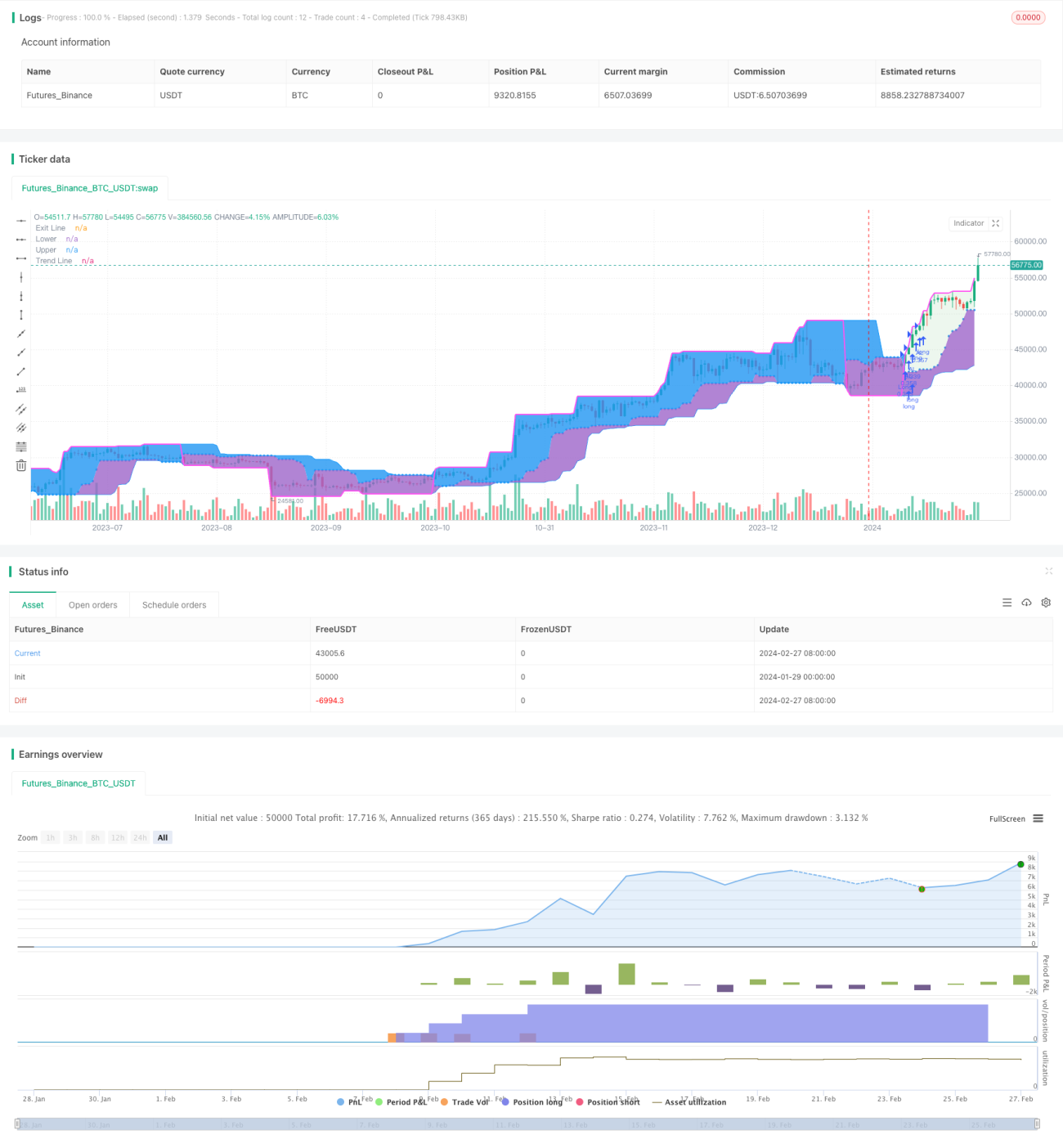

Hệ thống quyết định giao dịch rùa

Tổng quan

Hệ thống quyết định giao dịch biển là một chiến lược giao dịch theo dõi xu hướng dựa trên lý thuyết đột phá. Nó tạo ra tín hiệu giao dịch bằng cách tạo ra trung bình di chuyển của giá cao nhất và giá thấp nhất của các loại giao dịch, để nhận diện xu hướng tiềm năng. Nó tạo ra tín hiệu giao dịch khi giá phá vỡ giá cao nhất hoặc thấp nhất trong chu kỳ được chỉ định.

