Торговая стратегия разделения длинных и коротких позиций на основе индикатора RSI

Обзор

Данная стратегия использует индикатор RSI для выявления явлений бычьей и медвежьей дивергенции, на основании чего принимаются торговые решения. Её основная идея заключается в том, что когда цена обновляет минимум, а RSI обновляет максимум, формируется сигнал «бычьей дивергенции», указывающий на формирование дна, и открывается длинная позиция; когда цена обновляет максимум, а RSI обновляет минимум, формируется сигнал «медвежьей дивергенции», указывающий на формирование вершины, и открывается короткая позиция.

Принцип стратегии

Стратегия в основном использует индикатор RSI для выявления дивергенции между ценой и RSI. Конкретный метод следующий:

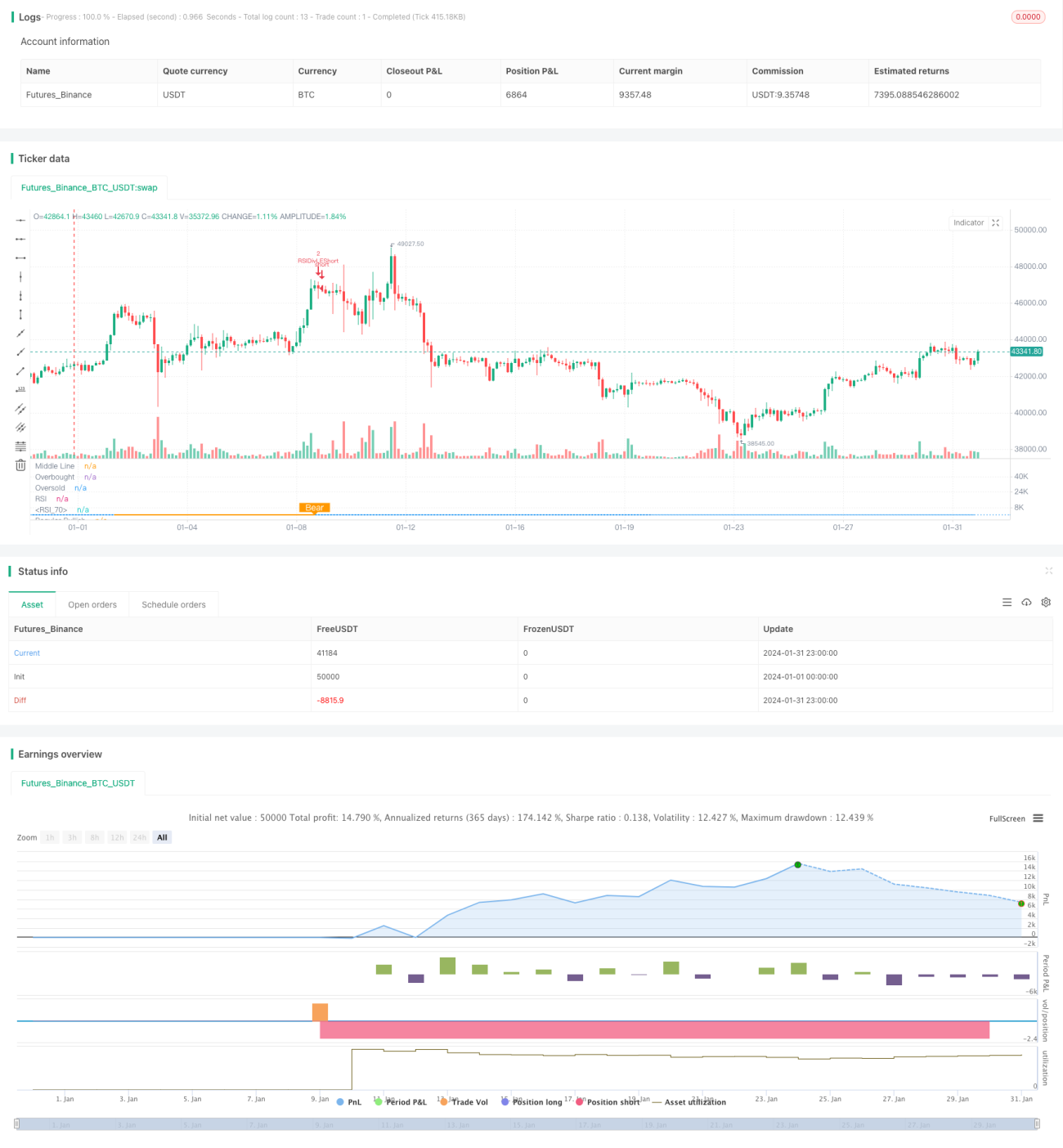

- Параметр RSI = 13, источник данных – цена закрытия.

- Для бычьей дивергенции период ретроспективного анализа влево составляет 14 дней, вправо – 2 дня.

- Для медвежьей дивергенции период ретроспективного анализа влево составляет 47 дней, вправо – 1 день.

- Когда цена образует более низкий минимум, а RSI – более высокий минимум, выполняется условие бычьей дивергенции, генерируется сигнал на покупку.

- Когда цена образует более высокий максимум, а RSI – более низкий максимум, выполняется условие медвежьей дивергенции, генерируется сигнал на продажу.

Выявляя дивергенцию между ценой и RSI, стратегия позволяет заранее улавливать точки разворота ценового тренда и принимать на их основе торговые решения.

Преимущества стратегии

Основные преимущества данной стратегии:

- Выявление дивергенции между ценой и RSI позволяет заранее определять точки разворота ценового тренда и использовать торговые возможности.

- Поскольку используется анализ индикаторов, он не подвержен субъективным эмоциям.

- Использование фиксированных ретроспективных интервалов для идентификации дивергенции позволяет избежать частой настройки параметров.

- Дополнительные условия, такие как дневной RSI, снижают вероятность ошибочных сделок.

Риски и методы их устранения

Стратегия также сопряжена с определёнными рисками:

-

Дивергенция RSI не обязательно означает немедленный разворот цены, может наблюдаться временной лаг, что приводит к риску срабатывания стоп-лосса. Решение: соответствующим образом расширить диапазон стоп-лосса, давая цене достаточно времени для подтверждения сигнала дивергенции.

-

Длительное сохранение дивергенции также увеличивает риск. Решение: использовать в качестве фильтра более долгосрочные дневные или недельные индикаторы RSI.

-

Слишком малая амплитуда дивергенции не позволяет подтвердить разворот тренда. Необходимо соответствующим образом расширить ретроспективный интервал для поиска более выраженной дивергенции RSI.

Направления оптимизации стратегии

Стратегию можно оптимизировать по следующим направлениям:

- Оптимизация параметров RSI для поиска наилучшего сочетания.

- Использование других технических индикаторов, таких как MACD, KD, для выявления дивергенции.

- Добавление фильтров для периодов флэта, чтобы снизить количество ошибочных сделок во время бокового движения.

- Комбинирование RSI на различных таймфреймах для поиска наилучшего комбинированного сигнала.

Заключение

Стратегия торговли на дивергенции RSI выявляет дивергенцию между индикатором RSI и ценой, определяет точки разворота ценового тренда и на этой основе формирует торговые сигналы. Стратегия проста и практична. Путём оптимизации параметров и добавления фильтров можно дополнительно повысить вероятность получения прибыли. В целом, стратегия дивергенции RSI является весьма эффективной стратегией количественной торговли.

- 1