Chiến lược giao dịch phân tách đa/không dựa trên chỉ báo RSI

Tổng quan

Chiến lược này sử dụng chỉ báo RSI để nhận diện hiện tượng phân kỳ đa/không, từ đó đưa ra quyết định giao dịch. Ý tưởng cốt lõi là khi giá tạo đáy mới nhưng RSI tạo đỉnh mới, hình thành tín hiệu "phân kỳ tăng", cho thấy đáy đã hình thành, vào lệnh mua; khi giá tạo đỉnh mới nhưng RSI tạo đáy mới, hình thành tín hiệu "phân kỳ giảm", cho thấy đỉnh đã hình thành, vào lệnh bán.

Nguyên lý chiến lược

Chiến lược này chủ yếu sử dụng chỉ báo RSI để nhận diện hiện tượng phân kỳ giữa giá và RSI, cụ thể như sau:

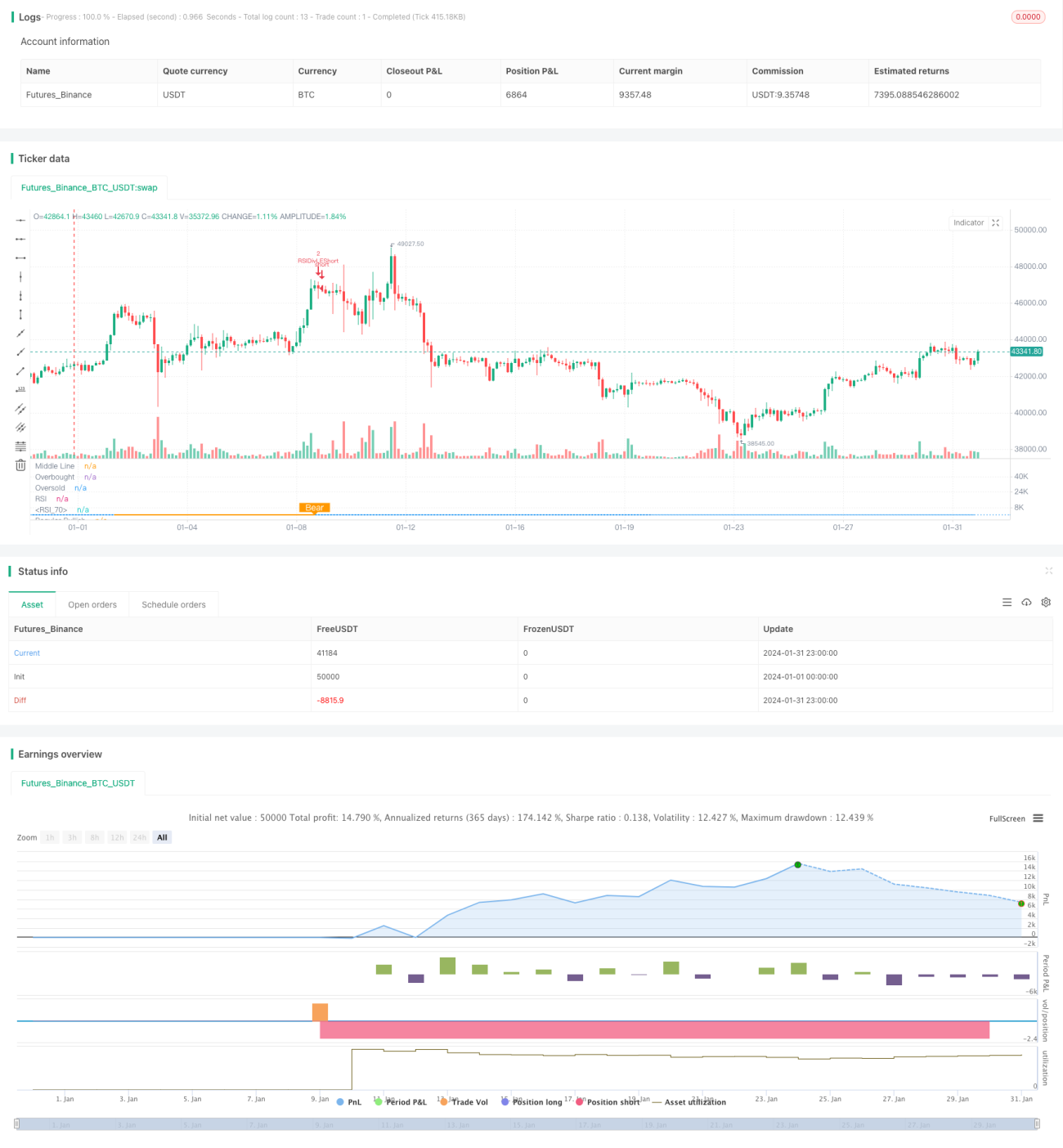

- Sử dụng tham số chỉ báo RSI là 13, nguồn dữ liệu là giá đóng cửa

- Xác định phạm vi hồi quy trái cho phân kỳ tăng là 14 ngày, phạm vi hồi quy phải là 2 ngày

- Xác định phạm vi hồi quy trái cho phân kỳ giảm là 47 ngày, phạm vi hồi quy phải là 1 ngày

- Khi giá tạo đáy thấp hơn, nhưng chỉ báo RSI tạo đáy cao hơn, điều kiện phân kỳ tăng được thỏa mãn, tạo tín hiệu mua

- Khi giá tạo đỉnh cao hơn, nhưng chỉ báo RSI tạo đỉnh thấp hơn, điều kiện phân kỳ giảm được thỏa mãn, tạo tín hiệu bán

Bằng cách nhận diện hiện tượng phân kỳ giữa giá và RSI, có thể nắm bắt trước các điểm đảo chiều của xu hướng giá, từ đó đưa ra quyết định giao dịch.

Lợi thế của chiến lược

Chiến lược này có những lợi thế chính sau:

- Nhận diện hiện tượng phân kỳ giữa giá và RSI, có thể dự đoán trước điểm đảo chiều của xu hướng giá, nắm bắt cơ hội giao dịch

- Do sử dụng phân tích chỉ báo, nên không bị ảnh hưởng bởi cảm xúc chủ quan

