Multi-Faktor-Strategiekombination

Hier ist eine ausführliche Strategieanalyse, die ich basierend auf Ihrem bereitgestellten Handelsstrategiecode verfasst habe:

Übersicht

Diese Strategie kombiniert mehrere Faktoren, um die Vorteile verschiedener Indikatoren zu nutzen und eine umfassende Handelsstrategie zu entwickeln. Sie setzt sich hauptsächlich aus folgenden Faktoren zusammen:

- Stoch.RSI - Stochastischer RSI (gleitender Durchschnitt)

- RSI - Relativer Stärkeindex

- Double Strategy - Doppelstrategie aus Stochastik und RSI

- CM Williams Vix Fix - Williams Volatilitätsreparatur zur Erkennung von Markttiefs

- DMI - Directional Movement Index

Durch die Kombination mehrerer Faktoren können die Stärken jedes Indikators genutzt, mehr Handelsmöglichkeiten gefunden und das Risiko einer Abhängigkeit von einem einzelnen Faktor verringert werden.

Strategieprinzip

Die Strategie verwendet die folgenden technischen Indikatoren:

-

Stoch.RSI - Der stochastische RSI kombiniert die Vorteile von RSI und Stochastic. Er verwendet die RSI-Werte als Eingabe für den Stochastic-Indikator, um zu bestimmen, ob sich der Markt im überkauften oder überverkauften Bereich befindet. Wenn die %K-Linie von oben nach unten die %D-Linie im überkauften Bereich kreuzt, wird eine Long-Position eröffnet; wenn die %K-Linie von unten nach oben die %D-Linie im überverkauften Bereich kreuzt, wird eine Short-Position eröffnet.

-

RSI - Der Relative Stärkeindex zeigt den überkauften und überverkauften Zustand des Marktes an. Ein RSI über 70 gilt als überkauft, unter 30 als überverkauft. Pendelt der RSI zwischen 30 und 70, deutet dies auf eine seitwärts verlaufende Konsolidierungsphase hin.

-

Double Strategy - Eine Doppelstrategie, die Stochastik und RSI kombiniert. Wenn die %K-Linie des Stochastic von oben nach unten die %D-Linie im überverkauften Bereich kreuzt und der RSI ebenfalls von oben nach unten den überverkauften Bereich durchbricht, wird eine Long-Position eröffnet. Wenn die %K-Linie des Stochastic von unten nach oben die %D-Linie im überkauften Bereich kreuzt und der RSI von unten nach oben den überkauften Bereich durchbricht, wird eine Short-Position eröffnet.

-

CM Williams Vix Fix - Der Williams Volatilitätsreparaturindikator berechnet den Perzentilbereich der Preisschwankungen über einen bestimmten Zeitraum, um zu bestimmen, ob sich der Markt an einem Wendepunkt befindet. Überschreitet der Wert einen Schwellenwert, wird ein Umkehrsignal generiert.

-

DMI - Der Directional Movement Index misst die Differenz zwischen +DI und -DI, um die Markttrendrichtung zu bestimmen. Der ADX kann zur Bewertung der Trendstärke verwendet werden.

Durch die kombinierte Nutzung der jeweiligen Stärken dieser Indikatoren kann die Marktrichtung und der beste Ein-/Ausstiegspunkt aus verschiedenen Blickwinkeln beurteilt werden, was die Stabilität und Erfolgsrate der Strategie verbessert.

Strategievorteile

- Multifaktor-Kombination, verschiedene Faktoren ergänzen sich gegenseitig – umfassender Ansatz

- Enthält verschiedene Signaltypen wie Trend und Umkehr – mehr Handelsmöglichkeiten

- Gleichzeitige Erkennung von überkauften/überverkauften Zonen – frühzeitige Identifizierung extremer Marktzustände und Umkehrungen

- Verwendung parametrisierter Indikatoreinstellungen, die besser an unterschiedliche Marktumgebungen angepasst sind

- Kombination mit Trendindikator zur Beurteilung der Trendstärke – Vermeidung von Gegentrendgeschäften

Risikoanalyse

- Multifaktor-Kombination: Die Gesamtrobustheit der Strategie muss noch validiert werden

- Einige Indikatoren weisen Homogenitätsprobleme auf – weitere Optimierung der Kombination notwendig

- Bei gleichzeitigem Auftreten von Long- und Short-Signalen müssen klare Auswahlprinzipien für die Strategierichtung definiert werden

- Die Parametereinstellungen erfordern strenge Backtests – willkürliche Änderungen sind nicht empfehlenswert

- Langfristige Haltedauer könnte ineffektiv sein – rechtzeitiger Stop-Loss erforderlich

Optimierungsmöglichkeiten

- Weitere Selektion der in der Kombination enthaltenen Indikatoren – nur Indikatoren mit einzigartigem Mehrwert beibehalten

- Optimierung der Parametereinstellungen jedes Indikators für den Zielmarkt

- Etablierung klarer Regeln für Ein- und Ausstiege

- Kombination mit Stop-Loss und Take-Profit sowie Trailing-Stop zur Risikokontrolle

