Stratégie de divergence des prix v1.0

Auteur:ChaoZhang est là., Date: le 31 mai 2022 à 18h31h45Les étiquettes:Le MACDIndice de résistance

Créé par demande: Il s'agit d'une stratégie de trading de tendance qui utilise des signaux de détection de la divergence de prix qui sont confirmés par l'oscillateur mathématique de Murray (basé sur le canal Donchanin).

Code de stratégie basé sur: Détecteur de divergence de prix V2 de RicardoSantos L'oscillateur mathématique UCS_Murrey par Ucsgears Stratégie de gestion des risques basée sur: Exemple de code de stratégie par JayRogers

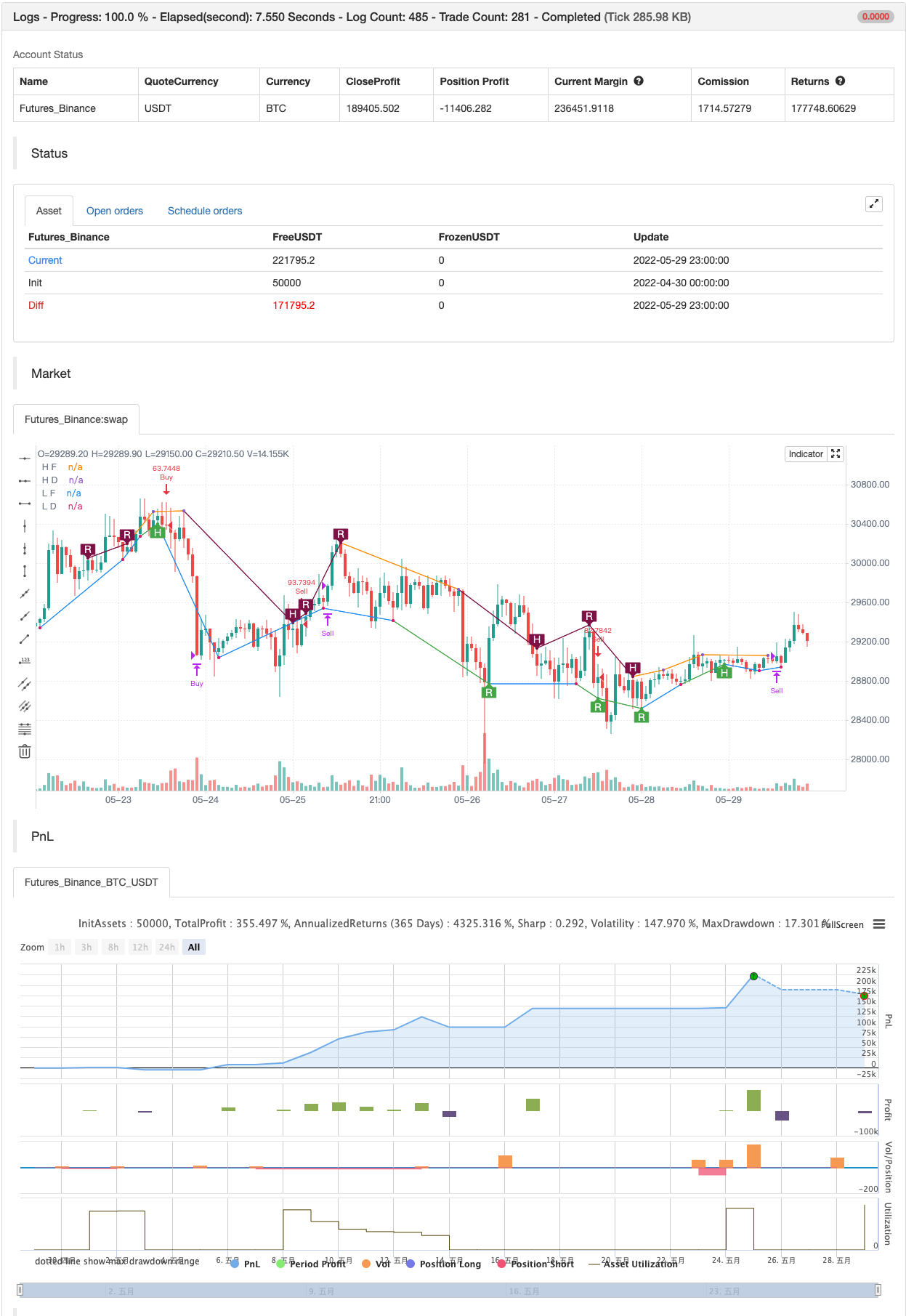

test de retour

/*backtest

start: 2022-04-30 00:00:00

end: 2022-05-29 23:59:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//

// Title: [STRATEGY][UL]Price Divergence Strategy V1.1

// Author: JustUncleL

// Date: 23-Oct-2016

// Version: v1.1

//

// Description:

// A trend trading strategy the uses Price Divergence detection signals, that

// are confirmed by the "Murrey's Math Oscillator" (Donchanin Channel based).