- Sử dụng khoảng hồi quy cố định để nhận diện phân kỳ, tránh việc điều chỉnh tham số thường xuyên

- Kết hợp với các điều kiện bổ sung như RSI ngày, có thể giảm xác suất giao dịch sai

Rủi ro và giải pháp

Chiến lược này cũng tồn tại một số rủi ro:

-

Phân kỳ của chỉ báo RSI không nhất thiết báo hiệu giá sẽ đảo chiều ngay lập tức, có thể có độ trễ về thời gian, dẫn đến rủi ro chạm stop loss. Giải pháp là nới lỏng biên độ stop loss một cách phù hợp, cho phép giá có đủ thời gian để xác nhận tín hiệu phân kỳ.

-

Hiện tượng phân kỳ kéo dài quá lâu cũng làm tăng rủi ro. Giải pháp là kết hợp chỉ báo RSI dài hạn hơn như ngày hoặc tuần làm bộ lọc.

-

Biên độ phân kỳ quá nhỏ cũng không thể xác nhận đảo chiều xu hướng, cần mở rộng khoảng hồi quy thích hợp để tìm kiếm phân kỳ RSI rõ ràng hơn.

Hướng tối ưu hóa chiến lược

Chiến lược này có thể được tối ưu hóa theo các hướng sau:

-

Tối ưu hóa tham số RSI, tìm tổ hợp tham số tốt nhất

-

Thử nghiệm các chỉ báo kỹ thuật khác như MACD, KD để nhận diện hiện tượng phân kỳ

-

Thêm các điều kiện lọc trong giai đoạn dao động, tránh giao dịch sai khi thị trường sideway

-

Kết hợp chỉ báo RSI trên nhiều khung thời gian, tìm tín hiệu tổ hợp tốt nhất

Kết luận

Chiến lược giao dịch phân kỳ RSI nhận diện hiện tượng phân kỳ giữa chỉ báo RSI và giá, phán đoán điểm đảo chiều của xu hướng giá, từ đó xây dựng tín hiệu giao dịch. Chiến lược này đơn giản và thiết thực, thông qua việc tối ưu hóa cài đặt tham số và bổ sung bộ lọc, có thể nâng cao hơn nữa xác suất lợi nhuận. Nhìn chung, chiến lược phân kỳ RSI là một chiến lược giao dịch định lượng rất hiệu quả.

- 1