Chiến lược giao dịch đa khung thời gian dựa trên RSI và đường trung bình động

Tổng quan

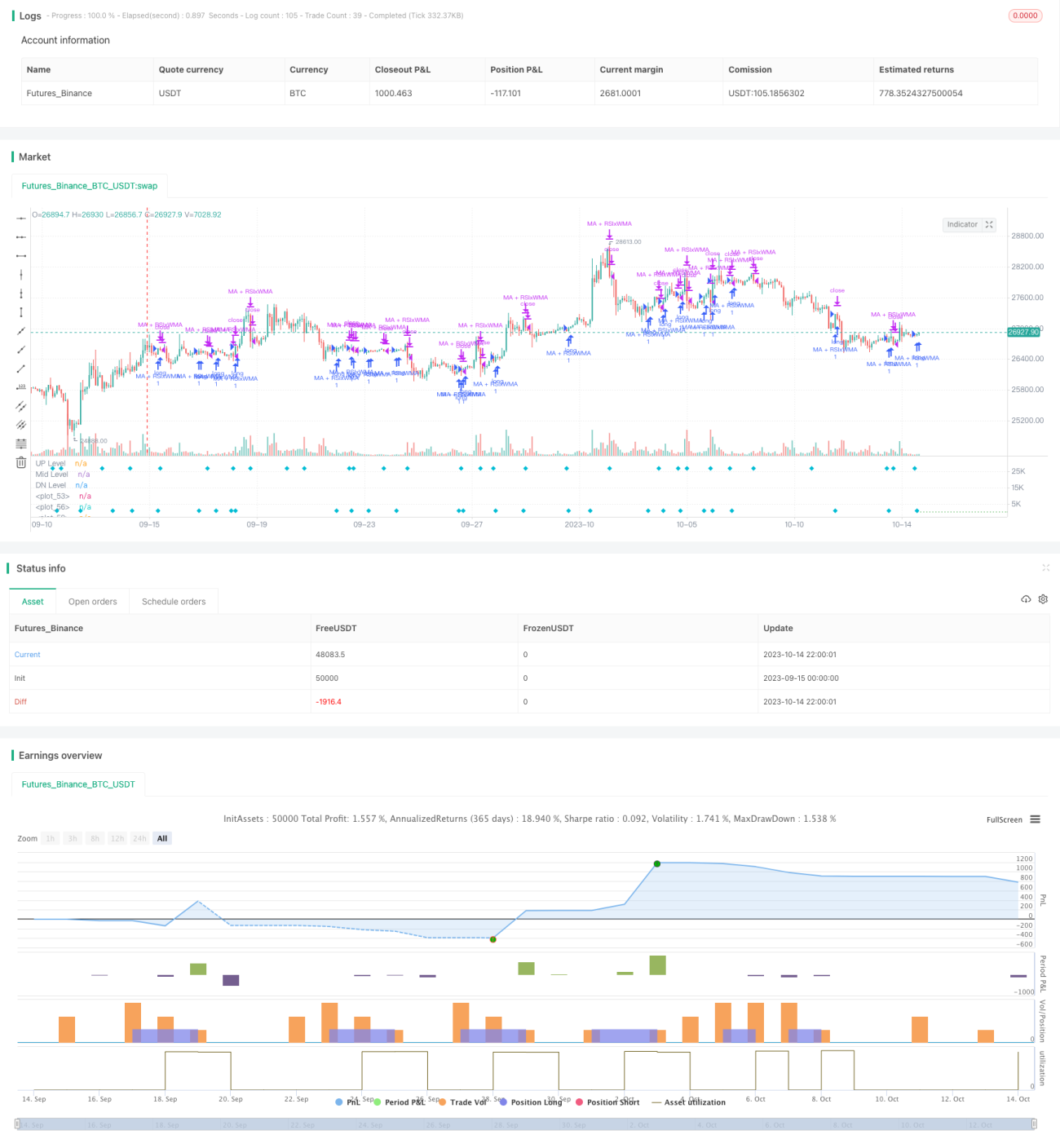

Ý tưởng cốt lõi của chiến lược này là đồng thời sử dụng Chỉ số sức mạnh tương đối (RSI) và các đường trung bình động với chu kỳ thời gian khác nhau để xác định điểm đảo chiều xu hướng, nhằm bắt kịp xu hướng trung và dài hạn đồng thời giao dịch ngắn hạn. Chiến lược này kết hợp nhiều tín hiệu giao dịch, hướng đến nâng cao tỷ lệ thành công.

