Thương mại đường cong vốn chủ sở hữu ví dụ về kích thước vị trí

Tác giả:ChaoZhang, Ngày: 2022-05-13 22:25:44Tags:CMOSMA

Mục đích của việc quản lý đường cong cổ phiếu là giảm thiểu rủi ro trong giao dịch khi đường cong cổ phiếu đang trong xu hướng giảm. Chiến lược này có hai chế độ để xác định xu hướng giảm của đường cong cổ phiếu: Bằng cách tạo ra hai trung bình động đơn giản của đường cong cổ phiếu của danh mục đầu tư - một ngắn hạn và một dài hạn - và hoạt động trên các đường băng của chúng. Nếu SMA nhanh nằm dưới SMA chậm, xu hướng giảm cổ phiếu được phát hiện (smafastequity < smaslowequity). Phương pháp thứ hai là bằng cách sử dụng các đường chéo của vốn chủ sở hữu với SMA dài hạn (tài sản < smasloweequity).

Khi Trading with the Equity Curve" được kích hoạt, kích thước vị trí sẽ được giảm một tỷ lệ phần trăm nếu vốn

backtest

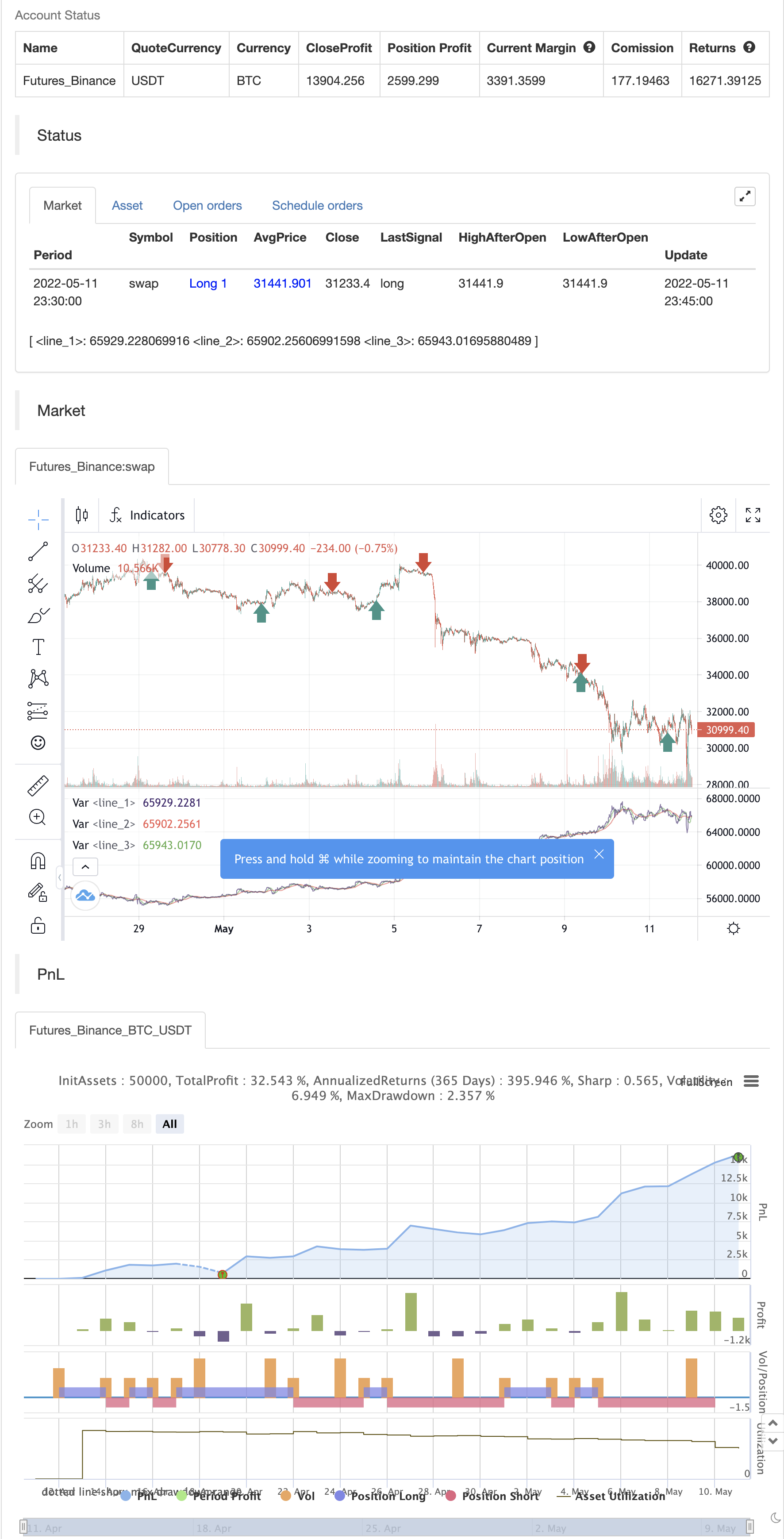

/*backtest

start: 2022-04-12 00:00:00

end: 2022-05-11 23:59:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © shardison

//@version=5

//EXPLANATION

//"Trading the equity curve" as a risk management method is the

//process of acting on trade signals depending on whether a system’s performance

//is indicating the strategy is in a profitable or losing phase.

//The point of managing equity curve is to minimize risk in trading when the equity curve is in a downtrend.

//This strategy has two modes to determine the equity curve downtrend:

//By creating two simple moving averages of a portfolio's equity curve - a short-term

//and a longer-term one - and acting on their crossings. If the fast SMA is below

//the slow SMA, equity downtrend is detected (smafastequity < smaslowequity).