- Testen des Einflusses verschiedener Haltedauern auf die Performance

Zusammenfassung

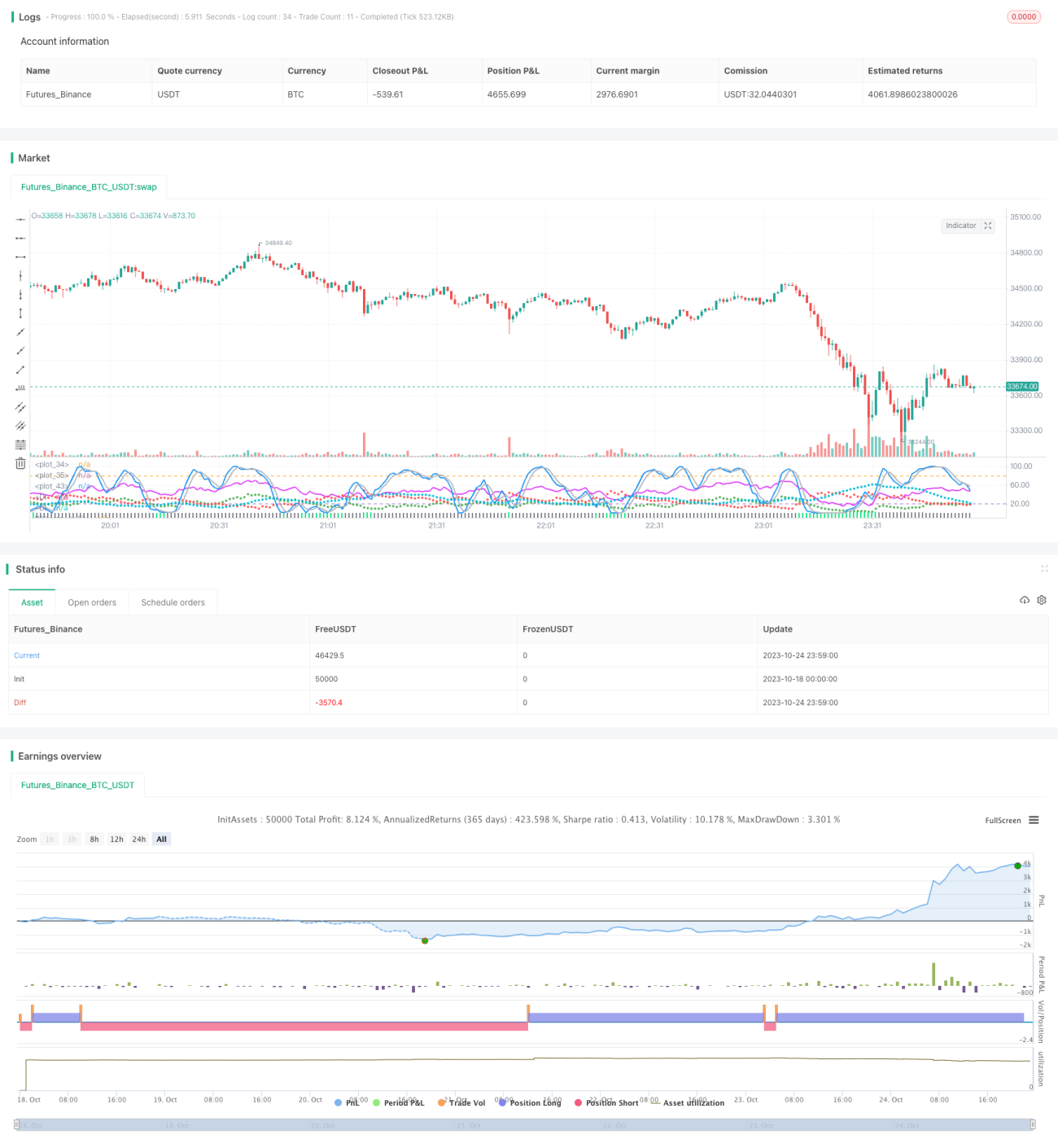

Die Strategie nutzt die Vorteile mehrerer technischer Indikatoren, um Handelssignale aus Faktoren wie Stoch.RSI, RSI, Double Strategy, CM Williams Vix Fix und DMI zu generieren. Sie bietet eine umfassendere und stabilere Entscheidungsgrundlage, macht aber auch die Optimierung der Strategieparameter komplexer. Durch weitere Optimierung der Parametereinstellungen, Auswahl einzigartiger Faktoren und Festlegung klarer Ein-/Ausstiegsregeln kann die Stabilität und Performance der Strategie verbessert werden. Dennoch müssen die Gesamtrobustheit und die Eignung für langfristige Positionen noch streng überprüft werden. Diese Strategie ist ein gutes Beispiel für eine multifaktorielle Handelsstrategie und es lohnt sich, von ihr zu lernen.

/*backtest

start: 2023-10-18 00:00:00

end: 2023-10-25 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//////////////////////////////////////////////////////////////////////

//// STOCHASTIC_RSI+RSI+DOUBLE_STRATEGY+CM_WILLIAMS_VIX_FIX+DMI ////

//////////////////////////////////////////////////////////////////////- 1