Drei-Faktor-Modell zur unterstützenden Beurteilung von Preisschwankungen

Übersicht

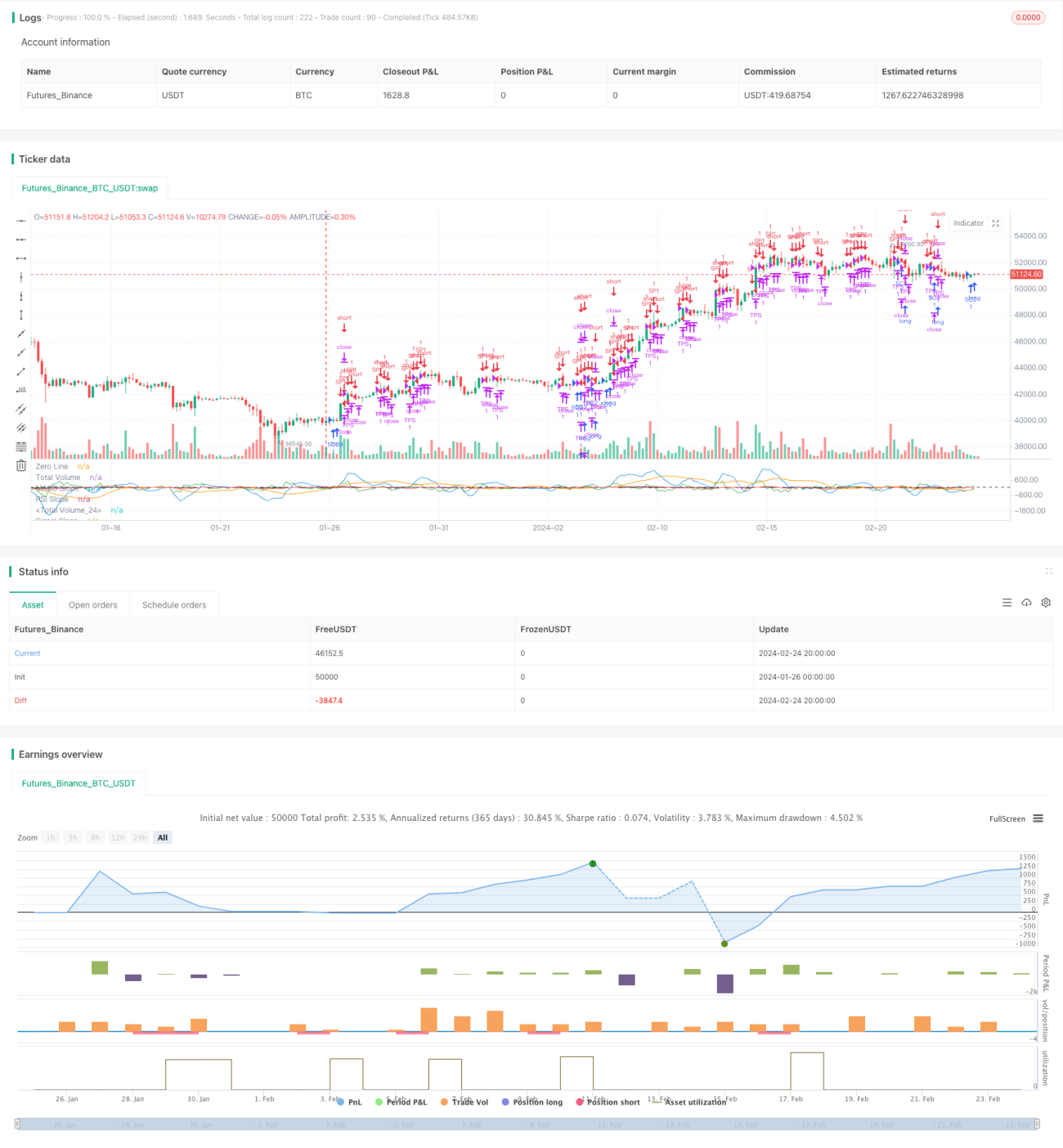

Das Drei-Faktoren-Modell zur unterstützenden Beurteilung von Preisschwankungen ist eine kurzfristige Handelsstrategie, die mehrere Faktoren integriert. Die Strategie berücksichtigt umfassend das Volumenverhältnis, den RSI-Indikator, den MACD-Indikator und den Signallinien-Indikator, um Preisschwankungen zu beurteilen und kurzfristige Handelsmöglichkeiten zu identifizieren.

