Стратегия следования за трендом с двойными скользящими средними и полосами Боллинджера

Обзор

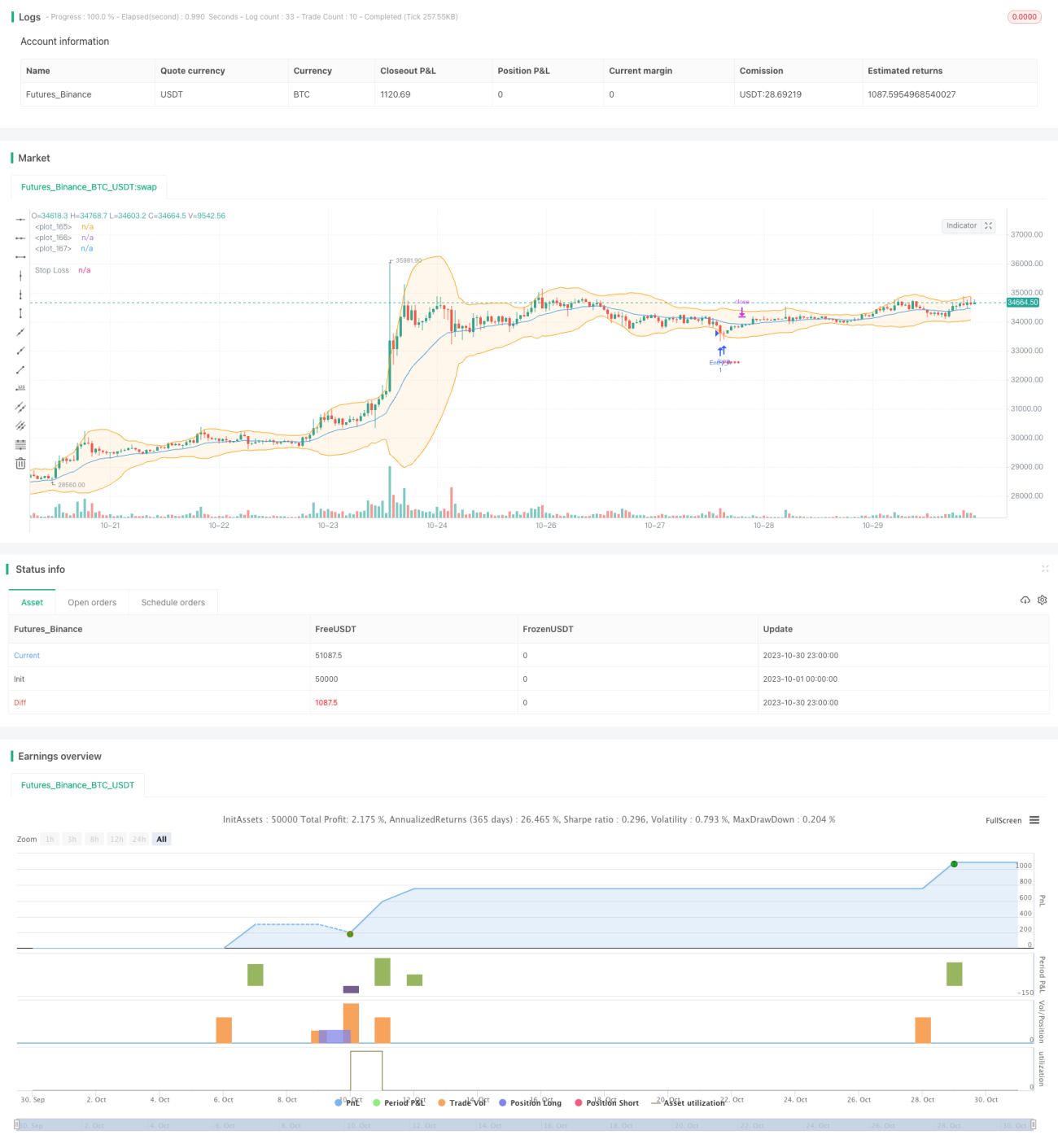

Данная стратегия основана на двойных скользящих средних полос Боллинджера для принятия решений о следовании за трендом. Она использует схождение и расхождение верхней и нижней границ полос Боллинджера для определения изменения тренда, покупает вблизи нижней границы и продает вблизи верхней, реализуя принцип "покупай дешево, продавай дорого" и фиксируя прибыль.

