মিল মেশিন

লেখক:চাওঝাং, তারিখ: ২০২২-০৫-০৮ ১১ঃ২১ঃ২০ট্যাগঃএটিআর

হ্যালো ট্রেডার,

এখন আমি আপনাদের সামনে একটি নির্ভরযোগ্য, লাভজনক ট্রেডিং কৌশল খুঁজে বের করার জন্য আমার যাত্রার দ্বিতীয় ধাপ উপস্থাপন করছি।

এই কৌশলটি ট্রেন্ডিং মার্কেটে খুব লাভজনক বলে প্রমাণিত হয়েছে, তবে ট্রেন্ডিং মার্কেটের সময় ক্ষতির সম্মুখীন হতে পারে। সিস্টেমটিকে আরও শক্তিশালী করার জন্য, কৌশলটি কেবল ট্রেন্ডিং সিস্টেমের উপর নির্ভর করতে পারে না। অন্যান্য সিস্টেম যুক্ত করতে হবে। আমি বিশ্বাস করি যে একটি ভাল ট্রেডিং বট বিভিন্ন সিস্টেমের উপর ভিত্তি করে 4 টিরও বেশি বিভিন্ন কৌশল নিয়ে গঠিত হতে হবে। এটিই আমি বর্তমানে কাজ করছি।

এই কৌশলটি প্রকাশ করার জন্য আমার লক্ষ্য হল অন্য ব্যবসায়ীদের তাদের নিজস্ব তৈরি করতে সহায়তা করা। আমার যাত্রায় আমি একটি ভাল কৌশল খুঁজে পাওয়া কঠিন ছিল যা একটি শালীন ঝুঁকি ব্যবস্থাপনা ব্যবহার করে, যা সত্যিই ভাল, ধারাবাহিক ফলাফলের জন্য অপরিহার্য। এছাড়াও, একটি বাস্তবসম্মত কমিশন একটি বাস্তবসম্মত কর্মক্ষমতা পূর্বাভাস আছে সংজ্ঞায়িত করা প্রয়োজন। এটি লাভজনকতা উপর weighs এবং তাই প্রায়ই অন্য কৌশল লেখক দ্বারা 0 সেট করা হয়, যা আমি বিভ্রান্তিকর খুঁজে।

যদি আপনি এই কৌশলটি তথ্যবহুল বা উপযোগী বলে মনে করেন, তাহলে দয়া করে একটি মন্তব্য করুন।

