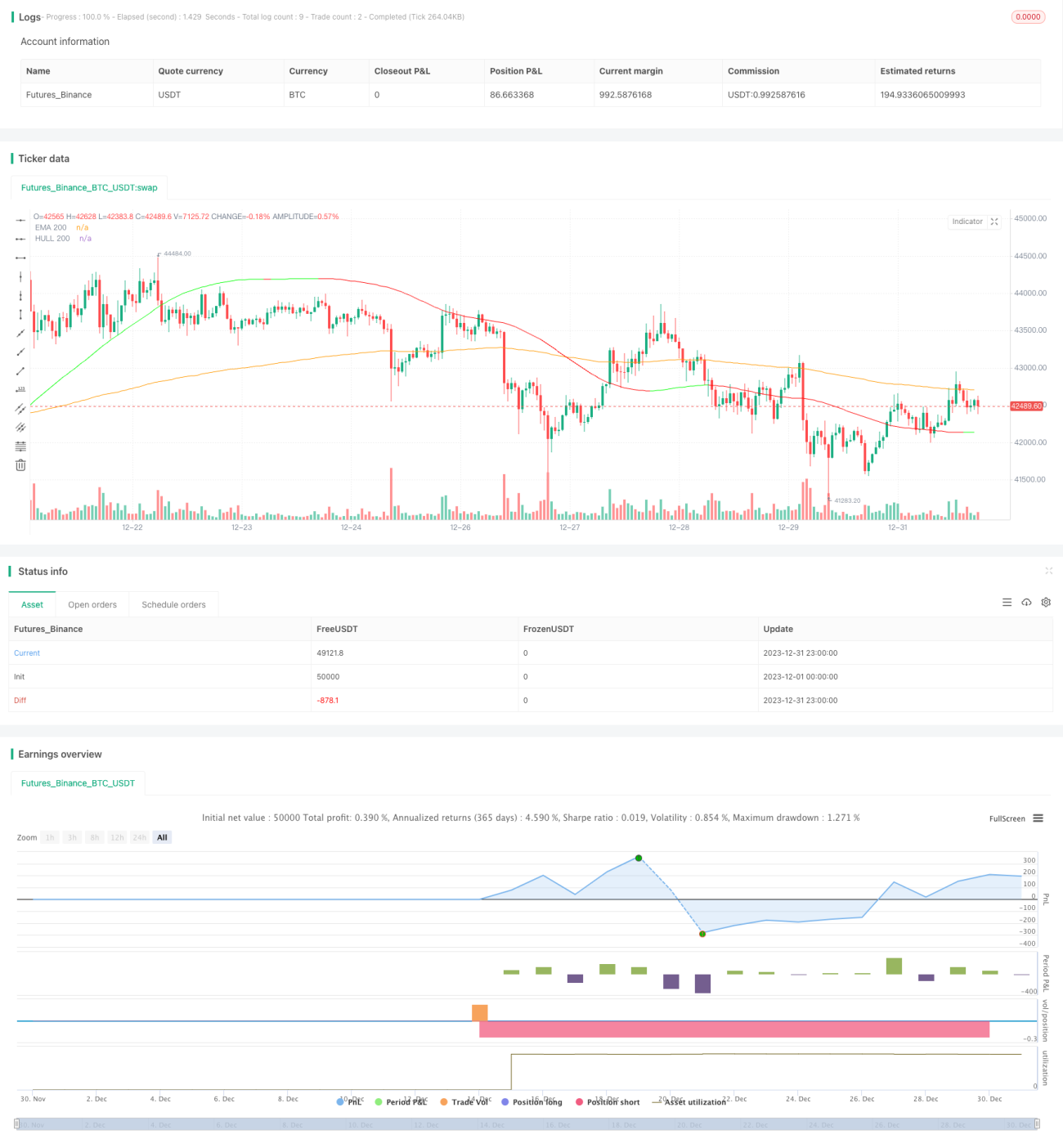

Chiến lược Động lượng và Đường trung bình Tích lũy

Tổng quan

Chiến lược này chủ yếu sử dụng đường trung bình động HMA và EMA để hình thành sự tích lũy của các đường trung bình nhằm xác định thời điểm mua vào. Khi HMA cắt lên trên EMA, được coi là kết thúc giai đoạn tích lũy, hình thành xu hướng tăng mới, do đó mua vào ngay khi HMA cắt lên trên EMA.

