市場流動性とトレンドに基づく短期取引戦略

概要

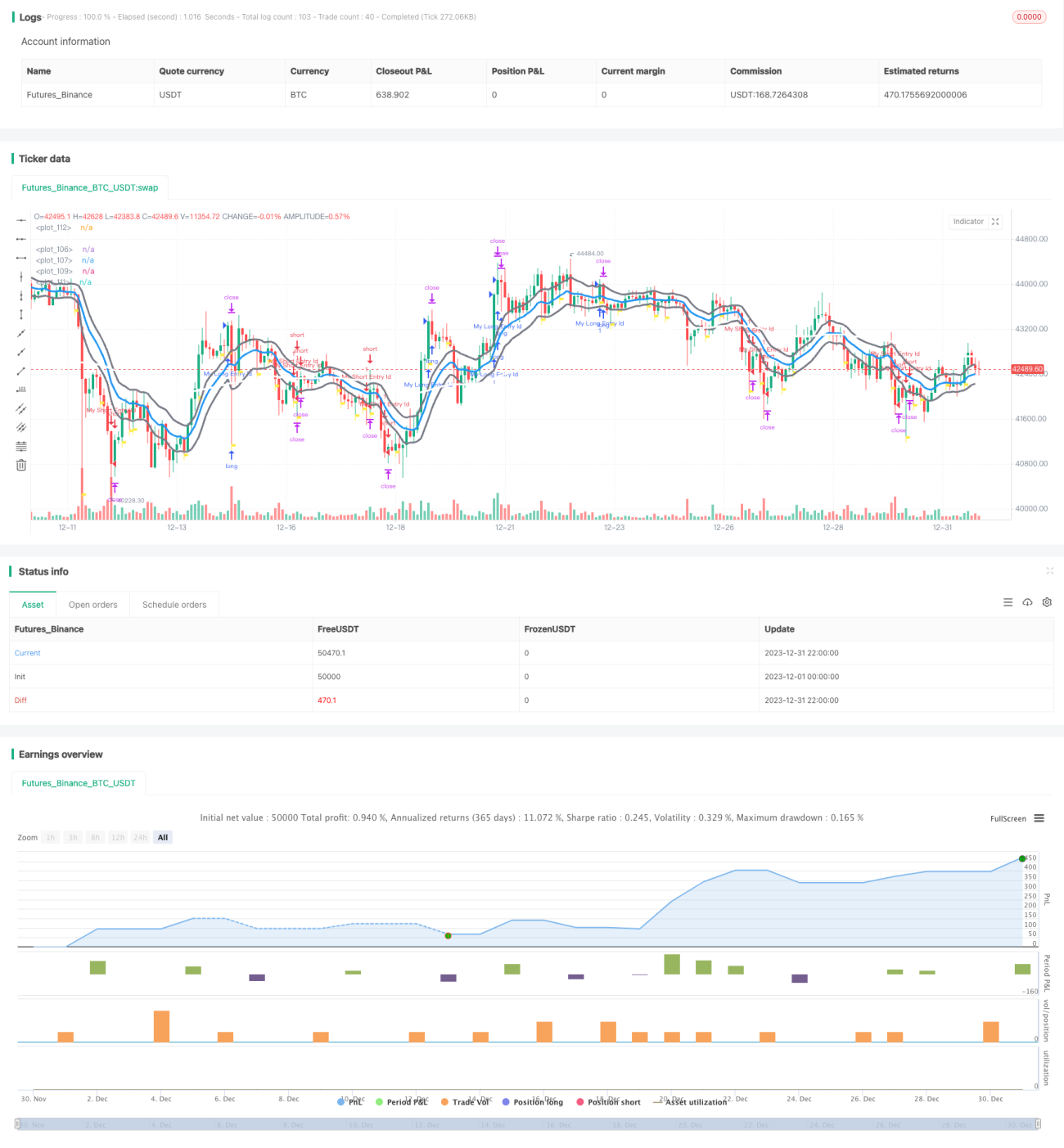

本戦略は、市場の流動性、トレンド、テクニカル指標など複数の次元を総合的に考慮し、短期売買戦略を実行します。この戦略はトレンドに追随し、市場の流動性が良好なタイミングでポジションを建てることで、短期的な利益を獲得することを目的としています。