সালাম মাইকেল

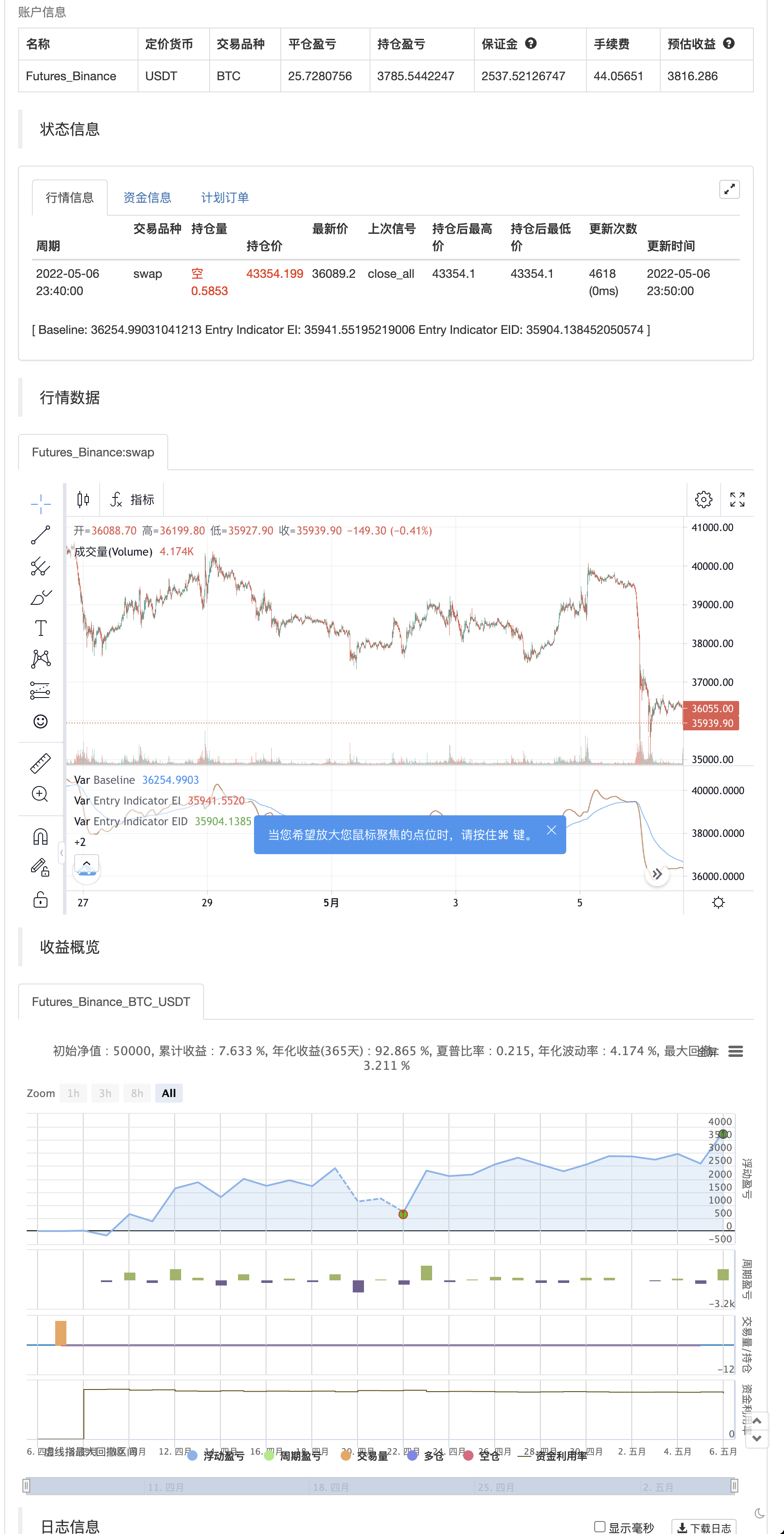

ব্যাকটেস্ট

// © Milleman

//@version=4

//strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

// Additional settings

Mode = input(title="Mode", defval="LongShort", options=["LongShort", "OnlyLong", "OnlyShort","Indicator Mode"])

UseTP = false //input(false, title="Use Take Profit?")

QuickSwitch = true //input(true, title="Quickswitch")

UseTC = true //input(true, title="Use Trendchange?")

// Risk management settings

//Spacer2 = input(false, title="======= Risk management settings =======")

Risk = input(1.0, title="% Risk",minval=0)/100

RRR = 2 //input(2,title="Risk Reward Ratio",step=0.1,minval=0,maxval=20)

SL_Mode = false // input(true, title="ON = Fixed SL / OFF = Dynamic SL (ATR)")

SL_Fix = 3 //input(3,title="StopLoss %",step=0.25, minval=0)/100

ATR = atr(14) //input(14,title="Periode ATR"))

Mul = input(2,title="ATR Multiplier",step=0.1)

xATR = ATR * Mul

SL = SL_Mode ? SL_Fix : (1 - close/(close+xATR))

// INDICATORS //////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

Ind(type, src, len) =>

float result = 0

if type=="McGinley"

result := na(result[1]) ? ema(src, len) : result[1] + (src - result[1]) / (len * pow(src/result[1], 4))

if type=="HMA"

result := wma(2*wma(src, len/2)-wma(src, len), round(sqrt(len)))

if type=="EHMA"

result := ema(2*ema(src, len/2)-ema(src, len), round(sqrt(len)))

if type=="THMA"

lend = len/2

result := wma(wma(src, lend/3)*3-wma(src, lend/2)-wma(src,lend), lend)

if type=="SMA" // Simple

result := sma(src, len)

if type=="EMA" // Exponential

result := ema(src, len)

if type=="DEMA" // Double Exponential

e = ema(src, len)

result := 2 * e - ema(e, len)

if type=="TEMA" // Triple Exponential

e = ema(src, len)

result := 3 * (e - ema(e, len)) + ema(ema(e, len), len)

if type=="WMA" // Weighted

result := wma(src, len)

if type=="VWMA" // Volume Weighted

result := vwma(src, len)

if type=="SMMA" // Smoothed

w = wma(src, len)

result := (w[1] * (len - 1) + src) / len

if type == "RMA"

result := rma(src, len)

if type=="LSMA" // Least Squares

result := linreg(src, len, 0)

if type=="ALMA" // Arnaud Legoux

result := alma(src, len, 0.85, 6)

if type=="Kijun" //Kijun-sen

kijun = avg(lowest(len), highest(len))

result :=kijun

if type=="WWSA" // Welles Wilder Smoothed Moving Average

result := nz(result[1]) + (close -nz(result[1]))/len

result

// Baseline : Switch from Long to Short and vice versa

BL_Act = input(true, title="====== Activate Baseline - Switch L/S ======")

