Chiến lược đường trung bình động đa khung thời gian với micro bị tháo rời

Tổng quan

Chiến lược này kết hợp sử dụng chỉ báo MACD và đường trung bình động đa khung thời gian, hình thành một chiến lược giao dịch hai chiều (long/short) tận dụng tín hiệu xu hướng và tín hiệu đảo chiều xu hướng. Chiến lược có thể thu thêm lợi nhuận trong xu hướng, đồng thời cũng nắm bắt các cơ hội đảo chiều.

Nguyên lý chiến lược

-

Sử dụng hai bộ đường EMA với chu kỳ khác nhau làm bộ lọc đa khung thời gian để xác định hướng long/short: EMA nhanh 15 phút cao hơn EMA chậm 1 giờ là bộ lọc tăng giá, EMA nhanh 15 phút thấp hơn EMA chậm 1 giờ là bộ lọc giảm giá.

-

Khi phát hiện sự phân kỳ trên MACD (đường histogram và giá đi ngược chiều), xác định khả năng đảo chiều.

-

Khi bộ lọc tăng giá được kích hoạt, nếu phát hiện phân kỳ tăng (giá tạo đỉnh cao hơn nhưng MACD không tạo đỉnh cao hơn), chờ MACD cắt lên trên đường zero, vào lệnh long; khi bộ lọc giảm giá được kích hoạt, nếu phát hiện phân kỳ giảm (giá tạo đáy thấp hơn nhưng MACD không tạo đáy thấp hơn), chờ MACD cắt xuống dưới đường zero, vào lệnh short.

-

Phương pháp dừng lỗ là trailing stop liên tục, được tính dựa trên biên độ dao động giá cao nhất và thấp nhất. Chốt lời là bội số nhất định của mức dừng lỗ.

-

Khi đường histogram MACD cắt qua đường zero, thoát lệnh.

Phân tích ưu điểm

-

Bộ EMA đa khung thời gian có thể đánh giá xu hướng trên khung lớn, tránh giao dịch ngược xu hướng.

-

Phân kỳ MACD có thể nắm bắt cơ hội đảo chiều giá, phù hợp với chiến lược đảo chiều.

-

Trailing stop động giúp khóa lợi nhuận và hạn chế thua lỗ.

-

Khoảng cách chốt lời được tính dựa trên mức dừng lỗ giúp đạt được lợi nhuận kỳ vọng.

Phân tích rủi ro

-

Bộ lọc đường EMA có thể đưa ra nhận định sai hướng trong giai đoạn đi ngang.

-

Sau phân kỳ MACD, biên độ hồi phục có thể không đủ, dẫn đến không có lợi nhuận.

-

Khoảng cách dừng lỗ cài đặt không phù hợp, có thể quá rộng hoặc quá hẹp.

-

Không gian đảo chiều không đủ, lợi nhuận bị giới hạn.

-

Cần căn đúng thời điểm vào lệnh đảo chiều; vào quá sớm hoặc quá muộn đều có thể gây thua lỗ.

Hướng tối ưu

-

Có thể thử nghiệm các bộ tham số EMA khác nhau để có nhận định xu hướng chính xác hơn.

-

Có thể thử điều chỉnh tham số MACD thành bộ nhạy hơn.

-

Có thể thử nghiệm các tỷ lệ dừng lỗ/chốt lời khác nhau.

-

Có thể thêm điều kiện lọc phụ để tránh bẫy hồi phục giả, ví dụ thêm EMA khung thời gian lớn hơn để đánh giá xu hướng tổng thể.

-

Có thể tối ưu điều kiện xác nhận điểm vào đảo chiều, đảm bảo xu hướng đảo chiều đủ chín muồi.

