Chiến lược theo xu hướng với hai đường trung bình động và dải Bollinger

Tổng quan

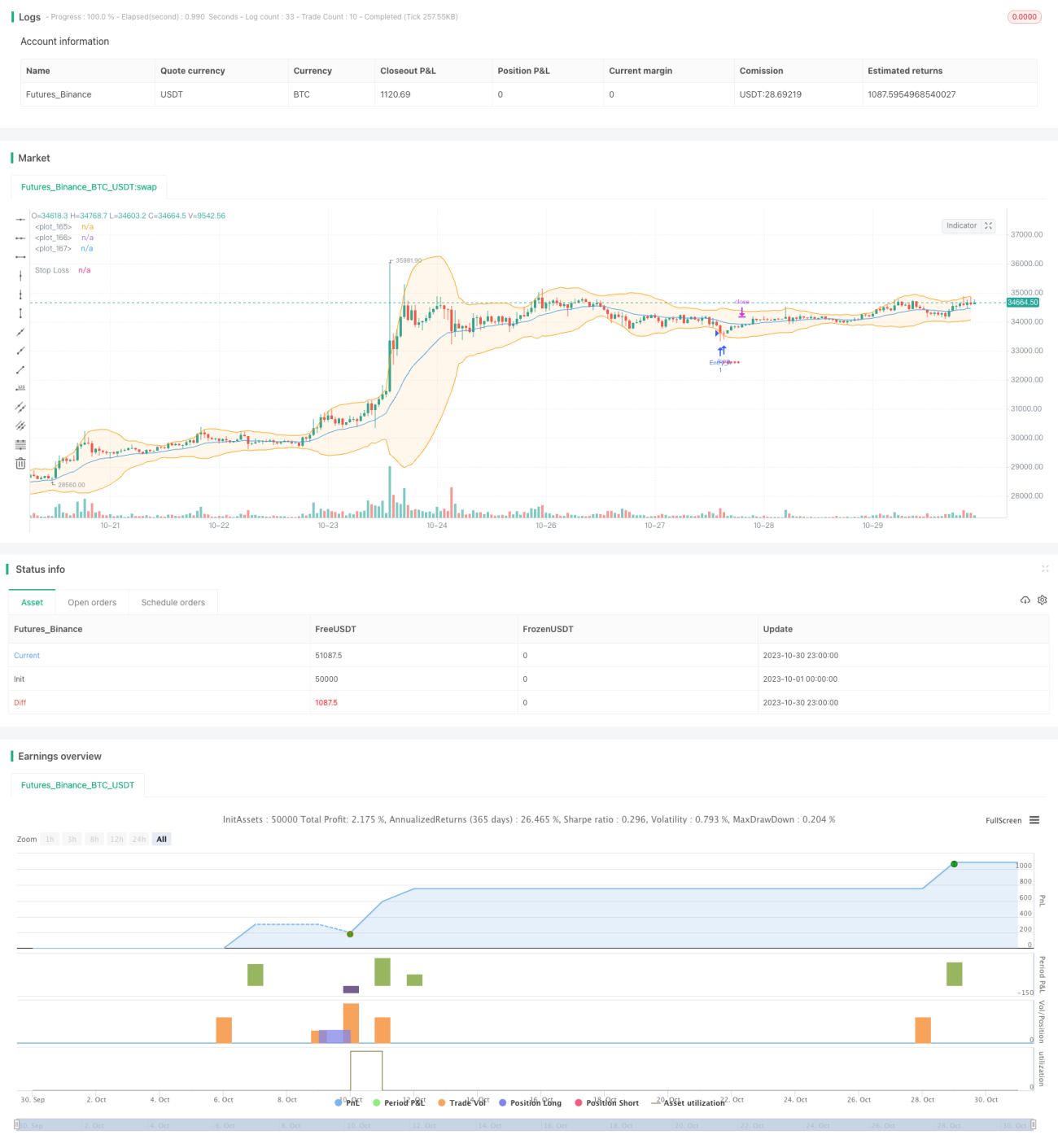

Chiến lược này dựa trên đường trung bình kép của Bollinger Bands để đưa ra quyết định giao dịch theo xu hướng. Nó tận dụng sự co hẹp và mở rộng của dải trên và dải dưới Bollinger Bands để xác định sự thay đổi xu hướng, mua vào gần dải dưới và bán ra gần dải trên, thực hiện mua thấp bán cao và chốt lời.

Nguyên lý chiến lược

Chiến lược này áp dụng đồng thời hai phiên bản của Bollinger Bands: Bollinger Bands đơn giản và Bollinger Bands tăng cường.

Bollinger Bands đơn giản sử dụng SMA của giá đóng cửa để tính đường giữa, trong khi Bollinger Bands tăng cường sử dụng EMA của giá đóng cửa để tính đường giữa.