//The second method is by using the crossings of equity itself with the longer-period SMA (equity < smasloweequity).

//When "Reduce size by %" is active, the position size will be reduced by a specified percentage

//if the equity is "under water" according to a selected rule. If you're a risk seeker, select "Increase size by %"

//- for some robust systems, it could help overcome their small drawdowns quicker.

//strategy("Use Trading the Equity Curve Postion Sizing", shorttitle="TEC", default_qty_type = strategy.percent_of_equity, default_qty_value = 10, initial_capital = 100000)

//TRADING THE EQUITY CURVE INPUTS

useTEC = input.bool(true, title="Use Trading the Equity Curve Position Sizing")

defulttraderule = useTEC ? false: true

initialsize = input.float(defval=10.0, title="Initial % Equity")

slowequitylength = input.int(25, title="Slow SMA Period")

fastequitylength = input.int(9, title="Fast SMA Period")

seedequity = 100000 * .10

if strategy.equity == 0

seedequity

else

strategy.equity

slowequityseed = strategy.equity > seedequity ? strategy.equity : seedequity

fastequityseed = strategy.equity > seedequity ? strategy.equity : seedequity

smaslowequity = ta.sma(slowequityseed, slowequitylength)

smafastequity = ta.sma(fastequityseed, fastequitylength)

equitycalc = input.bool(true, title="Use Fast/Slow Avg", tooltip="Fast Equity Avg is below Slow---otherwise if unchecked uses Slow Equity Avg below Equity")

sizeadjstring = input.string("Reduce size by (%)", title="Position Size Adjustment", options=["Reduce size by (%)","Increase size by (%)"])

sizeadjint = input.int(50, title="Increase/Decrease % Equity by:")

equitydowntrendavgs = smafastequity < smaslowequity

slowequitylessequity = strategy.equity < smaslowequity

equitymethod = equitycalc ? equitydowntrendavgs : slowequitylessequity

if sizeadjstring == ("Reduce size by (%)")

sizeadjdown = initialsize * (1 - (sizeadjint/100))

else

sizeadjup = initialsize * (1 + (sizeadjint/100))

c = close

qty = 100000 * (initialsize / 100) / c

if useTEC and equitymethod

if sizeadjstring == "Reduce size by (%)"

qty := (strategy.equity * (initialsize / 100) * (1 - (sizeadjint/100))) / c

else

qty := (strategy.equity * (initialsize / 100) * (1 + (sizeadjint/100))) / c

//EXAMPLE TRADING STRATEGY INPUTS

CMO_Length = input.int(defval=9, minval=1, title='Chande Momentum Length')

CMO_Signal = input.int(defval=10, minval=1, title='Chande Momentum Signal')

chandeMO = ta.cmo(close, CMO_Length)

cmosignal = ta.sma(chandeMO, CMO_Signal)

SuperTrend_atrPeriod = input.int(10, "SuperTrend ATR Length")

SuperTrend_Factor = input.float(3.0, "SuperTrend Factor", step = 0.01)

Momentum_Length = input.int(12, "Momentum Length")

price = close

mom0 = ta.mom(price, Momentum_Length)

mom1 = ta.mom( mom0, 1)

[supertrend, direction] = ta.supertrend(SuperTrend_Factor, SuperTrend_atrPeriod)

stupind = (direction < 0 ? supertrend : na)

stdownind = (direction < 0? na : supertrend)

//TRADING CONDITIONS

longConditiondefault = ta.crossover(chandeMO, cmosignal) and (mom0 > 0 and mom1 > 0 and close > stupind) and defulttraderule

if (longConditiondefault)

strategy.entry("DefLong", strategy.long)

shortConditiondefault = ta.crossunder(chandeMO, cmosignal) and (mom0 < 0 and mom1 < 0 and close < stdownind) and defulttraderule

if (shortConditiondefault)

strategy.entry("DefShort", strategy.short)

longCondition = ta.crossover(chandeMO, cmosignal) and (mom0 > 0 and mom1 > 0 and close > stupind) and useTEC

if (longCondition)

strategy.entry("AdjLong", strategy.long)

shortCondition = ta.crossunder(chandeMO, cmosignal) and (mom0 < 0 and mom1 < 0 and close < stdownind) and useTEC

if (shortCondition)

strategy.entry("AdjShort", strategy.short)

plot(strategy.equity)

plot(smaslowequity, color=color.new(color.red, 0))

plot(smafastequity, color=color.new(color.green, 0))

- NMVOB-S

- Bollinger Bands Chiến lược dao động stochastic

- Điểm số Z với tín hiệu

- TMA Overlay

- Chiến lược Bollinger Bands Standard Deviation Breakout

- Hurst Các đường biên giới trong tương lai của chiến lược phân định

- Nhóm nhạc Mobo

- Chỉ số Động lực nén

- Nik Stoch

- Chiến lược thúc đẩy khung thời gian kép

- CCI MTF Ob+Os

- MACD thông minh hơn

- Chiến lược của OCC R5.1

- Chào mừng bạn đến chợ gấu.

- Sidboss

- Điểm trục cao thấp nhiều khung thời gian

- Phantom Trends theo dõi cơ sở dữ liệu chiến lược

- Phantom Trends theo dõi các cơ sở kinh doanh chiến lược

- Chiến lược theo dõi xu hướng ma

- Rainbow Oscillator

- KLineChart Demo

- Chiến lược siêu xu hướng Villa Dynamic Pivot

- Crodl's Supertrend

- RSI của zdmre

- FTL - Range Filter X2 + EMA + UO

- BRAHMASTRA

- Nhóm nhạc Mobo

- SAR + 3SMMA với SL & TP

- SSS

- Mô hình cảnh báo phóng mặt trăng [Dấu hiệu]