戦略の原理

-

基本原理:本戦略は主に市場の流動性とトレンドの2つの次元を考慮します。市場の流動性が良好で、かつトレンドが発生した場合に短期売買を行います。

-

市場流動性指標:本戦略では主にMFI(マネーフローインデックス)と出来高の変化を市場流動性の指標として使用します。MFIが上昇し、かつ出来高が増加している場合、市場の流動性が良好で、ポジションを建てるのに適していると判断します。

-

トレンド判断:本戦略はADX、EMAなど複数の指標を組み合わせてトレンドを判断します。ADXが30およびそのEMAを上回っている場合、強いトレンドと見なします。また、短期EMAと長期EMAのゴールデンクロスなどが発生した場合もトレンドの確認に用います。

-

ポジション建て条件:市場の流動性が良好で、かつトレンドが出現している場合、その他の補助条件(SARの位置判断など)も満たしていれば、ポジション建てシグナルが発生します。

-

利確・損切りの設定:本戦略では、各トレードに対して固定の利確(10ポイント)と損切り(7.5ポイント)を設定しています。

優位性分析

本戦略には以下の優位性があります:

-

市場流動性に基づくタイミング判断:MFIと出来高に基づいて市場の流動性を判断し、流動性が低い時のポジション建てを回避します。

-

トレンドに追随して利益を獲得:EMAなどの指標を組み合わせてトレンド方向を判断し、トレンド利益の獲得を支援します。

-

リスク管理が適切:固定の利確・損切りを設定することで、1回の取引における最大損失を効果的に抑制します。

-

取引頻度が比較的高い:短期戦略であるため、取引頻度が高くなりやすく、利益を徐々に積み上げるのに適しています。

-

パラメータ最適化の余地が大きい:MAのパラメータや損切り・利確の設定などを最適化することで、戦略の効果をさらに高めることができます。

リスク分析

本戦略には以下のリスクも存在します:

-

実戦におけるスリッページリスク:理論上の損切り・利確は実戦を完全に反映するものではなく、実戦ではスリッページが大きくなる可能性があります。

-

トレンド判断失敗のリスク:本戦略はトレンド判断に多くの指標を依存していますが、それでも失敗する可能性があります。

-

過剰取引リスク:短期戦略であるため、パラメータ設定が適切でないと過剰取引につながる恐れがあります。

-

市場異常時のリスク:市場の流動性が極端に低下した場合や政策変更などの異常な状況では、本戦略が正常に機能しない可能性があります。

これらに対応するため、以下の方法でリスクを低減できます:

-

損切り範囲を適度に拡大し、実戦のスリッページ要因を考慮する。

-

トレンド判断ロジックを最適化し、より多くの指標を導入して失敗確率を低下させる。

-

ポジション建て頻度に制限を設け、過剰取引を回避する。

-

市場状況に応じて柔軟にパラメータを調整し、異常な状況に対応する。

最適化の方向性

本戦略の最適化の方向性は以下の通りです:

-

トレンド判断をより正確にするために、MACDなどの指標を追加で導入する。

-

MAの期間パラメータを最適化し、最適なパラメータ組み合わせを探す。

-

損切り・利確戦略を改良する(例:トレーリングストップ、レンジストップなど)。

-

取引回数に制限を設け、過度な取引頻度を回避する(例:1日最大3回までポジション建て)。

-

より優れた市場流動性指標を探し、ポジション建てタイミングの判断をさらに改善する(例:ネットインフローなどの指標を導入)。

-

パラメータ自動最適化機能を追加し、最適なパラメータ組み合わせを自動的に見つける。

まとめ

本戦略は市場の流動性やトレンドなど複数の次元を総合的に考慮し、短期間で利益を捕捉します。従来のトレンド戦略と比較して、本戦略の最大の革新点は市場流動性指標を導入し、流動性が低い時のポジション建てを回避することにあります。一方で、本戦略には実戦におけるコントロールリスクやトレンド判断失敗のリスクも存在します。これらのリスクは、さらなる指標の導入、パラメータの最適化、リスク管理の徹底により、本戦略を継続的に改善することが可能です。

- 1