Tổng kết

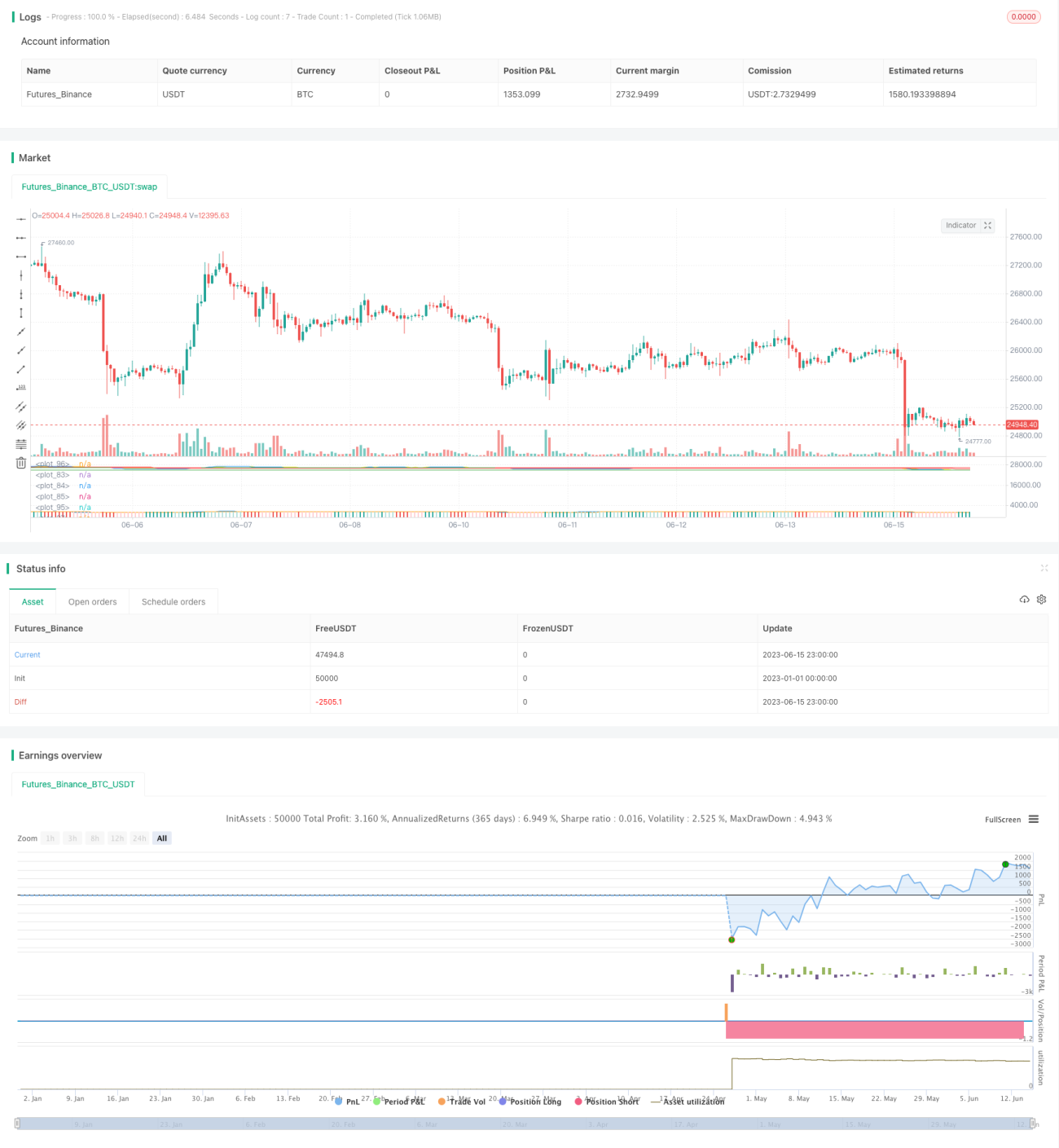

Chiến lược này kết hợp bộ lọc xu hướng, tín hiệu đảo chiều xu hướng và quản lý dừng lỗ/chốt lời động, có thể đi theo xu hướng cũng như bắt đảo chiều. Thông qua điều chỉnh tham số và tối ưu điều kiện lọc, chiến lược có thể thích ứng với nhiều môi trường thị trường hơn, thu được lợi nhuận ổn định trong khi kiểm soát rủi ro. Chiến lược có tính phổ biến và giá trị ứng dụng nhất định, là một ví dụ điển hình về việc kết hợp đa khung thời gian và chỉ báo.

- 1