Strategi Dagangan Pengasingan Long-Short Indikator RSI

Gambaran Keseluruhan

Strategi ini menggunakan indikator RSI untuk mengenal pasti fenomena perbezaan kenaikan dan penurunan, dan seterusnya membuat keputusan perdagangan. Idea utamanya ialah apabila harga mencapai paras rendah baharu tetapi RSI mencapai paras tinggi baharu, ia membentuk isyarat "perbezaan kenaikan" yang menunjukkan bahawa bahagian bawah telah terbentuk, dan lakukan beli (long). Apabila harga mencapai paras tinggi baharu tetapi RSI mencapai paras rendah baharu, ia membentuk isyarat "perbezaan penurunan" yang menunjukkan bahagian atas telah terbentuk, dan lakukan jual (short).

Prinsip Strategi

Strategi ini terutamanya menggunakan indikator RSI untuk mengenal pasti perbezaan kenaikan dan penurunan antara harga dan RSI. Kaedah khusus adalah seperti berikut:

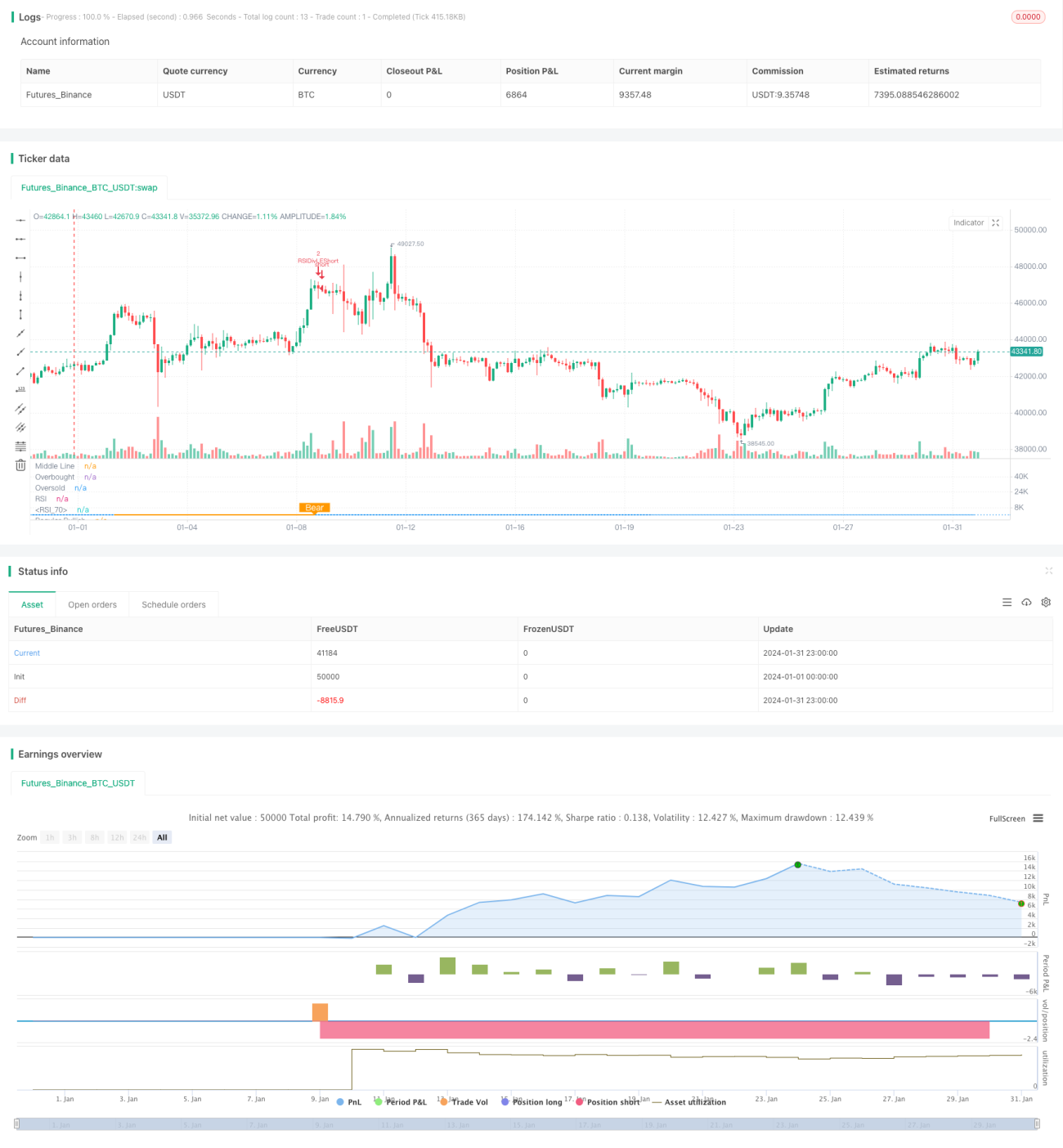

- Gunakan parameter RSI 13 dengan data sumber harga penutup.

