Система принятия торговых решений Turtle

Обзор

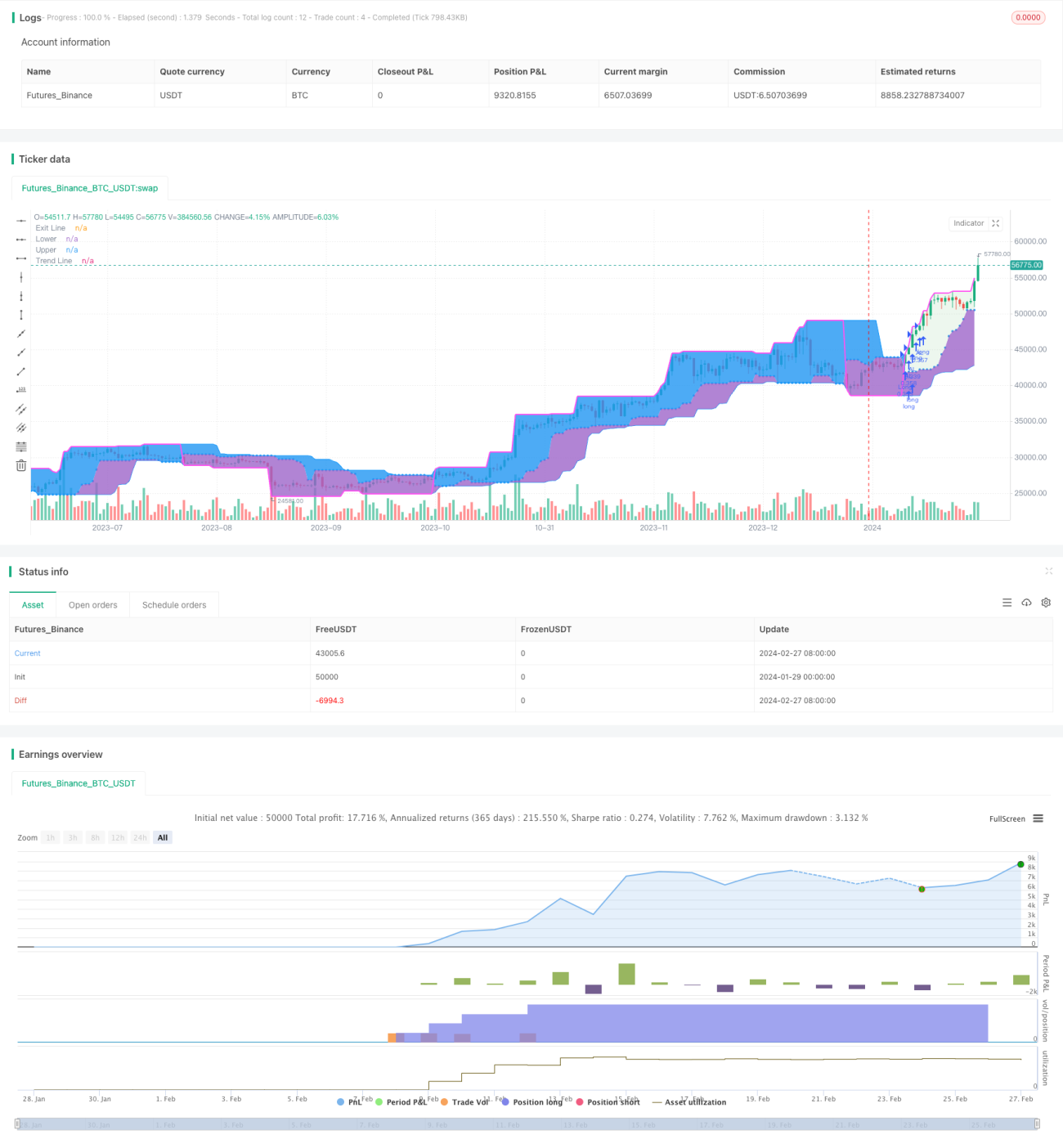

Система принятия решений о трейдинге на берегу моря - это торговая стратегия, основанная на теории прорыва. Она генерирует торговые сигналы, позволяющие идентифицировать потенциальные тенденции, путем создания движущихся средних цен на наивысшие и наименьшие цены торговых сортов.

Стратегический принцип

Основные стратегические сигналы в системе принятия решений о трейдинге в Океане формируются путем сравнения величины отношений цены с максимальной ценой цикла N1 и минимальной ценой цикла N2. При пересечении максимальной цены цикла N1 на верхнем уровне генерируется сигнал покупки; при пересечении минимальной цены цикла N2 на нижнем уровне генерируется сигнал продажи.

После открытия позиции, будет сравнивать в реальном времени цены и величины отношения к цене остановки, генерируя мобильный сигнал остановки. В то же время, также будет сравнивать отношения цены и линии наращивания, генерируя сигнал наращивания. Стоп-цены и линии наращивания связаны с ATR.

Каждый раз, когда открывается позиция, она рассчитывается в единицах удержания, чтобы избежать влияния одиночных потерь на общий капитал путем снятия определенной доли первоначального капитала.

Анализ преимуществ

Система принятия решений по сделкам на пляже имеет следующие преимущества:

-

Поймать потенциальные тенденции: определить направление потенциальных тенденций, сравнив цены с их отношениями с циклическими максимумами и минимумами.

-

Управление рисками: использование управления капиталом и потери для контроля риска потерь как в отдельных, так и в целом.

-

Управление накладом: надлежащее накладывание накладов позволяет получить дополнительную прибыль в тренде.

-

Целостность: в сочетании с управлением капиталом, управлением убытками и управлением налогами, система принятия решений становится более полной.

-

Простые и ясные: правила создания сигнала простые, простые, понятные и легко проверяемые.

Анализ рисков

Некоторые риски, связанные с принятием решений в системе торговли шелкопрядами:

-

Риск ложного прорыва: цены могут быть ложными, превышая максимальные или минимальные цены, что приводит к ошибочным сигналам. Можно соответствующим образом отфильтровать некоторые ложные прорывы, регулируя параметры.

-

Риск обратного тренда: существует риск того, что ценовой поворот после нажима может привести к увеличению убытков. Следует ограничить количество нажимов и своевременно прекратить убытки.

-

Параметры оптимизации риска: различные параметры рынка могут быть настроены по-разному. Параметры оптимизации должны быть разделены на рынки для снижения риска.

Направление оптимизации

Система принятия решений по торговле шелковыми костями может быть оптимизирована в следующих аспектах:

-

Добавление фильтров: обнаружение силы ценовых прорывов, отфильтрование ложных прорывов.

-

Оптимизация стратегии остановки убытков: как разумно отслеживать остановки и находить баланс между защитой прибыли и уменьшением ненужных убытков.

-

Оптимизация параметров сегмента: комбинация параметров для оптимизации различных сортовых характеристик.

-

Увеличение машинного обучения: алгоритмы машинного обучения помогают определить направление тенденций.

Подвести итог

Система принятия решений о торговле на пляже определяет направление потенциальной тенденции путем сравнения цены с наивысшей и самой низкой ценой в течение заданного периода и в сочетании с модулем управления рисками строит всю систему принятия решений. Она обладает более сильной способностью отслеживать тенденции, но также имеет определенные проблемы с оптимизацией рисков ложных прорывов и параметров.

/*backtest

start: 2024-01-29 00:00:00

end: 2024-02-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © 李和邪

// 本脚本所有内容只适用于交流学习,不构成投资建议,所有后果自行承担。

//@version=5- 1