मोड़ बिंदुओं पर आधारित RSI विचलन रणनीति

अवलोकन

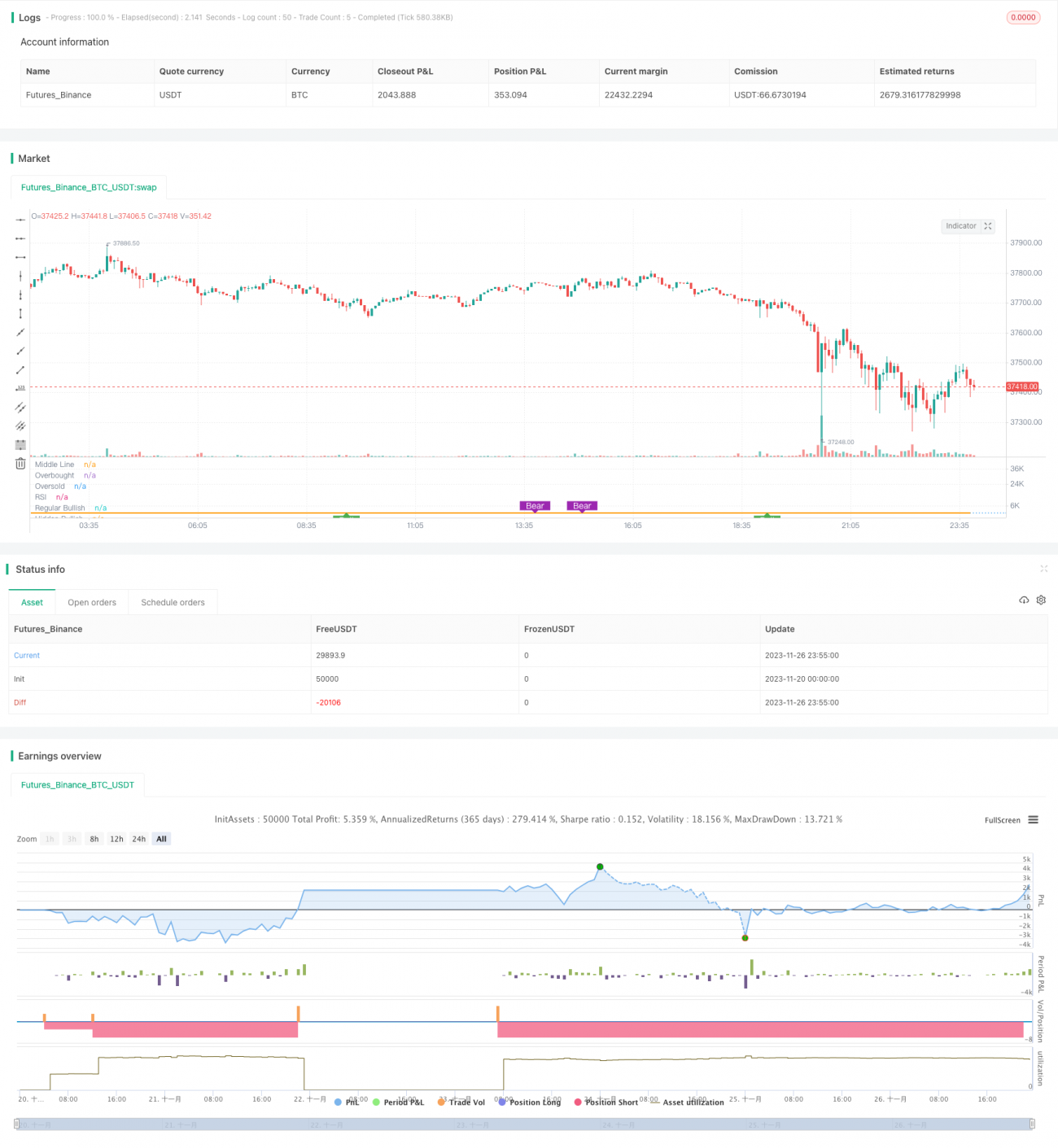

इस रणनीति का नाम "पिवट-आधारित RSI डाइवर्जेंस रणनीति" (Pivot-based RSI Divergence Strategy) है। यह RSI संकेतक के विभिन्न अवधियों पर डाइवर्जेंस (अपसरण) का उपयोग करके खरीद और बिक्री के बिंदु निर्धारित करती है, और इसके ऊपर दीर्घकालिक RSI को फ़िल्टर शर्त के रूप में जोड़ती है, जिससे रणनीति की स्थिरता बढ़ जाती है।