Strategieprinzip

Der Kernlogik dieser Strategie ist:

- Berechnung technischer Indikatoren wie schneller gleitender Durchschnitt, langsamer gleitender Durchschnitt, MACD-Kurve und Signallinie;

- Bewertung der Mehrfaktor-Bedingungen wie Kauf-/Verkaufsvolumenverhältnis, RSI-Indikator, MACD-Indikator und Signallinien-Indikator;

- Kombination der Mehrfaktor-Beurteilung zur Bestätigung einer aktuellen Preisschwankungsphase mit Handelsmöglichkeiten;

- Eingehen von LONG- oder SHORT-Positionen mit festgelegten Take-Profit und Stop-Loss;

- Schließen der Position, wenn der Preis die Take-Profit- oder Stop-Loss-Bedingungen erreicht.

Die Strategie nutzt flexibel mehrere Faktoren wie Volumenverhältnis, RSI, MACD und Signallinie, um Preisschwankungen zu beurteilen und kurzfristige Handelschancen zu erfassen. Die Mehrfaktor-Kombination vermeidet Fehlsignale, die durch einzelne Faktoren entstehen, und erhöht die Signaltreffsicherheit.

Vorteilsanalyse

Die Strategie bietet folgende Vorteile:

- Mehrfaktor-Beurteilung erhöht die Signaltreffsicherheit und vermeidet Fehlsignale;

- Nutzung der Eigenschaften von Preisschwankungen zur Erfassung kurzfristiger Handelsmöglichkeiten mit großem Gewinnpotenzial;

- Automatische Festlegung von Take-Profit und Stop-Loss zur Risikokontrolle;

- Einfache und klare Handelslogik, leicht umsetzbar.

Risikoanalyse

Die Strategie birgt auch folgende Risiken:

- Der Algorithmus hängt zu stark von historischen Daten ab und reagiert empfindlich auf Marktveränderungen;

- Die Kombination der Mehrfaktor-Kriterien muss möglicherweise weiter optimiert werden, es besteht die Möglichkeit von Fehlentscheidungen;

- Die angemessene Festlegung des Stop-Loss wirkt sich direkt auf die Stabilität der Strategie aus.

Gegen diese Risiken können folgende Optimierungen vorgenommen werden:

- Vergrößerung des Datenabtastzeitraums zur Verringerung des Einflusses von Marktdatenänderungen;

- Anpassung der Mehrfaktor-Gewichtung zur Realisierung adaptiver Optimierung;

- Testen verschiedener Stop-Loss-Punkte zur Findung der optimalen Stop-Loss-Position.

Optimierungsrichtungen

Die Strategie kann hauptsächlich in folgenden Bereichen optimiert werden:

- Optimierung der Mehrfaktor-Gewichtung zur dynamischen Anpassung. Je nach Marktphase können die Gewichtungen der Faktoren angepasst werden, um die Anpassungsfähigkeit zu erhöhen;

- Integration von maschinellen Lernalgorithmen zur adaptiven Optimierung der Mehrfaktor-Kombination. Einsatz von neuronalen Netzen, genetischen Algorithmen etc. zum Trainieren des Mehrfaktor-Modells und zur automatischen Parameteroptimierung;

- Optimierung der Stop-Loss-Strategie. Testen verschiedener Trailing-Stop-Loss- und Moving-Stop-Loss-Kombinationen zur Findung der optimalen Stop-Loss-Lösung;

- Einbeziehung fortgeschrittener technischer Indikatoren. Testen weiterer Indikatoren wie Volatilitäts-Oszillator, Momentum-Oszillator etc. zur Bereicherung der Mehrfaktor-Kombination.

Zusammenfassung

Die Strategie "Drei-Faktoren-Modell zur unterstützenden Beurteilung von Preisschwankungen" nutzt die Mehrfaktor-Eigenschaften von Preisschwankungsbereichen voll aus, um eine effiziente kurzfristige Handelsstrategie zu realisieren. Die Strategie verwendet mehrere Faktoren wie Volumen, RSI, MACD und Signallinie zur Bestimmung optimaler Kauf- und Verkaufszeitpunkte. Die Mehrfaktor-Beurteilung erhöht die Signaltreffsicherheit und begünstigt stabile Renditen. Durch maschinelles Lernen kann zukünftig eine adaptive Optimierung der Mehrfaktor-Kombination erreicht werden, um eine noch überragendere Strategieleistung zu erzielen.

/*backtest

start: 2024-01-26 00:00:00

end: 2024-02-25 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("3 10.0 Oscillator Profile Flagging", shorttitle="3 10.0 Oscillator Profile Flagging", overlay=false)

signalBiasValue = input(title="Signal Bias", defval=0.26)- 1