Chiến lược giao dịch dao động dựa trên hai đường trung bình động

Tổng quan

Chiến lược này là một chiến lược giao dịch dao động dựa trên hai đường trung bình động. Nó sử dụng sự giao cắt của đường trung bình động nhanh và đường trung bình động chậm làm tín hiệu mua và bán. Khi đường trung bình động nhanh cắt lên trên đường trung bình động chậm từ phía dưới, tín hiệu mua được tạo ra; khi đường trung bình động nhanh cắt xuống dưới đường trung bình động chậm từ phía trên, tín hiệu bán được tạo ra. Chiến lược này phù hợp với thị trường dao động, có thể nắm bắt biến động giá ngắn hạn để kiếm lợi nhuận.

Nguyên lý chiến lược

Chiến lược này sử dụng RMA có độ dài 6 làm đường trung bình động nhanh và HMA có độ dài 4 làm đường trung bình động chậm. Chiến lược xác định xu hướng giá và tạo tín hiệu giao dịch thông qua sự giao cắt của đường nhanh và đường chậm.

Khi đường nhanh cắt lên trên đường chậm từ phía dưới, điều đó cho thấy giá trong ngắn hạn chuyển từ giảm sang tăng, đây là thời điểm chuyển đổi vị thế, do đó chiến lược tạo tín hiệu mua tại thời điểm này. Khi đường nhanh cắt xuống dưới đường chậm từ phía trên, điều đó cho thấy giá trong ngắn hạn chuyển từ tăng sang giảm, đây là thời điểm chuyển đổi vị thế, do đó chiến lược tạo tín hiệu bán tại thời điểm này.

Ngoài ra, chiến lược còn kiểm tra đánh giá xu hướng dài hạn để tránh giao dịch ngược xu hướng. Chỉ khi đánh giá xu hướng dài hạn cũng đồng ý với tín hiệu đó thì tín hiệu mua và bán thực tế mới được tạo ra.

Lợi thế của chiến lược

Chiến lược này có những lợi thế sau:

- Sử dụng giao cắt hai đường trung bình động để xác định các điểm đảo chiều giá ngắn hạn một cách hiệu quả.

- Sự kết hợp độ dài giữa đường nhanh và đường chậm hợp lý, có thể tạo ra các tín hiệu giao dịch chính xác hơn.

- Kết hợp đánh giá xu hướng dài hạn và ngắn hạn, có thể lọc bỏ phần lớn các tín hiệu giao dịch nhiễu.

- Thực hiện logic chốt lời và cắt lỗ, có thể chủ động tránh rủi ro.

- Dễ hiểu và dễ triển khai, phù hợp cho người mới bắt đầu giao dịch định lượng.

Rủi ro và cách khắc phục

Chiến lược này cũng tồn tại một số rủi ro:

- Chiến lược hai đường trung bình động dễ dẫn đến tình trạng nhiều lần lợi nhuận nhỏ nhưng một lần thua lỗ lớn. Giải pháp là điều chỉnh hợp lý mức chốt lời và cắt lỗ.

- Trong thị trường dao động, tín hiệu giao dịch xuất hiện thường xuyên, có thể dẫn đến giao dịch quá mức. Giải pháp là nới lỏng điều kiện giao dịch một cách phù hợp để giảm số lượng giao dịch.

- Các tham số của chiến lược dễ bị tối ưu hóa quá mức, hiệu quả thực tế có thể không tốt. Giải pháp là kiểm tra độ bền vững của tham số.

- Chiến lược hoạt động kém trong thị trường có xu hướng. Giải pháp là thêm mô-đun đánh giá xu hướng hoặc kết hợp với chiến lược xu hướng.

Hướng tối ưu hóa

Các hướng tối ưu hóa tiếp theo cho chiến lược này bao gồm:

- Cập nhật chỉ báo đường trung bình động, sử dụng bộ lọc thích ứng như Kalman.

- Bổ sung mô-đun học máy, sử dụng AI để huấn luyện xác định điểm mua bán.

- Thêm mô-đun quản lý vốn, giúp kiểm soát rủi ro tự động hơn.

- Kết hợp với các yếu tố tần suất cao để tìm tín hiệu giao dịch mạnh hơn.

- Kinh doanh chênh lệch giá đa thị trường, đa sản phẩm.