BL_type = input(title="Baseline Type", defval="McGinley", options=["McGinley","HMA","EHMA","THMA","SMA","EMA","DEMA","TEMA","WMA","VWMA","SMMA","RMA","LSMA","ALMA","Kijun","WWSA"])

BL_src = input(close, title="BL source")

BL_len = input(50, title="BL length", minval=1)

BL = Ind(BL_type,BL_src, BL_len)

// Confirmation indicator

C1_Act = input(false, title="===== Activate Confirmation indicator =====")

C1_type = input(title="C1 Entry indicator", defval="SMA", options=["McGinley","HMA","EHMA","THMA","SMA","EMA","DEMA","TEMA","WMA","VWMA","SMMA","RMA","LSMA","ALMA","Kijun","WWSA"])

C1_src = input(close, title="Source")

C1_len = input(5,title="Length", minval=1)

C1 = Ind(C1_type,C1_src,C1_len)

// Entry indicator : Hull Moving Average

Spacer5 = input(true, title="====== ENTRY indicator =======")

EI_type = input(title="EI Entry indicator", defval="HMA", options=["McGinley","HMA","EHMA","THMA","SMA","EMA","DEMA","TEMA","WMA","VWMA","SMMA","RMA","LSMA","ALMA","Kijun","WWSA"])

EI_src = input(close, title="Source")

EI_Len = input(46,title="Length", minval=1)

EI = Ind(EI_type,EI_src,EI_Len)

// Trail stop settings

TrailActivation = input(true, title="===== Activate Trailing Stop =====")

TS_type = input(title="TS Traling Stop Type", defval="EMA", options=["McGinley","HMA","EHMA","THMA","SMA","EMA","DEMA","TEMA","WMA","VWMA","SMMA","RMA","LSMA","ALMA","Kijun","WWSA"])

TrailSLScaling = 1 //input(100, title="SL Scaling", minval=0, step=5)/100

TrailingSourceLong = Ind(TS_type,low,input(5,"Smoothing Trail Long EMA", minval=1))

TrailingSourceShort = Ind(TS_type,high,input(2,"Smoothing Trail Short EMA", minval=1))

//VARIABLES MANAGEMENT

TriggerPrice = 0.0, TriggerPrice := TriggerPrice[1]

TriggerSL = 0.0, TriggerSL := TriggerSL[1]

SLPrice = 0.0, SLPrice := SLPrice[1], TPPrice = 0.0, TPPrice := TPPrice[1]

isLong = false, isLong := isLong[1], isShort = false, isShort := isShort[1]

//LOGIC

GoLong = crossover(EI,EI[1]) and (strategy.position_size == 0.0 and QuickSwitch) and (not BL_Act or BL/BL[1] > 1) and (not C1_Act or C1>C1[1]) and (Mode == "LongShort" or Mode == "OnlyLong")

GoShort = crossunder(EI,EI[1]) and (strategy.position_size == 0.0 and QuickSwitch) and (not BL_Act or BL/BL[1] < 1) and (not C1_Act or C1<C1[1]) and (Mode == "LongShort" or Mode == "OnlyShort")

ExitLong = isLong and crossunder(EI,EI[1]) and UseTC

ExitShort = isShort and crossover(EI,EI[1]) and UseTC

//FRAMEWORK

//Reset Long-Short memory

if isLong and strategy.position_size == 0.0

isLong := false

if isShort and strategy.position_size == 0.0

isShort := false

//Long

if GoLong

isLong := true, TriggerPrice := close, TriggerSL := SL

TPPrice := UseTP? TriggerPrice * (1 + (TriggerSL * RRR)) : na

SLPrice := TriggerPrice * (1-TriggerSL)

Entry_Contracts = strategy.equity * Risk / ((TriggerPrice-SLPrice)/TriggerPrice) / TriggerPrice

strategy.entry("Long", strategy.long, comment=str.tostring(math.round((TriggerSL/TriggerPrice)*1000)), qty=Entry_Contracts)

strategy.exit("TPSL","Long", limit=TPPrice, stop=SLPrice)

if isLong

NewValSL = TrailingSourceLong * (1 - (SL*TrailSLScaling))

if TrailActivation and NewValSL > SLPrice

SLPrice := NewValSL

strategy.exit("TPSL","Long", limit=TPPrice, stop=SLPrice)

if ExitLong

strategy.close_all(comment="TrendChange")

isLong := false

//Short

if GoShort

isShort := true, TriggerPrice := close, TriggerSL := SL

TPPrice := UseTP? TriggerPrice * (1 - (TriggerSL * RRR)) : na

SLPrice := TriggerPrice * (1 + TriggerSL)