Nguyên tắc chiến lược

Các tín hiệu chiến lược cốt lõi của hệ thống quyết định giao dịch của Bạch Dương được tạo ra bằng cách so sánh giá với giá cao nhất chu kỳ N1 và giá thấp nhất chu kỳ N2. Khi giá vượt qua mức cao nhất chu kỳ N1, nó tạo ra tín hiệu mua; Khi giá vượt qua mức thấp nhất chu kỳ N2, nó tạo ra tín hiệu bán. Chế độ đóng cửa được sử dụng để kiểm soát việc tạo ra tín hiệu mới.

Sau khi mở vị trí, nó sẽ so sánh giá với giá dừng trong thời gian thực, tạo ra tín hiệu dừng di động. Đồng thời, nó cũng sẽ so sánh giá với đường gia tăng, tạo ra tín hiệu gia tăng. Giá dừng và đường gia tăng đều liên quan đến ATR.

Mỗi lần mở vị trí, các đơn vị nắm giữ được tính bằng cách lấy một tỷ lệ số tiền ban đầu để tránh ảnh hưởng của tổn thất đơn lẻ đến tổng vốn. Các tổn thất đơn lẻ được giới hạn trong một phạm vi nhất định.

Phân tích lợi thế

Các hệ thống quyết định giao dịch của Hải Dương có những ưu điểm sau:

-

Lấy xu hướng tiềm năng: Xác định hướng xu hướng tiềm năng bằng cách so sánh giá với mối quan hệ giữa giá cao nhất và giá thấp nhất theo chu kỳ, có thể nắm bắt xu hướng giá tiềm năng sớm hơn.

-

Quản lý rủi ro: Sử dụng quản lý tiền và dừng lỗ để kiểm soát rủi ro tổn thất cá nhân và tổng thể.

-

Quản lý cổ phần: Một cổ phần phù hợp có thể mang lại lợi nhuận bổ sung trong xu hướng.

-

Tính toàn vẹn: kết hợp quản lý tài chính, quản lý lỗ hổng và quản lý gia tăng, làm cho hệ thống ra quyết định hoàn chỉnh hơn.

-

Đơn giản và rõ ràng: quy tắc tạo tín hiệu đơn giản, trực tiếp, dễ hiểu và xác minh.

Phân tích rủi ro

Có một số rủi ro đối với hệ thống quyết định giao dịch trên biển:

-

Rủi ro phá vỡ giả: Giá có thể xảy ra phá vỡ giả giá cao nhất hoặc giá thấp nhất, gây ra tín hiệu sai. Bạn có thể điều chỉnh tham số thích hợp để lọc một số phá vỡ giả.

-

Rủi ro đảo ngược xu hướng: Rủi ro tăng lỗ do giá đảo ngược sau khi gia tăng. Bạn nên hạn chế số lần gia tăng và dừng lỗ kịp thời.

-

Rủi ro tối ưu hóa tham số: Các thiết lập tham số của thị trường khác nhau có thể khác nhau, nên phân chia tham số tối ưu hóa thị trường để giảm rủi ro.

Hướng tối ưu hóa

Các hệ thống quyết định giao dịch trên biển cũng có thể được tối ưu hóa theo các khía cạnh sau:

-

Thêm bộ lọc: phát hiện mức độ phá vỡ giá và lọc ra một số phá vỡ giả.

-

Tối ưu hóa chiến lược dừng lỗ: Làm thế nào để theo dõi lỗ một cách hợp lý, tìm sự cân bằng trong việc bảo vệ lợi nhuận và giảm lỗ không cần thiết.

-

Tối ưu hóa tham số phân khúc: Gói tham số tối ưu hóa cho các đặc điểm khác nhau của giống.

-

Tăng học máy: Sử dụng thuật toán học máy để hỗ trợ định hướng xu hướng.

Tóm tắt

Hệ thống ra quyết định giao dịch trên bờ biển đánh giá hướng xu hướng tiềm năng bằng cách so sánh giá với mối quan hệ giữa giá cao nhất và giá thấp nhất trong một chu kỳ nhất định và kết hợp với mô-đun quản lý rủi ro để xây dựng toàn bộ hệ thống ra quyết định. Nó có khả năng theo dõi xu hướng mạnh mẽ, đồng thời cũng có một số rủi ro giả mạo và các vấn đề tối ưu hóa tham số. Chiến lược này có thể được sử dụng như một mô hình cơ bản của giao dịch định lượng và dựa trên đó mở rộng và tối ưu hóa để phát triển hệ thống ra quyết định phù hợp với chính mình.

/*backtest

start: 2024-01-29 00:00:00

end: 2024-02-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © 李和邪

// 本脚本所有内容只适用于交流学习,不构成投资建议,所有后果自行承担。

//@version=5- 1