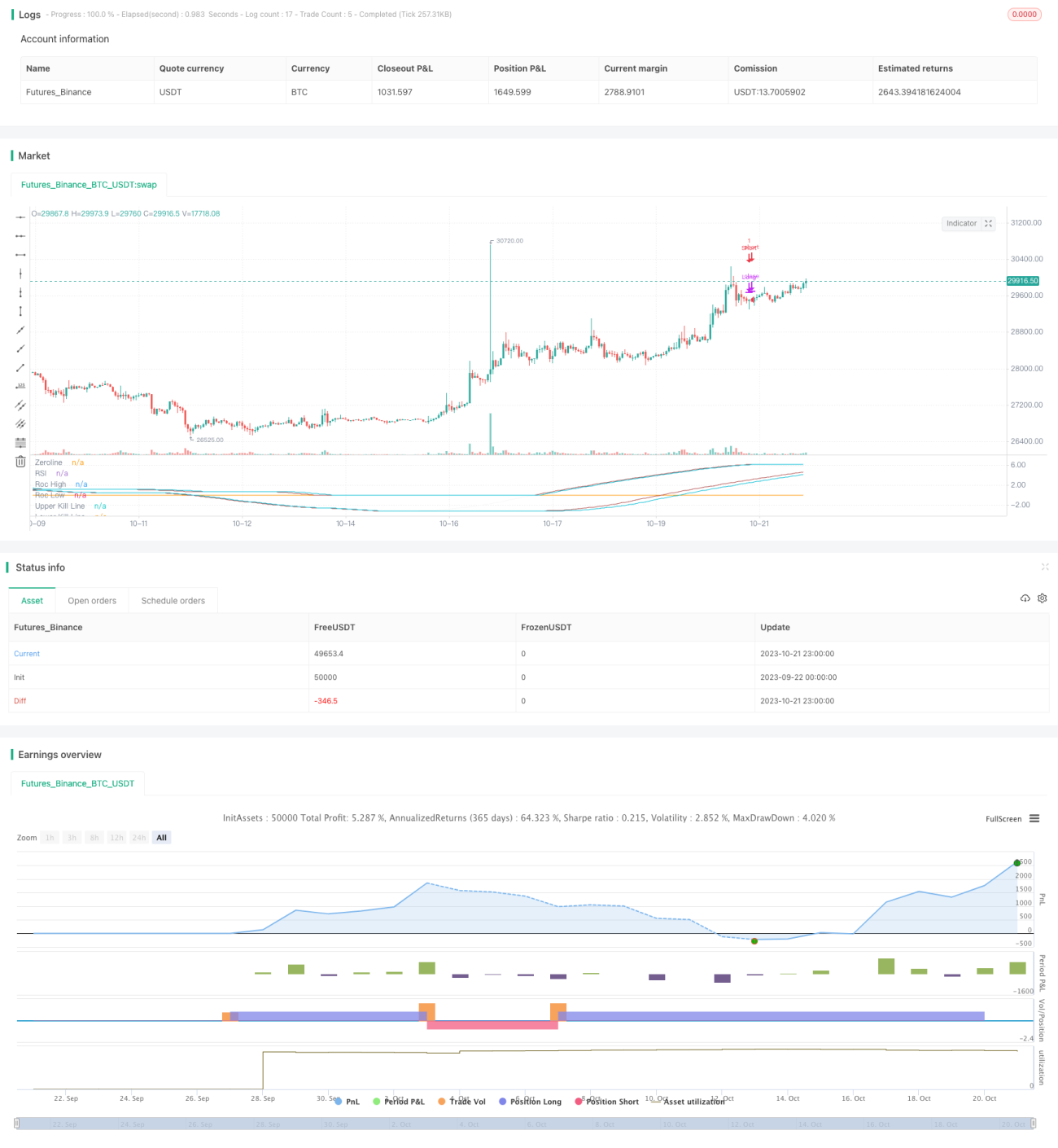

平均足ROCパーセンタイルに基づく取引戦略

概要

本戦略は「Heikin Ashi ROCパーセンタイルに基づく取引戦略」と名付けられ、Heikin Ashi ROCとそのパーセンタイルを用いた使いやすい取引フレームワークを提供することを目的としています。

戦略の原理

本戦略は、Heikin Ashi終値のROCと、その一定期間内の最高値・最安値を計算し、取引に使用する上限ライン・下限ラインを生成します。具体的には、過去rocLength期間のHeikin Ashi終値のROCを計算します。次に、過去50期間のROCの最高値rocHighと最安値rocLowを計算します。その後、rocHighから上限ラインupperKillLineを、rocLowから下限ラインlowerKillLineを算出します。これらの2つのラインは、ROCの特定のパーセンタイルを示します。ROCが下限ラインを上抜けたら買い建て、ROCが上限ラインを下抜けたら買いポジションを決済します。逆に、ROCが上限ラインを下抜けたら売り建て、ROCが下限ラインを上抜けたら売りポジションを決済します。

優位性分析

本戦略の最大の利点は、ROC指標の強力なトレンド追従能力を活かし、Heikin Ashiによる価格情報の平滑化特性と組み合わせることで、トレンドの変化を効果的に識別できる点です。単純な移動平均線などの指標と比較して、ROCは価格変動に対してより敏感に反応し、戦略が適時にエントリーできます。さらに、パーセンタイルを用いて生成された上限ライン・下限ラインにより、レンジ相場を効果的にフィルタリングし、偽のブレイクアウトによる不要な取引を回避できます。全体的に、本戦略はトレンド追従とレンジ相場のフィルタリングという2つの機能を組み合わせており、大きなトレンドにおいて良好なリスクリターン比を得ることができます。

リスク分析

本戦略の主なリスクは、パラメータ設定が不適切な場合、取引頻度が高くなりすぎたり、感度が鈍くなったりする点です。rocLengthとパーセンタイル計算期間は慎重に設定する必要があり、そうでなければ上限ライン・下限ラインが柔軟性を失ったり硬直的になり、取引機会を逃したり不必要な損失を招く可能性があります。また、パーセンタイルの設定も市場ごとに繰り返しテスト・調整し、最適なパラメータ組み合わせを見つける必要があります。トレンドが反転した場合、本戦略はトレンド指標に依存しているため、一定の損失に直面します。保有期間を適切に短縮するか、ストップロスを設定してリスクを管理すべきです。

最適化の方向性

本戦略は以下の点で最適化が可能です。1) RSIなどの他の指標を組み合わせてエントリーシグナルをフィルタリングする。2) 機械学習手法を活用してパラメータを動的に最適化する。3) ストップロス・利確の自動退出メカニズムを設定する。4) 他の非トレンド戦略と組み合わせて戦略のリスクをバランスする。

まとめ

以上をまとめると、本戦略はROC指標の強力なトレンド追従能力を活用し、Heikin Ashi特性を組み合わせてトレンド判断とトレンド追従を行い、ROCのパーセンタイルから形成される上限ライン・下限ラインでストップロスをフィルタリングすることで、良好なトレンド追従効果を実現しています。その強みは、トレンド変化を適時に識別し大きなトレンドに追従できる点、そして上限ライン・下限ラインでレンジ相場をフィルタリングできる点にあります。ただし、パラメータ設定が不適切だと戦略のパフォーマンスに影響し、トレンド反転のリスクに直面します。さらなるパラメータ選択の最適化とストップロス・利確の設定により、本戦略はより安定した結果を得られるでしょう。

- 1