyarat beli pada ketika ini. Apabila garis pantas melintasi ke bawah garis perlahan, ia menunjukkan harga berubah daripada meningkat kepada menurun dalam jangka pendek, yang juga merupakan masa yang sesuai untuk pertukaran cip, maka strategi menjana isyarat jual.

Selain itu, strategi juga mengesan penilaian trend jangka panjang untuk mengelakkan dagangan melawan arah (counter-trend). Isyarat beli dan jual sebenar hanya akan dijana apabila penilaian trend jangka panjang juga menyokong isyarat tersebut.

Kelebihan Strategi

Strategi ini mempunyai kelebihan berikut:

- Menggunakan persilangan dua purata bergerak untuk mengenal pasti titik pembalikan harga jangka pendek dengan berkesan.

- Panjang garis pantas dan garis perlahan digabungkan secara munasabah, menghasilkan isyarat dagangan yang lebih tepat.

- Menggabungkan penilaian trend jangka panjang dan pendek, dapat menapis kebanyakan isyarat dagangan yang bising (noise).

- Melaksanakan logik ambil untung dan henti rugi (take profit dan stop loss) untuk mengelakkan risiko secara aktif.

- Mudah difahami dan dilaksanakan, sesuai untuk pemula dagangan kuantitatif.

Risiko dan Penyelesaian

Strategi ini juga mempunyai beberapa risiko:

- Strategi dua purata bergerak cenderung menjana banyak keuntungan kecil tetapi satu kerugian besar. Penyelesaiannya adalah dengan menyesuaikan tahap ambil untung dan henti rugi dengan sewajarnya.

- Dalam pasaran yang tidak menentu, isyarat dagangan yang kerap boleh menyebabkan dagangan berlebihan. Penyelesaiannya adalah dengan melonggarkan syarat dagangan untuk mengurangkan urus niaga.

- Parameter strategi mudah dioptimumkan secara berlebihan (overfitting), yang mungkin menyebabkan prestasi lemah dalam dagangan sebenar. Penyelesaiannya adalah dengan melakukan ujian keteguhan (robustness test) parameter.

- Strategi menunjukkan prestasi lemah dalam pasaran yang cenderung (trending). Penyelesaiannya adalah dengan menambah modul pengesanan trend atau menggabungkannya dengan strategi trend.

Hala Tuju Pengoptimuman

Strategi ini boleh dioptimumkan lagi dalam arah berikut:

- Mengemas kini penunjuk purata bergerak dengan menggunakan penapis adaptif seperti Kalman.

- Menambah modul pembelajaran mesin untuk melatih AI mengenal pasti titik beli dan jual.

- Menambah modul pengurusan modal untuk mengautomasikan kawalan risiko.

- Menggabungkan dengan faktor frekuensi tinggi untuk mencari isyarat dagangan yang lebih kuat.

- Arbitraj merentas pasaran (cross-market arbitrage) dengan pelbagai instrumen.

Kesimpulan

Secara keseluruhan, strategi ayunan dua purata bergerak ini adalah strategi dagangan kuantitatif yang tipikal dan praktikal. Ia mempunyai kebolehsuaian yang kuat, dan pemula boleh mempelajari banyak pengetahuan tentang pembangunan strategi daripadanya. Pada masa yang sama, ia juga mempunyai ruang yang besar untuk penambahbaikan dan boleh dioptimumkan dengan lebih banyak teknik kuantitatif untuk mencapai hasil yang lebih baik.

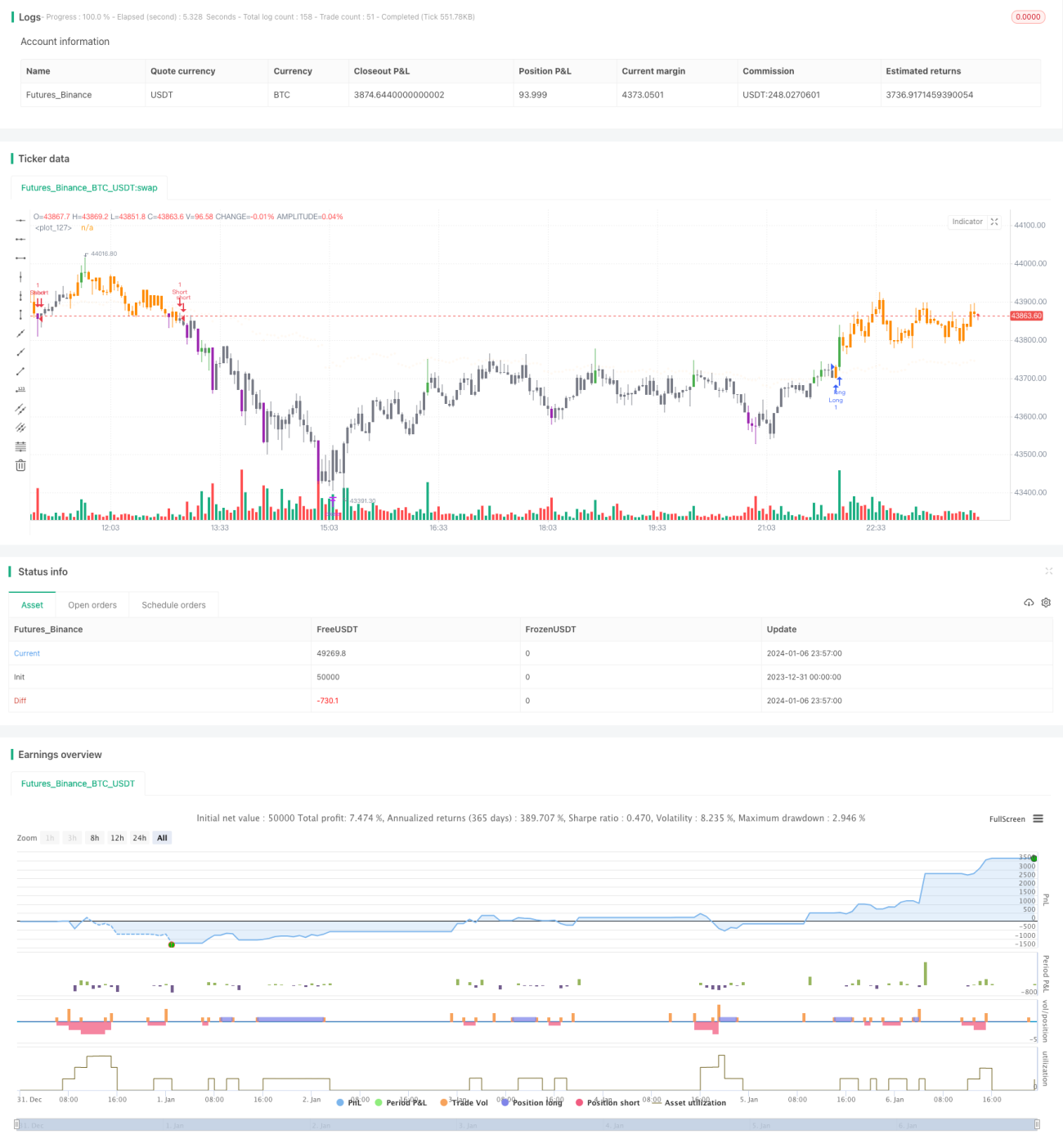

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © dc_analytics

// https://datacryptoanalytics.com/

- 1