Cả dải trên và dải dưới đều được tính bằng đường giữa ± N lần độ lệch chuẩn.

Chiến lược đánh giá xu hướng dựa trên khoảng cách (spread) giữa dải trên và dải dưới của Bollinger Bands. Khi spread nhỏ hơn ngưỡng đã đặt, điều đó cho thấy thị trường đang bước vào vùng xu hướng và có thể thực hiện giao dịch theo xu hướng.

Cụ thể, khi giá tiến gần dải dưới, chiến lược mua vào (long), và khi giá tiến gần dải trên, chiến lược bán ra để đóng vị thế. Phương pháp dừng lỗ là phần trăm dừng lỗ cố định, đồng thời có thể chọn kích hoạt trailing stop.

Mục tiêu lợi nhuận phụ thuộc vào việc chọn đóng vị thế gần đường giữa hoặc dải trên.

Chiến lược này cũng có thể chọn chỉ bán ra khi đảm bảo có lợi nhuận, nhằm ngăn ngừa thua lỗ.

Phân tích ưu điểm

Chiến lược này có các ưu điểm sau:

- Kết hợp hai Bollinger Bands, nâng cao hiệu quả ra quyết định

Áp dụng cả Bollinger Bands đơn giản và Bollinger Bands tăng cường, cho phép so sánh hiệu quả của hai phiên bản, chọn ra phiên bản tốt hơn, từ đó nâng cao hiệu quả ra quyết định.

- Đánh giá mức độ xu hướng dựa trên độ rộng kênh Bollinger Bands

Khi kênh Bollinger Bands thu hẹp, điều đó cho thấy thị trường đang bước vào giai đoạn xu hướng, lúc này giao dịch theo xu hướng có tỷ lệ thắng cao hơn.

- Phương pháp chốt lời và dừng lỗ linh hoạt

Sử dụng dừng lỗ theo phần trăm cố định để kiểm soát tổn thất từng lệnh. Đồng thời có thể chọn chốt lời gần đường giữa hoặc dải trên, cũng như kích hoạt trailing stop để khóa thêm lợi nhuận.

- Cơ chế bảo vệ ngăn ngừa thua lỗ

Chỉ bán ra khi đảm bảo có lợi nhuận, giúp ngăn chặn việc thua lỗ mở rộng.

Phân tích rủi ro

Chiến lược này cũng tồn tại các rủi ro sau:

- Rủi ro drawdown

Giao dịch theo xu hướng vốn có rủi ro drawdown nhất định, cần chịu áp lực tâm lý từ các khoản lỗ liên tiếp.

- Rủi ro thị trường đi ngang

Khi kênh Bollinger Bands mở rộng, điều đó cho thấy thị trường có thể bước vào giai đoạn đi ngang (sideways), lúc này hiệu quả giao dịch của chiến lược không tốt, cần tạm dừng giao dịch chờ xu hướng hình thành trở lại.

- Rủi ro dừng lỗ bị kích hoạt

Dừng lỗ theo phần trăm cố định có thể quá mạnh, cần điều chỉnh sang phương pháp dừng lỗ ôn hòa hơn như dừng lỗ dựa trên ATR.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa theo các hướng sau:

- Tối ưu hóa tham số Bollinger Bands

Có thể thử nghiệm các tham số đường trung bình và hệ số độ lệch chuẩn khác nhau để tìm ra bộ tham số Bollinger Bands phù hợp hơn với các thị trường khác nhau.

- Kết hợp thêm các chỉ báo để lọc tín hiệu

Dựa trên tín hiệu Bollinger Bands, có thể thêm các bộ lọc từ các chỉ báo như MACD, KD, v.v., để giảm giao dịch trong thị trường đi ngang.

- Tối ưu hóa chiến lược chốt lời và dừng lỗ

Có thể thử nghiệm các phương pháp trailing stop khác nhau, hoặc tối ưu điểm dừng lỗ dựa trên các chỉ báo như biên độ dao động, ATR, v.v.

- Tối ưu hóa quản lý vốn

Tối ưu hóa quản lý khối lượng cho mỗi lệnh giao dịch và thử nghiệm các chiến lược bổ sung vị thế khác nhau.

Tổng kết

Chiến lược này tích hợp ưu điểm của hai chỉ báo Bollinger Bands, đánh giá mức độ xu hướng dựa trên độ rộng kênh Bollinger Bands, thực hiện giao dịch bám xu hướng mua thấp bán cao trong suốt xu hướng. Đồng thời thiết lập cơ chế dừng lỗ khoa học để kiểm soát rủi ro. Chiến lược có thể được cải thiện tính ổn định hơn nữa thông qua tối ưu hóa tham số và kết hợp thêm các chỉ báo để lọc tín hiệu.

- 1