//

// *** USE AT YOUR OWN RISK ***

//

// Mofidifications:

// 1.0 - original

// 1.1 - Pinescript V4 update 21-Aug-2021

//

// References:

// Strategy Based on:

// - [RS]Price Divergence Detector V2 by RicardoSantos

// - UCS_Murrey's Math Oscillator by Ucsgears

// Some Code borrowed from:

// - "Strategy Code Example by JayRogers"

// Information on Divergence Trading:

// - http://www.babypips.com/school/high-school/trading-divergences

//

strategy(title='[STRATEGY][UL]Price Divergence Strategy v1.1', pyramiding=0, overlay=true, initial_capital=10000, calc_on_every_tick=false, currency=currency.USD,

default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// || General Input:

method = input(title='Method (0=rsi, 1=macd, 2=stoch, 3=volume, 4=acc/dist, 5=fisher, 6=cci):', type=input.integer, defval=1, minval=0, maxval=6)

SHOW_LABEL = input(title='Show Labels', type=input.bool, defval=true)

SHOW_CHANNEL = input(title='Show Channel', type=input.bool, defval=false)

uHid = input(true, title="Use Hidden Divergence in Strategy")

uReg = input(true, title="Use Regular Divergence in Strategy")

// || RSI / STOCH / VOLUME / ACC/DIST Input:

rsi_smooth = input(title='RSI/STOCH/Volume/ACC-DIST/Fisher/cci Smooth:', type=input.integer, defval=5)

// || MACD Input:

macd_src = input(title='MACD Source:', type=input.source, defval=close)

macd_fast = input(title='MACD Fast:', type=input.integer, defval=12)

macd_slow = input(title='MACD Slow:', type=input.integer, defval=26)

macd_smooth = input(title='MACD Smooth Signal:', type=input.integer, defval=9)

// || Functions:

f_top_fractal(_src) =>

_src[4] < _src[2] and _src[3] < _src[2] and _src[2] > _src[1] and

_src[2] > _src[0]

f_bot_fractal(_src) =>

_src[4] > _src[2] and _src[3] > _src[2] and _src[2] < _src[1] and

_src[2] < _src[0]

f_fractalize(_src) =>

f_bot_fractal__1 = f_bot_fractal(_src)

f_top_fractal(_src) ? 1 : f_bot_fractal__1 ? -1 : 0

// ||••> START MACD FUNCTION

f_macd(_src, _fast, _slow, _smooth) =>

_fast_ma = sma(_src, _fast)

_slow_ma = sma(_src, _slow)

_macd = _fast_ma - _slow_ma

_signal = ema(_macd, _smooth)

_hist = _macd - _signal

_hist

// ||<•• END MACD FUNCTION

// ||••> START ACC/DIST FUNCTION

f_accdist(_smooth) =>

_return = sma(cum(close == high and close == low or high == low ? 0 : (2 * close - low - high) / (high - low) * volume), _smooth)

_return

// ||<•• END ACC/DIST FUNCTION

// ||••> START FISHER FUNCTION

f_fisher(_src, _window) =>

_h = highest(_src, _window)

_l = lowest(_src, _window)

_value0 = 0.0

_fisher = 0.0

_value0 := .66 * ((_src - _l) / max(_h - _l, .001) - .5) + .67 * nz(_value0[1])

_value1 = _value0 > .99 ? .999 : _value0 < -.99 ? -.999 : _value0

_fisher := .5 * log((1 + _value1) / max(1 - _value1, .001)) + .5 * nz(_fisher[1])

