Estratégia de Trading Multitimeframe Baseada em RSI e Médias Móveis

Visão Geral

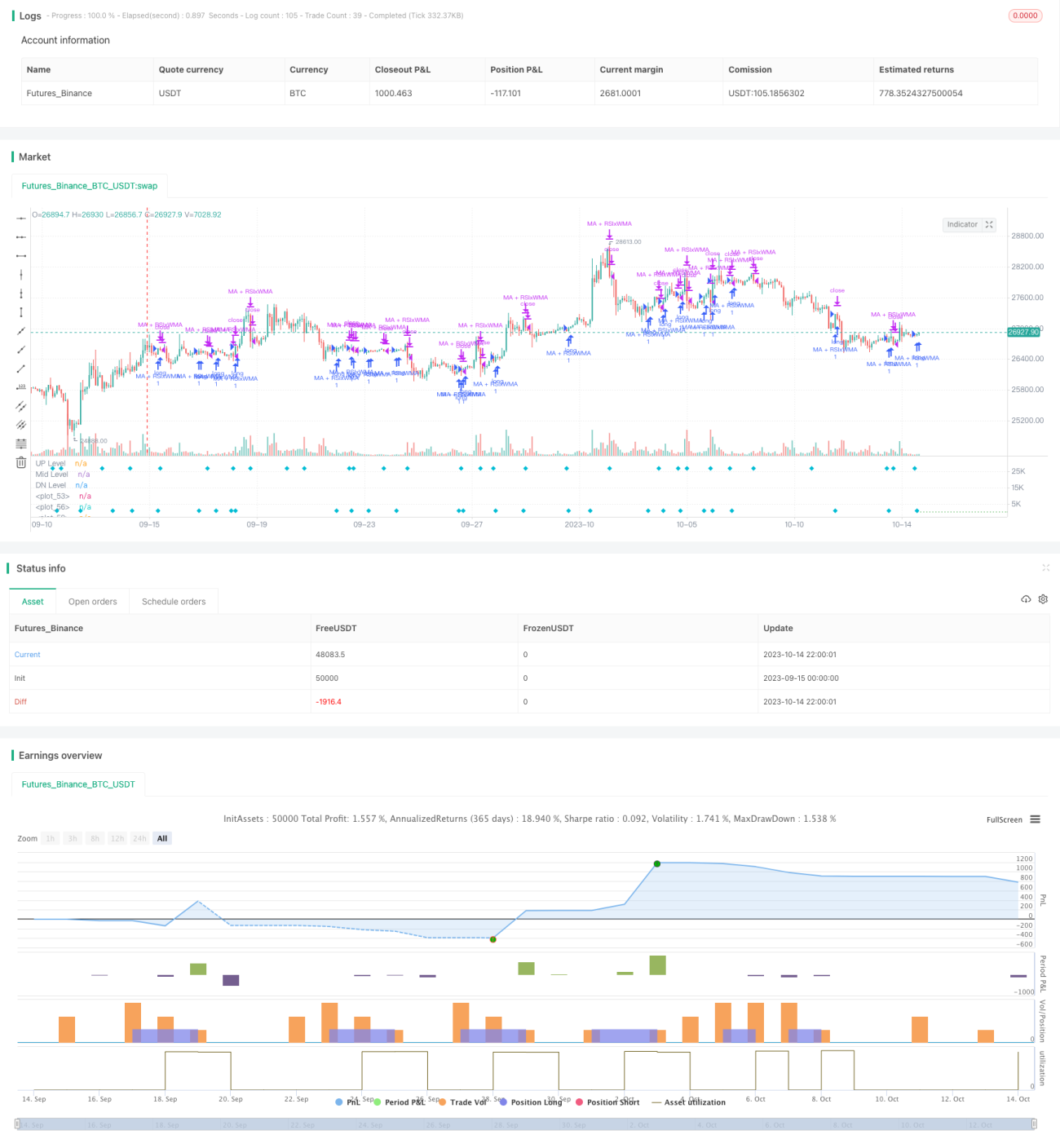

A ideia central desta estratégia é utilizar simultaneamente o Índice de Força Relativa (RSI) e médias móveis de diferentes períodos para identificar pontos de reversão de tendência, capturando tendências de médio/longo prazo enquanto realiza negociações de curto prazo. A estratégia combina múltiplos sinais de negociação para aumentar a taxa de sucesso.

Princípio da Estratégia

- Calcula o indicador RSI, bem como a EMA rápida e a WMA lenta (médias móveis).

- Quando a linha do indicador RSI rompe a média móvel WMA, gera um sinal de compra/venda.

- Quando a EMA rápida rompe a WMA lenta, gera um sinal de compra/venda.

- Quando o RSI e a EMA rompem a WMA simultaneamente, gera um sinal forte de compra/venda.

- Simultaneamente, quando o preço rompe a média móvel auxiliar, pode reforçar o sinal principal.

- Define condições de stop loss e take profit.

A estratégia combina múltiplos sinais de rompimento de indicadores técnicos, utilizando médias móveis com parâmetros diferentes para identificar tendências de diferentes períodos, aumentando assim a confiabilidade da estratégia. O RSI avalia condições de sobrecompra/sobrevenda, a EMA rápida indica tendência de curto prazo, a WMA lenta indica tendência de médio prazo, e o rompimento do preço em relação à média auxiliar confirma a tendência. A combinação de múltiplos sinais melhora a eficácia da estratégia.

Análise de Vantagens

- Utiliza as características de reversão do RSI para capturar oportunidades de reversão em zonas de sobrecompra/sobrevenda.

- As médias móveis auxiliares atuam como filtros de tendência, evitando falsos rompimentos.

- Combinação de múltiplos períodos de tempo, permitindo acompanhar tendências de longo prazo e capturar oportunidades de curto prazo.

- Combinação de múltiplos sinais de indicadores pode aumentar a taxa de sucesso das negociações.

- Definição de estratégias de stop loss e take profit permite controlar o risco ativamente.

Análise de Riscos

- O RSI é propenso a gerar sinais falsos, necessitando de filtragem por médias móveis auxiliares.

- Reversões dentro de uma tendência maior podem gerar sinais de negociação contrários, exigindo cautela.

- É necessário otimizar parâmetros como o período do RSI e os períodos das médias móveis.

- O ponto de stop loss deve ser definido com cuidado para evitar ser "encurralado".

Os riscos podem ser mitigados através de otimização de parâmetros, estratégias rigorosas de stop loss e consideração da tendência de longo prazo.

Direções de Otimização

- Otimizar os parâmetros do RSI para encontrar o período ideal.

- Testar diferentes combinações de tipos de médias móveis.

- Adicionar indicadores de volatilidade como o ATR para ajustar dinamicamente stop loss e take profit.

- Incluir um módulo de gerenciamento de volume de negociação.

- Utilizar técnicas de aprendizado de máquina para otimização de parâmetros e avaliação da qualidade dos sinais.

Resumo

Esta estratégia integra conceitos de acompanhamento de tendência e reversão de extremos, adicionando análise em múltiplos períodos e uso combinado de vários indicadores, com o objetivo de aumentar a taxa de acerto das negociações. O ponto chave é controlar o risco, otimizar os parâmetros e considerar adequadamente o impacto da tendência de longo prazo nas negociações. No geral, esta estratégia possui forte praticidade e adaptabilidade. No futuro, técnicas mais avançadas podem ser empregadas para aprimorar ainda mais a qualidade da estratégia.

- 1