रणनीति का सिद्धांत

यह रणनीति मुख्य रूप से तब खरीद का अवसर मानती है जब अल्पकालिक RSI (जैसे 5-दिवसीय RSI) और मूल्य में "छिपा हुआ तेजी का डाइवर्जेंस" (Hidden Bullish Divergence) या "सामान्य तेजी का डाइवर्जेंस" (Regular Bullish Divergence) दिखाई दे; तथा तब बेचने का अवसर मानती है जब "छिपा हुआ मंदी का डाइवर्जेंस" (Hidden Bearish Divergence) या "सामान्य मंदी का डाइवर्जेंस" (Regular Bearish Divergence) दिखाई दे।

सामान्य तेजी का डाइवर्जेंस का अर्थ है: मूल्य नया निचला स्तर बनाता है जबकि RSI नया निचला स्तर नहीं बनाता। इसके विपरीत, छिपा हुआ तेजी का डाइवर्जेंस तब होता है जब मूल्य नया निचला स्तर नहीं बनाता जबकि RSI नया निचला स्तर बनाता है। दोनों परिभाषाओं में "नया निचला" और "नया ऊँचा" एक निश्चित चल खिड़की के ऐतिहासिक चरम मूल्यों के सापेक्ष होते हैं।

इसके अतिरिक्त, रणनीति दीर्घकालिक RSI (जैसे 50-दिवसीय RSI) को फ़िल्टर के रूप में शामिल करती है। केवल जब लंबी अवधि का RSI 50 से अधिक होता है, तब खरीद संकेत पर विचार किया जाता है; जब लंबी अवधि का RSI 30 से कम होता है, तो स्टॉप-लॉस या टेक-प्रॉफिट से बाहर निकलने पर विचार किया जाता है।

रणनीति के लाभ

इस रणनीति का सबसे बड़ा लाभ यह है कि यह एक साथ अल्पकालिक RSI के डाइवर्जेंस संकेत और दीर्घकालिक RSI के फ़िल्टर का उपयोग करती है, जिससे कुछ हद तक फँसने और अवसरों को चूकने से बचा जा सकता है। विशेष रूप से, इसके निम्नलिखित मुख्य लाभ हैं:

- अल्पकालिक RSI डाइवर्जेंस संकेत मूल्य के उलट होने के अवसर को पहले ही पहचान सकता है, समय पर बाजार के मोड़ को पकड़ सकता है।

- दीर्घकालिक RSI फ़िल्टर शर्त अनिश्चित प्रवृत्ति के दौरान अंधाधुंध खरीद से बचाती है।

- विभिन्न प्रकार के टेक-प्रॉफिट तरीके, आंशिक टेक-प्रॉफिट जोखिम को कम करने में मदद करता है।

- पिरामिडिंग तंत्र स्थिति बढ़ाने की अनुमति देता है, जिससे लाभ का स्थान और बढ़ जाता है।

रणनीति के जोखिम

इस रणनीति में कुछ जोखिमों पर ध्यान देने की आवश्यकता है:

- RSI डाइवर्जेंस हमेशा प्रभावी नहीं होता, झूठे संकेत हो सकते हैं।

- स्थिति बढ़ाने के बाद जोखिम बढ़ जाता है। यदि गलत अनुमान लगे, तो हानि तेजी से बढ़ सकती है।

- टेक-प्रॉफिट का अनुचित निर्धारण भी समय से पहले टेक-प्रॉफिट या अपर्याप्त लाभ का कारण बन सकता है।

इन जोखिमों को प्रबंधित करने के उपायों में शामिल हैं: स्टॉप-लॉस और टेक-प्रॉफिट शर्तों का उचित निर्धारण, प्रत्येक स्थिति के आकार पर नियंत्रण, लाभ-हानि वक्र को सुचारू करने के लिए क्रमशः स्थिति घटाना आदि।

अनुकूलन की दिशा

इस रणनीति में और अनुकूलन की गुंजाइश है:

- RSI मापदंडों को और अनुकूलित किया जा सकता है, सर्वोत्तम मापदंड संयोजन खोजा जा सकता है।

- अन्य संकेतकों के डाइवर्जेंस संकेतों का परीक्षण किया जा सकता है, जैसे MACD, KD आदि।

- विशिष्ट वस्तुओं (जैसे कच्चा तेल, कीमती धातु आदि) पर विशेष रूप से मापदंड अनुकूलित करके अनुकूलनशीलता बढ़ाई जा सकती है।

सारांश

यह रणनीति अल्पकालिक और दीर्घकालिक RSI के तेजी/मंदी डाइवर्जेंस संकेतों का सम्मिलित उपयोग करती है, जोखिम को नियंत्रित करते हुए लाभ दक्षता बढ़ाती है। यह मात्रात्मक ट्रेडिंग रणनीति डिजाइन के कई सिद्धांतों को दर्शाती है, जिसमें कब प्रवेश करना, कब बाहर निकलना, क्रमशः स्थिति बनाना और घटाना, स्टॉप-लॉस और टेक-प्रॉफिट सेट करना आदि शामिल हैं। यह एक संदर्भनीय RSI डाइवर्जेंस रणनीति का उदाहरण है।

- 1