Chiến lược cũng kết hợp chỉ báo RSI để phát hiện tình trạng quá mua/quá bán. Cho phép mua vào khi RSI dưới 70, và xem xét chốt lời một phần khi RSI trên 80.

Nguyên lý chiến lược

Chiến lược này sử dụng EMA 200 chu kỳ và HMA để xây dựng hệ thống đường trung bình. Trong đó, chỉ báo HMA là đường trung bình động nhạy hơn được cải tiến dựa trên EMA. Khi HMA cắt lên trên EMA, cho thấy giai đoạn tích lũy kết thúc, giá cổ phiếu bắt đầu tăng. Lúc này, nếu chỉ báo RSI không hiển thị quá mua, thì phát sinh tín hiệu mua.

Trong trường hợp đã có vị thế, nếu giá giảm trở lại, HMA lại cắt xuống dưới EMA, cho thấy sự tích lũy mới bắt đầu, thì sẽ đóng toàn bộ vị thế. Đồng thời, nếu RSI cắt lên trên 80, sẽ chốt lời 20% một phần để tránh thua lỗ.

Logic giao dịch của chiến lược này khá đơn giản, chủ yếu dựa trên sự giao cắt lên/xuống của HMA và EMA, kết hợp với đánh giá vùng cao/thấp của RSI, hình thành một chiến lược giao dịch tương đối ổn định.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là sử dụng mô hình giao dịch tích lũy của EMA và HMA, có thể lọc bỏ hầu hết các tín hiệu phá vỡ giả, từ đó nâng cao tỷ lệ lợi nhuận. Đồng thời, sự hỗ trợ của chỉ báo RSI cũng có thể kiểm soát rủi ro hiệu quả, sự kết hợp này khiến chiến lược rất phù hợp với thị trường dao động tích lũy.

Ngoài ra, chiến lược chỉ sử dụng 3 chỉ báo và logic đơn giản, giúp việc tối ưu hóa tham số và backtest thuận tiện hơn, có lợi cho việc xác minh và cải tiến chiến lược.

Phân tích rủi ro

Mặc dù chiến lược này có những ưu điểm nhất định, nhưng vẫn tồn tại một số rủi ro cần lưu ý. Ví dụ, thời gian nắm giữ có thể khá dài, cần có đủ nguồn vốn hỗ trợ. Nếu gặp giai đoạn đi ngang kéo dài, không thể thoát lỗ nhanh chóng, dễ dẫn đến tình trạng lỗ lan rộng.

Ngoài ra, chiến lược chủ yếu phụ thuộc vào chỉ báo đường trung bình, nếu giá có sự đột biến phá vỡ bất thường, biện pháp cắt lỗ có thể không kịp phát huy tác dụng, mang lại rủi ro lớn hơn. Hơn nữa, cài đặt tham số cũng ảnh hưởng đến hiệu suất của chiến lược, cần phải thực hiện nhiều thử nghiệm để tìm ra tham số tối ưu.

Hướng tối ưu hóa

Xét đến các rủi ro trên, chiến lược có thể được tối ưu hóa từ các khía cạnh sau:

-

Kết hợp chỉ báo biến động, điều chỉnh quy mô vị thế động theo biến động thị trường.

-

Thêm chỉ báo xu hướng để đánh giá, tránh các giao dịch đảo chiều không cần thiết.

-

Tối ưu hóa tham số đường trung bình động để phù hợp hơn với đặc điểm thị trường hiện tại.

-

Áp dụng cắt lỗ theo thời gian, giảm thiểu tối đa vấn đề thua lỗ quá lớn cho mỗi giao dịch.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược dao động tích lũy kinh điển và đơn giản. Nó chủ yếu được áp dụng cho giao dịch ngắn hạn và trung hạn của các chỉ số chứng khoán và cổ phiếu phổ biến, có thể thu được giá trị Alpha tương đối ổn định. Với việc tối ưu hóa tham số và tăng cường các biện pháp kiểm soát rủi ro, hiệu suất của chiến lược vẫn còn nhiều dư địa cải thiện.

- 1