_fisher

// ||<•• END FISHER FUNCTION

rsi_1 = rsi(high, rsi_smooth)

f_macd__1 = f_macd(macd_src, macd_fast, macd_slow, macd_smooth)

stoch_1 = stoch(close, high, low, rsi_smooth)

sma_1 = sma(volume, rsi_smooth)

f_accdist__1 = f_accdist(rsi_smooth)

f_fisher__1 = f_fisher(high, rsi_smooth)

cci_1 = cci(high, rsi_smooth)

method_high = method == 0 ? rsi_1 : method == 1 ? f_macd__1 :

method == 2 ? stoch_1 : method == 3 ? sma_1 : method == 4 ? f_accdist__1 :

method == 5 ? f_fisher__1 : method == 6 ? cci_1 : na

rsi_2 = rsi(low, rsi_smooth)

f_macd__2 = f_macd(macd_src, macd_fast, macd_slow, macd_smooth)

stoch_2 = stoch(close, high, low, rsi_smooth)

sma_2 = sma(volume, rsi_smooth)

f_accdist__2 = f_accdist(rsi_smooth)

f_fisher__2 = f_fisher(low, rsi_smooth)

cci_2 = cci(low, rsi_smooth)

method_low = method == 0 ? rsi_2 : method == 1 ? f_macd__2 :

method == 2 ? stoch_2 : method == 3 ? sma_2 : method == 4 ? f_accdist__2 :

method == 5 ? f_fisher__2 : method == 6 ? cci_2 : na

fractal_top = f_fractalize(method_high) > 0 ? method_high[2] : na

fractal_bot = f_fractalize(method_low) < 0 ? method_low[2] : na

high_prev = valuewhen(fractal_top, method_high[2], 1)

high_price = valuewhen(fractal_top, high[2], 1)

low_prev = valuewhen(fractal_bot, method_low[2], 1)

low_price = valuewhen(fractal_bot, low[2], 1)

regular_bearish_div = fractal_top and high[2] > high_price and method_high[2] < high_prev

hidden_bearish_div = fractal_top and high[2] < high_price and method_high[2] > high_prev

regular_bullish_div = fractal_bot and low[2] < low_price and method_low[2] > low_prev

hidden_bullish_div = fractal_bot and low[2] > low_price and method_low[2] < low_prev

plot(title='H F', series=fractal_top ? high[2] : na, color=regular_bearish_div or hidden_bearish_div ? color.maroon : not SHOW_CHANNEL ? na : color.silver, offset=-2)

plot(title='L F', series=fractal_bot ? low[2] : na, color=regular_bullish_div or hidden_bullish_div ? color.green : not SHOW_CHANNEL ? na : color.silver, offset=-2)

plot(title='H D', series=fractal_top ? high[2] : na, style=plot.style_circles, color=regular_bearish_div or hidden_bearish_div ? color.maroon : not SHOW_CHANNEL ? na : color.silver, linewidth=3, offset=-2)

plot(title='L D', series=fractal_bot ? low[2] : na, style=plot.style_circles, color=regular_bullish_div or hidden_bullish_div ? color.green : not SHOW_CHANNEL ? na : color.silver, linewidth=3, offset=-2)

plotshape(title='+RBD', series=not SHOW_LABEL ? na : regular_bearish_div ? high[2] : na, text='R', style=shape.labeldown, location=location.absolute, color=color.maroon, textcolor=color.white, offset=-2)

plotshape(title='+HBD', series=not SHOW_LABEL ? na : hidden_bearish_div ? high[2] : na, text='H', style=shape.labeldown, location=location.absolute, color=color.maroon, textcolor=color.white, offset=-2)

plotshape(title='-RBD', series=not SHOW_LABEL ? na : regular_bullish_div ? low[2] : na, text='R', style=shape.labelup, location=location.absolute, color=color.green, textcolor=color.white, offset=-2)

plotshape(title='-HBD', series=not SHOW_LABEL ? na : hidden_bullish_div ? low[2] : na, text='H', style=shape.labelup, location=location.absolute, color=color.green, textcolor=color.white, offset=-2)

// Code borrowed from UCS_Murrey's Math Oscillator by Ucsgears

// - UCS_MMLO

// Inputs

length = input(100, minval=10, title="MMLO Look back Length")

quad = input(2, minval=1, maxval=4, step=1, title="Mininum Quadrant for MMLO Support")

mult = 0.125

// Donchanin Channel

hi = highest(high, length)

lo = lowest(low, length)

range = hi - lo

multiplier = range * mult

midline = lo + multiplier * 4

oscillator = (close - midline) / (range / 2)

a = oscillator > 0

b = oscillator > 0 and oscillator > mult * 2

c = oscillator > 0 and oscillator > mult * 4

d = oscillator > 0 and oscillator > mult * 6

z = oscillator < 0

y = oscillator < 0 and oscillator < -mult * 2

x = oscillator < 0 and oscillator < -mult * 4

w = oscillator < 0 and oscillator < -mult * 6

// Strategy: (Thanks to JayRogers)

// === STRATEGY RELATED INPUTS ===

//tradeInvert = input(defval = false, title = "Invert Trade Direction?")