Entry_Contracts = strategy.equity * Risk / ((SLPrice-TriggerPrice)/TriggerPrice) / TriggerPrice

strategy.entry("Short", strategy.short, comment=str.tostring(math.round((TriggerSL/TriggerPrice)*1000)), qty=Entry_Contracts)

strategy.exit("TPSL","Short", limit=TPPrice, stop=SLPrice)

if isShort

NewValSL = TrailingSourceShort * (1 + (SL*TrailSLScaling))

if TrailActivation and NewValSL < SLPrice

SLPrice := NewValSL

strategy.exit("TPSL","Short", limit=TPPrice, stop=SLPrice)

if ExitShort

strategy.close_all(comment="TrendChange")

isShort := false

//VISUALISATION

plot(BL_Act?BL:na, color=color.blue,title="Baseline")

plot(C1_Act?C1:na, color=color.yellow,title="confirmation Indicator")

EIColor = EI>EI[1] ? color.green : color.red

Fill_EI = plot(EI, color=EIColor, linewidth=1, transp=40, title="Entry Indicator EI")

Fill_EID = plot(EI[1], color=EIColor, linewidth=1, transp=40, title="Entry Indicator EID")

plot(strategy.position_size != 0.0 and (isLong or isShort) ? TriggerPrice : na, title="TriggerPrice", color=color.yellow, style=plot.style_linebr)

plot(strategy.position_size != 0.0 and (isLong or isShort) ? TPPrice : na, title="TakeProfit", color=color.green, style=plot.style_linebr)

plot(strategy.position_size != 0.0 and (isLong or isShort) ? SLPrice : na, title="StopLoss", color=color.red, style=plot.style_linebr)

- ট্রিপল ইএমএ ক্রসওভার কৌশল

- মঙ্গলবারের টার্নআরাউন্ড কৌশল (উইকেন্ড ফিল্টার)

- RSI/MACD/ATR এর সাথে EMA ক্রসওভার কৌশল উন্নত

- কৌশল অনুসরণ করে মাল্টি-ইন্ডিকেটর ট্রেন্ড

- ফিবোনাচি ট্রেন্ড বিপরীত কৌশল

- আলফা ট্রেডিংবট ট্রেডিং কৌশল

- ভেগাস সুপারট্রেন্ড উন্নত কৌশল

- RSI ট্রেন্ড বিপরীত কৌশল

- ইলিয়ট ওয়েভ থিওরি 4-9 ইমপলস ওয়েভ স্বয়ংক্রিয় সনাক্তকরণ ট্রেডিং কৌশল

- ইনট্রা-ডে স্কেলযোগ্য ভোল্টেবিলিটি ট্রেডিং কৌশল

- পিভট পয়েন্ট এবং ঢাল উপর ভিত্তি করে রিয়েল টাইম ট্রেন্ডলাইন ট্রেডিং

- কিউকিউই এমওডি + এসএসএল হাইব্রিড + ওয়াদা আত্তার বিস্ফোরণ

- স্ট্র্যাট কিনুন/বিক্রয় করুন

- EMA এবং ADX এর সাথে ট্রিপল সুপারট্রেন্ড

- টম ডিমার্ক সিকোয়েন্সিয়াল হিট ম্যাপ

- jma + dwma multigrain দ্বারা

- ম্যাজিক এমএসিডি

- সিগন্যাল দিয়ে Z স্কোর

- পাইন ভাষার সংস্করণ

- 3EMA + Boullinger + PIVOT

- মাল্টি-গ্রেন দ্বারা বেগেট

- K এর বিপরীত সূচক I

- গলিত মোমবাতি

- এমএ সম্রাট ইনসিলিকনোট

- ডেমার্ক রিভার্স পয়েন্টস

- সুইং হাইস/লস এবং ক্যান্ডেল প্যাটার্নস

- টিএমএ ওভারলে

- এমএসিডি + এসএএমএ ২০০ কৌশল

- সিএম স্লিং শট সিস্টেম

- বোলিংজার + আরএসআই, ডাবল স্ট্র্যাটেজি v1.1

- বোলিংজার ব্যান্ড কৌশল