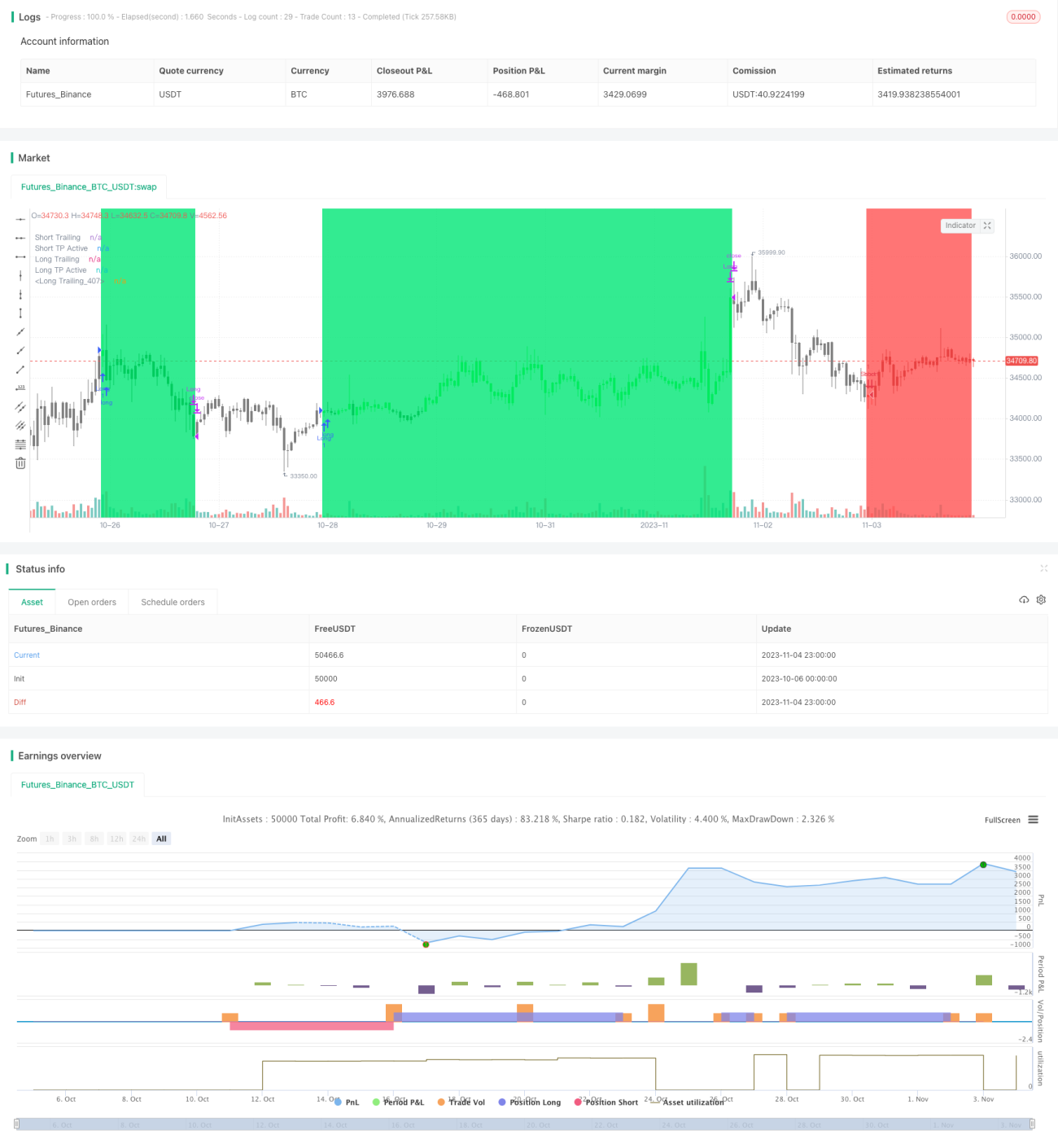

Chiến lược giao dịch momentum sử dụng nhiều đường MA

Tổng quan

Chiến lược giao dịch này kết hợp nhiều đường trung bình động và chỉ báo động lượng để xác định hướng và sức mạnh của xu hướng, thiết lập vị thế ở giai đoạn đầu của xu hướng, sau đó sử dụng các phương pháp như trailing stop, trailing take profit để tối ưu hóa lợi nhuận và kiểm soát rủi ro, nhằm mục tiêu bắt được những biến động giá lớn trong xu hướng trung và dài hạn.