- Takrifkan julat surihan ke kiri untuk perbezaan kenaikan sebagai 14 hari, dan julat surihan ke kanan sebagai 2 hari.

- Takrifkan julat surihan ke kiri untuk perbezaan penurunan sebagai 47 hari, dan julat surihan ke kanan sebagai 1 hari.

- Apabila harga mencipta titik rendah yang lebih rendah, tetapi RSI mencipta titik rendah yang lebih tinggi, syarat perbezaan kenaikan dipenuhi, menghasilkan isyarat beli (long).

- Apabila harga mencipta titik tinggi yang lebih tinggi, tetapi RSI mencipta titik tinggi yang lebih rendah, syarat perbezaan penurunan dipenuhi, menghasilkan isyarat jual (short).

Dengan mengenal pasti fenomena perbezaan kenaikan dan penurunan antara harga dan RSI, titik perubahan arah aliran harga dapat dikesan lebih awal, dan seterusnya keputusan perdagangan dibuat.

Kelebihan Strategi

Strategi ini mempunyai kelebihan utama berikut:

- Mengenal pasti fenomena perbezaan kenaikan dan penurunan antara harga dan RSI membolehkan penentuan titik perubahan arah aliran harga lebih awal, merebut peluang perdagangan.

- Oleh kerana ia menggunakan analisis indikator, ia tidak dipengaruhi oleh emosi subjektif.

- Menggunakan julat surihan tetap untuk mengenal pasti perbezaan, mengelakkan pelarasan parameter yang kerap.

- Menggabungkan syarat tambahan seperti RSI harian dapat mengurangkan kebarangkalian perdagangan yang salah.

Risiko dan Cara Penyelesaian

Strategi ini juga mempunyai risiko tertentu:

-

Perbezaan indikator RSI tidak semestinya meramalkan pembalikan harga serta-merta; mungkin terdapat jurang masa, yang boleh menyebabkan risiko henti rugi dipicu. Penyelesaiannya adalah dengan melonggarkan sedikit amplitud henti rugi untuk memberi masa yang mencukupi bagi harga mengesahkan isyarat perbezaan.

-

Fenomena perbezaan yang berlarutan terlalu lama juga boleh meningkatkan risiko. Penyelesaiannya adalah dengan menggabungkan indikator RSI jangka panjang seperti harian atau mingguan sebagai penapis.

-

Amplitud perbezaan yang terlalu kecil tidak dapat mengesahkan perubahan arah aliran, dan julat surihan perlu dibesarkan sedikit untuk mencari perbezaan RSI yang lebih jelas.

Arah Pengoptimuman Strategi

Strategi ini juga boleh dioptimumkan dari beberapa arah berikut:

- Mengoptimumkan parameter RSI untuk mendapatkan kombinasi parameter terbaik.

- Mencuba indikator teknikal lain seperti MACD, KD untuk mengenal pasti fenomena perbezaan kenaikan dan penurunan.

- Menambah syarat penapisan semasa fasa penyebaran yang sesuai untuk mengelakkan perdagangan yang salah semasa fasa penyebaran.

- Menggabungkan indikator RSI dari lebih banyak tempoh masa untuk mencari isyarat gabungan terbaik.

Ringkasan

Strategi perdagangan perbezaan kenaikan dan penurunan RSI mengenal pasti fenomena perbezaan antara RSI dan harga untuk menentukan titik perubahan arah aliran harga, dan seterusnya menghasilkan isyarat perdagangan. Strategi ini mudah dan praktikal. Dengan mengoptimumkan tetapan parameter dan menambah syarat penapisan, kebarangkalian keuntungan dapat ditingkatkan. Secara keseluruhan, strategi perbezaan kenaikan dan penurunan RSI adalah strategi perdagangan kuantitatif yang sangat berkesan.

- 1