Принцип стратегии

Стратегия одновременно использует две версии полос Боллинджера: простые полосы Боллинджера и усиленные полосы Боллинджера.

В простых полосах Боллинджера средняя линия рассчитывается как SMA цены закрытия, в усиленных — как EMA цены закрытия.

Верхняя и нижняя границы вычисляются как средняя линия ± N стандартных отклонений.

Стратегия определяет тренд на основе расстояния (spread) между верхней и нижней границами: когда spread меньше заданного порога, это сигнализирует о входе в трендовый диапазон, и можно совершать сделки по следованию за трендом.

Конкретно: когда цена приближается к нижней границе, открывается длинная позиция; когда приближается к верхней границе — позиция закрывается. Стоп-лосс устанавливается в виде фиксированного процента, также опционально можно использовать трейлинг-стоп.

Целевая прибыль зависит от выбора закрытия позиции вблизи средней линии или верхней границы.

Также стратегия может быть настроена на продажу только при гарантированной прибыли, чтобы избежать убытков.

Преимущества анализа

Стратегия обладает следующими преимуществами:

-

Объединение двойных полос Боллинджера повышает эффективность принятия решений

Использование простых и усиленных полос Боллинджера позволяет сравнить их эффективность и выбрать более подходящую версию, повышая качество решений.

-

Определение силы тренда по ширине канала полос Боллинджера

Когда канал сужается, это указывает на вход в трендовое движение, и вероятность успеха при следовании за трендом возрастает.

-

Гибкие методы фиксации прибыли и стоп-лосса

Используется фиксированный процентный стоп-лосс для контроля убытков по каждой сделке. Опционально можно фиксировать прибыль вблизи средней линии или верхней границы, а также применять трейлинг-стоп для сохранения большей прибыли.

-

Защитный механизм от убытков

Продажа только при гарантированной прибыли предотвращает увеличение убытков.

Анализ рисков

Стратегия также содержит следующие риски:

-

Риск просадки

Следование за трендом само по себе несет риск просадки, требуется психологическая устойчивость к серии убытков.

-

Риск бокового рынка

Когда канал полос Боллинджера расширен, это может указывать на боковое движение, в таких условиях стратегия работает плохо; необходимо приостановить торговлю до формирования нового тренда.

-

Риск срабатывания стоп-лосса

Фиксированный процентный стоп-лосс может быть слишком агрессивным; рекомендуется перейти на более мягкий метод, например, стоп на основе ATR.

Направления оптимизации

Стратегию можно оптимизировать по следующим направлениям:

-

Оптимизация параметров полос Боллинджера

Тестировать различные параметры скользящих средних и множители стандартного отклонения для нахождения наилучших комбинаций для разных рынков.

-

Добавление фильтров на основе других индикаторов

На сигналы полос Боллинджера можно накладывать фильтры, например, MACD, KDJ, чтобы уменьшить количество сделок на боковом рынке.

-

Оптимизация тактик фиксации прибыли и стоп-лосса

Тестировать различные виды трейлинг-стопа или оптимизировать уровни стоп-лосса на основе волатильности или ATR.

-

Оптимизация управления капиталом

Оптимизировать размер позиции в каждой сделке и тестировать различные стратегии добавления позиций.

Заключение

Данная стратегия объединяет преимущества двойных полос Боллинджера, определяет силу тренда по ширине канала и осуществляет следование за трендом с покупкой на спадах и продажей на пиках. При этом используются научные механизмы стоп-лосса для контроля рисков. Стратегия может быть дополнительно стабилизирована путем оптимизации параметров и добавления фильтров на основе других индикаторов.

- 1