Tổng kết

Nhìn chung, chiến lược dao động hai đường trung bình động này là một chiến lược giao dịch định lượng điển hình và thực tế. Nó có khả năng thích ứng cao, người mới bắt đầu có thể học được nhiều kiến thức về phát triển chiến lược từ đó. Đồng thời, nó cũng có nhiều không gian để cải tiến, có thể kết hợp thêm nhiều kỹ thuật định lượng để tối ưu hóa nhằm đạt được hiệu quả chiến lược tốt hơn.

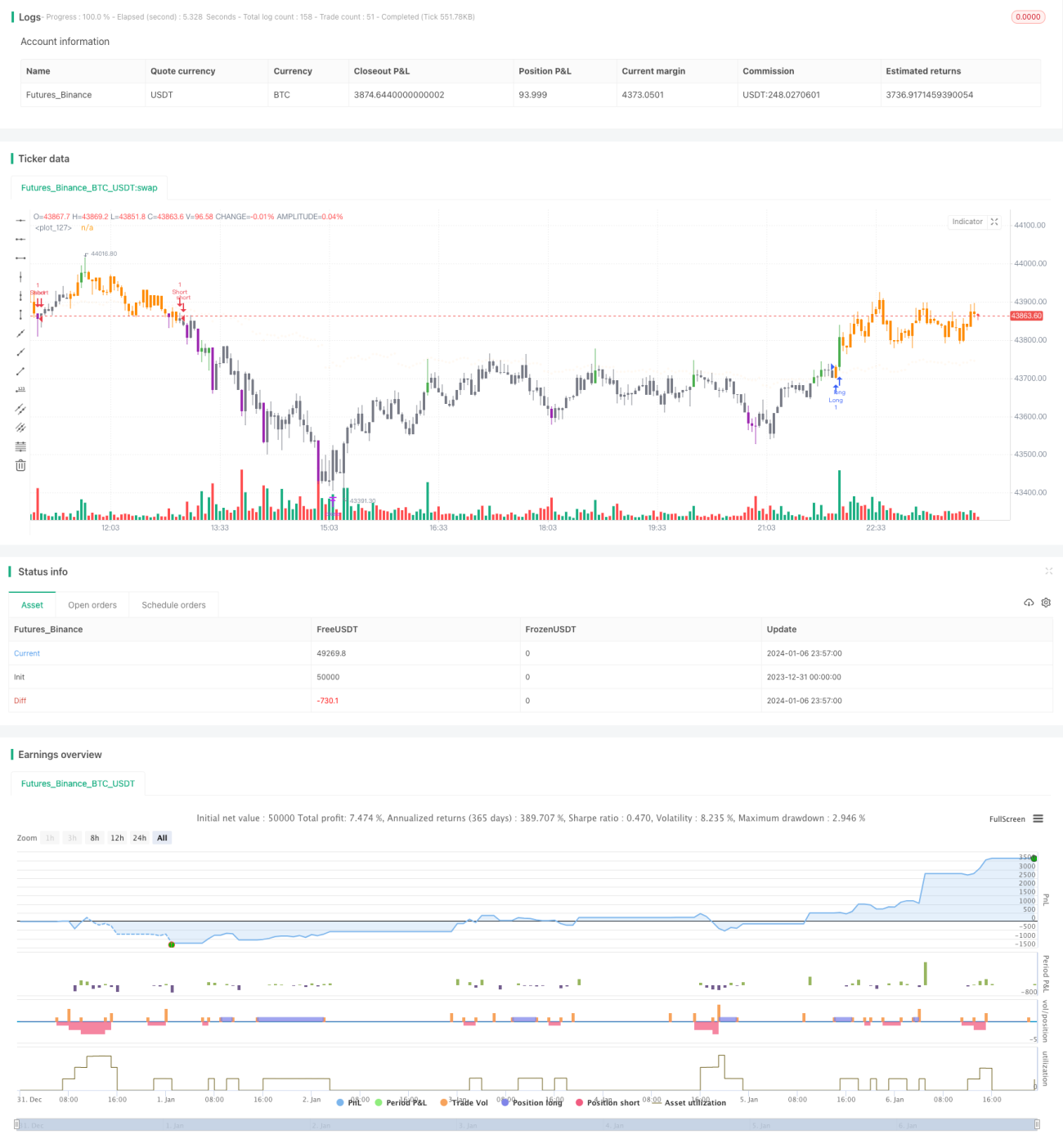

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © dc_analytics

// https://datacryptoanalytics.com/

- 1