Nguyên lý chiến lược

- Tính toán chỉ số RSI, cùng với đường EMA nhanh và đường WMA chậm.

- Khi đường chỉ số RSI vượt qua đường trung bình động WMA, tín hiệu mua/bán được phát sinh.

- Khi đường EMA nhanh vượt qua đường WMA chậm, tín hiệu mua/bán được phát sinh.

- Khi cả RSI và EMA cùng vượt qua WMA, tín hiệu mua/bán mạnh mẽ xuất hiện.

- Đồng thời, khi giá vượt qua đường trung bình động hỗ trợ, có thể củng cố tín hiệu chính.

- Thiết lập các điều kiện cắt lỗ, chốt lời.

Chiến lược này kết hợp các tín hiệu phá vỡ của nhiều chỉ báo kỹ thuật, sử dụng các đường trung bình động với tham số khác nhau để nhận diện xu hướng ở các chu kỳ khác nhau, qua đó nâng cao độ tin cậy của chiến lược. Chỉ số RSI đánh giá trạng thái quá mua/quá bán, đường EMA nhanh đánh giá xu hướng ngắn hạn, đường WMA chậm đánh giá xu hướng trung hạn, việc giá phá vỡ đường trung bình hỗ trợ xác nhận xu hướng. Sự kết hợp nhiều tín hiệu giúp nâng cao hiệu quả chiến lược.

Phân tích ưu điểm

- Tận dụng đặc tính đảo chiều của chỉ số RSI, có thể bắt được cơ hội đảo chiều tại vùng quá mua/quá bán.

- Đường trung bình động hỗ trợ đóng vai trò bộ lọc xu hướng, tránh các phá vỡ giả.

- Kết hợp nhiều khung thời gian, có thể theo dõi xu hướng dài hạn đồng thời bắt được cơ hội ngắn hạn.

- Kết hợp tín hiệu của nhiều chỉ báo, có thể nâng cao tỷ lệ thành công giao dịch.

- Thiết lập chiến lược cắt lỗ/chốt lời, có thể chủ động kiểm soát rủi ro.

Phân tích rủi ro

- Chỉ số RSI dễ phát sinh tín hiệu giả, cần có đường trung bình động hỗ trợ để lọc.

- Các đợt hồi phục trong xu hướng lớn có thể kích hoạt tín hiệu giao dịch ngược chiều, cần thận trọng.

- Cần tối ưu hóa tham số như độ dài chu kỳ RSI, chu kỳ đường trung bình động, v.v.

- Việc đặt điểm dừng lỗ cần thận trọng, tránh bị kẹt lệnh.

Rủi ro có thể được giảm nhẹ thông qua tối ưu hóa tham số, chiến lược dừng lỗ nghiêm ngặt và xem xét xu hướng chu kỳ lớn.

Hướng tối ưu hóa

- Tối ưu hóa tham số RSI để tìm độ dài chu kỳ tối ưu.

- Kiểm tra các tổ hợp đường trung bình động khác nhau.

- Thêm chỉ báo biến động như ATR để điều chỉnh linh hoạt mức cắt lỗ/chốt lời.

- Bổ sung mô-đun quản lý khối lượng giao dịch.

- Áp dụng kỹ thuật học máy để tối ưu hóa tham số và đánh giá chất lượng tín hiệu.

Tổng kết

Chiến lược này tích hợp tư duy giao dịch theo xu hướng và đảo chiều cực điểm, kết hợp phân tích đa khung thời gian và sử dụng tổng hợp nhiều chỉ báo, nhằm nâng cao tỷ lệ thắng. Điều quan trọng là phải kiểm soát rủi ro tốt, tối ưu hóa tham số và kịp thời xem xét ảnh hưởng của xu hướng chu kỳ lớn đến giao dịch. Nhìn chung, chiến lược này có tính thực tiễn và khả năng thích ứng cao. Sau này có thể áp dụng thêm các kỹ thuật tiên tiến hơn để nâng cao chất lượng chiến lược.

- 1