Nguyên lý chiến lược

-

Sử dụng hai bộ đường trung bình động với các tham số khác nhau để tạo thành đường nhanh và đường chậm:

- Đường nhanh được tạo thành từ đường trung bình động hàm mũ 5 chu kỳ và đường trung bình động gia quyền 25 chu kỳ, đại diện cho xu hướng ngắn hạn.

- Đường chậm được tạo thành từ đường trung bình động hàm mũ 28 chu kỳ và đường trung bình động gia quyền 72 chu kỳ, đại diện cho xu hướng trung và dài hạn.

-

Khi đường nhanh cắt lên trên đường chậm, điều đó cho thấy xu hướng ngắn hạn bắt đầu mạnh hơn xu hướng trung và dài hạn, đây là tín hiệu vào lệnh.

-

Kết hợp chỉ báo động lượng RSI, chỉ vào lệnh khi RSI ở vùng thấp (tín hiệu mua) hoặc vùng cao (tín hiệu bán) để lọc các tín hiệu phá vỡ giả.

-

Sau khi vào lệnh, sử dụng trailing stop để thu hẹp lỗ và trailing take profit để chốt lãi.

-

Khi đường nhanh cắt xuống dưới đường chậm, báo hiệu sự đảo chiều xu hướng, lúc đó sẽ thoát lệnh bằng stop loss hoặc take profit.

Phân tích ưu điểm

- Sự kết hợp của hai đường trung bình động giúp lọc nhiễu, xác định hướng và sức mạnh của xu hướng ở đoạn giữa.

- Chỉ thiết lập vị thế ở giai đoạn đầu của xu hướng, tránh những tổn thất không cần thiết do phá vỡ giả.

- Kết hợp chỉ báo động lượng để lọc lệnh vào, nâng cao chất lượng lệnh vào.

- Trailing stop thu hẹp thua lỗ mỗi lệnh, giảm thiểu thiệt hại do các điểm lỗ riêng lẻ.

- Trailing take profit giúp lợi nhuận trở nên đáng kể, gia tăng lợi nhuận khi thị trường thuận lợi.

Phân tích rủi ro

- Hai đường trung bình động có độ trễ tại các điểm xoay chiều xu hướng, có thể bỏ lỡ cơ hội đảo chiều.

- Có thể rút ngắn chu kỳ của các đường trung bình động để chúng nhạy hơn.

- Phá vỡ giả gây ra các lệnh vào không cần thiết.

- Có thể thêm nhiều chỉ báo lọc hơn.

- Khoảng cách stop loss hoặc take profit chưa được tối ưu, có thể quá rộng hoặc quá chặt.

- Có thể tối ưu hóa tham số thông qua backtest để tìm khoảng cách stop loss/take profit tốt nhất.

- Chiến lược theo hướng, chỉ phù hợp với thị trường có xu hướng.

- Có thể lựa chọn có sử dụng chiến lược này hay không dựa trên tình hình chung của thị trường.

Hướng tối ưu hóa

- Tối ưu hóa các tham số của đường trung bình động để tìm bộ tham số đại diện tốt nhất cho xu hướng.

- Thêm các chỉ báo lọc xu hướng, ví dụ ATR trailing stop động, chỉ báo dòng năng lượng, v.v.

- Tối ưu hóa tham số stop loss/take profit để tìm bộ tham số tốt nhất.

- Thêm đánh giá về thị trường lớn để quyết định có kích hoạt chiến lược hay không.

- Thêm đánh giá tổng hợp đa khung thời gian, sử dụng hướng xu hướng của khung lớn hơn để dẫn dắt hướng của chiến lược khung nhỏ.

Tổng kết

Chiến lược này kết hợp các đường trung bình động và chỉ báo động lượng, nhằm mục tiêu xác định các điểm vào lệnh sớm trong các xu hướng mới nổi, quản lý rủi ro và lợi nhuận thông qua việc cắt lỗ và chốt lời kịp thời. Mặc dù vẫn cần tối ưu hóa tham số và quy tắc để thích ứng với các điều kiện thị trường rộng hơn, nhưng nó đã có khung cơ bản và hướng đi để bắt xu hướng trung và dài hạn. Thông qua tối ưu hóa liên tục, chiến lược này được kỳ vọng sẽ phát triển thành một chiến lược giao dịch theo xu hướng ổn định và hiệu quả.

- 1