// the risk management inputs

inpTakeProfit = input(defval=0, title="Take Profit Points", minval=0)

inpStopLoss = input(defval=0, title="Stop Loss Points", minval=0)

inpTrailStop = input(defval=100, title="Trailing Stop Loss Points", minval=0)

inpTrailOffset = input(defval=0, title="Trailing Stop Loss Offset Points", minval=0)

// === RISK MANAGEMENT VALUE PREP ===

// if an input is less than 1, assuming not wanted so we assign 'na' value to disable it.

useTakeProfit = inpTakeProfit >= 1 ? inpTakeProfit : na

useStopLoss = inpStopLoss >= 1 ? inpStopLoss : na

useTrailStop = inpTrailStop >= 1 ? inpTrailStop : na

useTrailOffset = inpTrailOffset >= 1 ? inpTrailOffset : na

// === STRATEGY - LONG POSITION EXECUTION ===

enterLong() => // functions can be used to wrap up and work out complex conditions

(uReg and regular_bullish_div or uHid and hidden_bullish_div) and

(quad == 1 ? a[1] :

quad == 2 ? b[1] : quad == 3 ? c[1] : quad == 4 ? d[1] : false)

exitLong() =>

oscillator <= 0

strategy.entry(id="Buy", long=true, when=enterLong()) // use function or simple condition to decide when to get in

strategy.close(id="Buy", when=exitLong()) // ...and when to get out

// === STRATEGY - SHORT POSITION EXECUTION ===

enterShort() =>

(uReg and regular_bearish_div or uHid and hidden_bearish_div) and

(quad == 1 ? z[1] :

quad == 2 ? y[1] : quad == 3 ? x[1] : quad == 4 ? w[1] : false)

exitShort() =>

oscillator >= 0

strategy.entry(id="Sell", long=false, when=enterShort())

strategy.close(id="Sell", when=exitShort())

// === STRATEGY RISK MANAGEMENT EXECUTION ===

// finally, make use of all the earlier values we got prepped

strategy.exit("Exit Buy", from_entry="Buy", profit=useTakeProfit, loss=useStopLoss, trail_points=useTrailStop, trail_offset=useTrailOffset)

strategy.exit("Exit Sell", from_entry="Sell", profit=useTakeProfit, loss=useStopLoss, trail_points=useTrailStop, trail_offset=useTrailOffset)

//EOF

Relationnée

- Stratégie de négociation à haute fréquence de crypto-monnaie stable à faible risque basée sur le RSI et le MACD

- Le BOT de Johnny

- Tendance multi-indicateurs à la suite de la stratégie

- Stratégie du détecteur de vallée MACD

- Tendance multi-indicateur à la suite d'une stratégie dynamique de gestion des risques

- VuManChu chiffrement B + stratégie de divergence

- Stratégie de grille de position variable suivant la tendance

- Stratégie de négociation dynamique basée sur le volume MA et sur la pyramide adaptative

- 15 minutes BTCUSDTPERP BOT

- Stratégie dynamique de DCA basée sur le volume

Plus de

- Tendance linéaire

- Modèle de synchronisation de Fibonacci

- Boîte Darvas acheter vendre

- Indicateur de configuration de démarrage

- Indice de change stochastique extrême

- Indicateur MACD BB V 1,00

- SAR parabolique

- Indicateur de divergence RSI

- Indicateur OBV MACD

- Tendance de pivot

- Dépassement du support-résistance

- Moyenne mobile adaptative de pente

- Stratégie de l'oscillateur Delta-RSI

- Stratégie de cryptographie à faible balayage

- [blackcat] L2 stratégie de renversement des étiquettes

- SuperB

- SAR élevé SAR bas

- SuperTREX

- Détecteur de pic

- Détecteur bas