Estratégia de Negociação de Separação Longo/Curto do Indicador RSI

Visão Geral

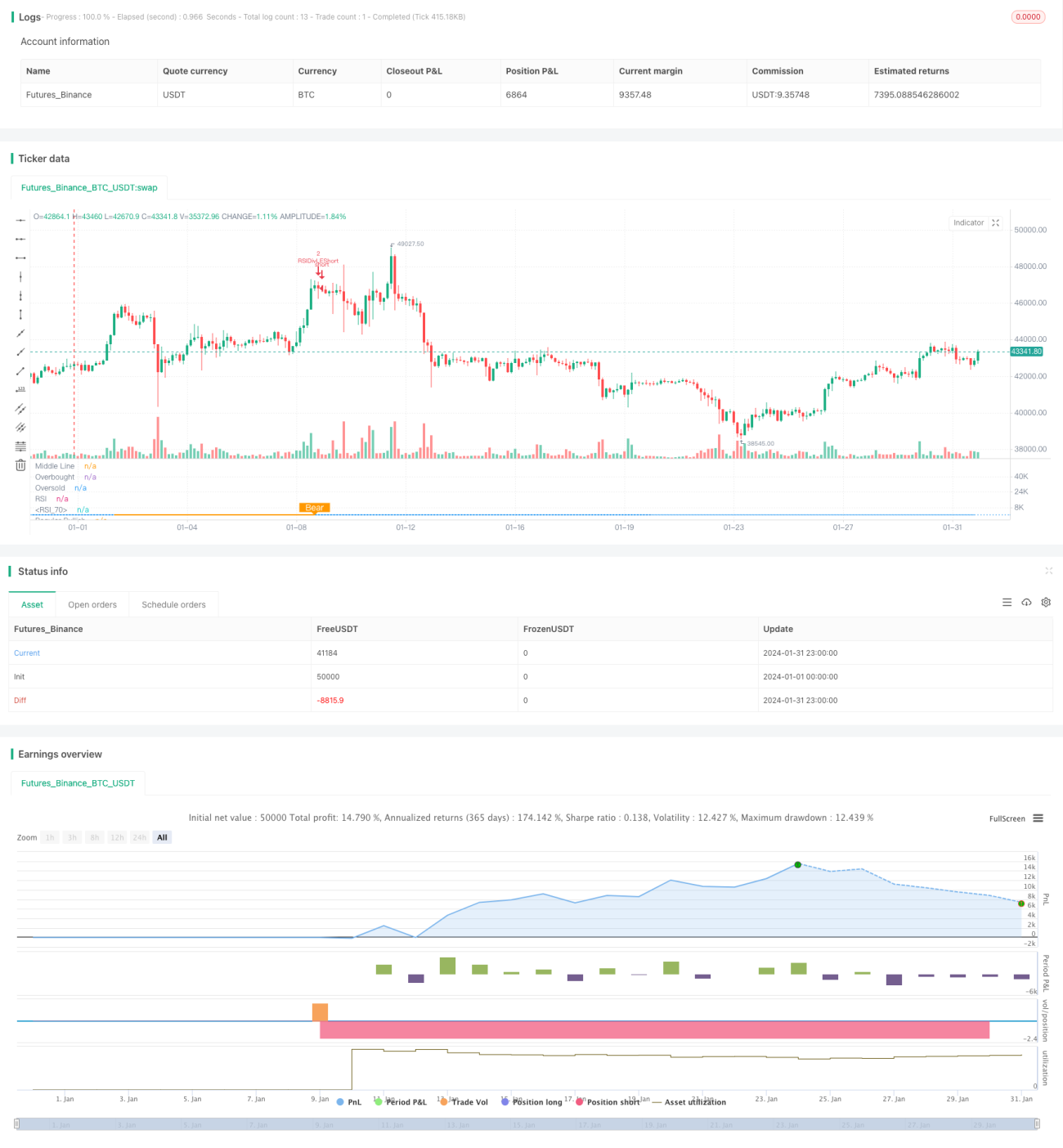

Esta estratégia identifica fenômenos de divergência de alta e baixa usando o indicador RSI, tomando decisões de negociação com base nisso. A ideia central é: quando o preço atinge uma nova mínima, mas o RSI atinge uma nova máxima (mínima mais alta), forma-se um sinal de "divergência de alta", indicando que um fundo foi formado — operar comprado. Quando o preço atinge uma nova máxima, mas o RSI atinge uma nova mínima (máxima mais baixa), forma-se um sinal de "divergência de baixa", indicando que um topo foi formado — operar vendido.

Princípio da Estratégia

A estratégia utiliza principalmente o indicador RSI para identificar divergências entre preço e RSI. O método específico é o seguinte:

- Parâmetro do RSI: período 13, fonte de dados: preço de fechamento.

- O período de retrospectiva para divergência de alta é de 14 dias para a esquerda e 2 dias para a direita.

- O período de retrospectiva para divergência de baixa é de 47 dias para a esquerda e 1 dia para a direita.

- Quando o preço forma uma mínima mais baixa, mas o RSI forma uma mínima mais alta, a condição de divergência de alta é satisfeita, gerando um sinal de compra.

- Quando o preço forma uma máxima mais alta, mas o RSI forma uma máxima mais baixa, a condição de divergência de baixa é satisfeita, gerando um sinal de venda.

Ao identificar divergências entre preço e RSI, é possível capturar antecipadamente pontos de reversão da tendência de preço, tomando decisões de negociação com base nisso.

Vantagens da Estratégia

As principais vantagens desta estratégia são:

- Identificar divergências entre preço e RSI permite antecipar pontos de reversão da tendência, aproveitando oportunidades de negociação.

- Por utilizar análise de indicadores, não é influenciada por emoções subjetivas.

- Utiliza intervalos de retrospectiva fixos para identificar divergências, evitando ajustes frequentes de parâmetros.

- A combinação com condições adicionais, como o RSI diário, reduz a probabilidade de negociações falsas.

Riscos e Soluções

A estratégia também apresenta alguns riscos:

- A divergência do RSI não indica necessariamente reversão imediata do preço; pode haver diferença temporal, o que pode acionar o stop loss. Solução: ajustar adequadamente a amplitude do stop loss, dando tempo suficiente para o preço confirmar o sinal de divergência.

- Divergências que persistem por muito tempo aumentam o risco. Solução: combinar indicadores de RSI de prazos mais longos (diário ou semanal) como filtro adicional.

- Divergências muito pequenas não conseguem confirmar a reversão da tendência, sendo necessário ampliar o intervalo de retrospectiva para buscar divergências mais evidentes.

Direções de Otimização

A estratégia pode ser otimizada nas seguintes direções:

- Otimizar os parâmetros do RSI para encontrar a melhor combinação.

- Experimentar outros indicadores técnicos, como MACD, KDJ, etc., para identificar divergências.

- Adicionar filtros adequados para períodos de consolidação, reduzindo negociações falsas nesses períodos.

- Combinar RSI de múltiplos períodos para encontrar os melhores sinais compostos.

Resumo

A estratégia de divergência de alta e baixa do RSI identifica divergências entre o RSI e o preço para julgar pontos de reversão da tendência, gerando sinais de negociação. A estratégia é simples e prática, e pode aumentar a probabilidade de lucro por meio da otimização de parâmetros e da adição de filtros. Em suma, a estratégia de divergência do RSI é uma estratégia de negociação quantitativa bastante eficaz.

- 1